Executive Summary: The High-Stakes Reality of IRS Back Taxes Resolution

In the rapidly evolving landscape of 2026, high-net-worth individuals face unprecedented scrutiny regarding IRS back taxes resolution. Consequently, the proliferation of anonymous advice on platforms like Reddit has created a dangerous echo chamber where well-intentioned but fundamentally flawed guidance threatens wealth preservation and personal freedom.

Furthermore, with the IRS receiving over £80 billion in enforcement appropriations and deploying sophisticated AI-powered detection algorithms, the margin for error in IRS back taxes resolution has virtually disappeared. Indeed, sophisticated investors operating across international jurisdictions—particularly those with connections to Bermuda’s zero-tax regime—find themselves navigating extraordinarily complex compliance requirements.

This authoritative guide, grounded in decades of experience advising ultra-high-net-worth individuals from Hamilton, Bermuda, exposes seven catastrophic mistakes that transform manageable IRS back taxes resolution cases into multi-million-pound financial disasters. Moreover, we reveal why Reddit’s crowdsourced wisdom, whilst emotionally supportive, consistently leads sophisticated investors toward outcomes that professional tax counsel would categorically avoid.

Critical 2026 Update: The IRS has enhanced third-party information reporting to capture cryptocurrency transactions, foreign account movements, and beneficial ownership structures through Corporate Transparency Act requirements. Therefore, the traditional assumption that “the IRS won’t discover historical non-compliance” no longer holds validity in the current enforcement environment.

Understanding IRS Back Taxes Resolution: The 2026 Enforcement Landscape

The Evolution of Tax Enforcement Technology

Firstly, it is essential to understand that IRS back taxes resolution in 2026 operates within a fundamentally transformed technological environment. Specifically, the IRS now employs machine learning algorithms capable of cross-referencing disparate data sources—from FATCA reports to Common Reporting Standard exchanges—with unprecedented precision.

Additionally, the Bermuda Monetary Authority (BMA) has strengthened cooperation frameworks with international tax authorities. As a result, high-net-worth individuals maintaining offshore structures must recognise that historical barriers to information exchange have largely dissolved.

Subsequently, the notion propagated on Reddit forums that “waiting out the statute of limitations” represents a viable strategy for IRS back taxes resolution reflects dangerous misinformation. In fact, the assessment statute never commences when returns remain unfiled, granting the IRS indefinite authority to pursue historical liabilities.

Common Tax Filing Errors 2026: What HNWIs Overlook

Remarkably, even sophisticated investors commit common tax filing errors 2026 that complicate IRS back taxes resolution. Firstly, the misclassification of cryptocurrency dispositions remains endemic, with many taxpayers failing to recognise that every transaction—regardless of magnitude—generates taxable events.

Secondly, foreign pension plan reporting continues to confound international executives. Particularly, the distinction between “qualified” and “non-qualified” foreign pensions creates substantial compliance challenges that Reddit advice consistently mischaracterises.

Thirdly, the treatment of Passive Foreign Investment Companies (PFICs) represents another area where common tax filing errors 2026 proliferate. Specifically, foreign mutual funds, ETFs, and insurance products frequently trigger punitive tax treatment absent timely elections—a nuance rarely discussed in online forums.

Fatal Mistake #1: Relying on Anonymous Reddit Advice for Professional Tax Audit Defense

Why Crowdsourced Wisdom Fails in IRS Back Taxes Resolution

To begin with, professional tax audit defense requires specialised expertise that anonymous Reddit contributors—regardless of good intentions—simply cannot provide. Moreover, the platform’s structure incentivises emotionally satisfying responses over technically accurate guidance.

Consequently, when high-net-worth individuals facing complex IRS back taxes resolution scenarios rely on Reddit advice, they unknowingly assume catastrophic risks. In particular, three fundamental deficiencies plague crowdsourced tax guidance:

The Absence of Attorney-Client Privilege

Primarily, communications on Reddit lack legal privilege protection. Therefore, any admissions regarding willfulness, concealment efforts, or compliance failures become discoverable in subsequent IRS proceedings. Conversely, professional tax audit defense conducted through qualified attorneys provides confidentiality safeguards essential for candid disclosure.

Incomplete Factual Understanding

Additionally, Reddit advice necessarily operates with fragmentary information. However, successful IRS back taxes resolution demands comprehensive factual development—including income sources, foreign account holdings, entity structures, and historical compliance patterns. Indeed, incomplete facts invariably lead to fundamentally flawed strategic recommendations.

Absence of Jurisdictional Expertise

Furthermore, Bermuda HNWI tax liability presents unique complexities that generic Reddit advice cannot address. Specifically, US persons residing in zero-tax jurisdictions face extraordinary reporting burdens whilst receiving minimal foreign tax credit benefits. Therefore, professional guidance tailored to Bermuda-US tax coordination becomes essential.

Comparison: Reddit Advice vs Professional Tax Audit Defense

| Factor | Reddit Advice | Professional Tax Audit Defense |

|---|---|---|

| Legal Privilege | None – Publicly discoverable | Attorney-client privilege protected |

| Factual Development | Fragmentary, self-reported | Comprehensive forensic analysis |

| Liability Insurance | Zero coverage | Professional indemnity insurance |

| Willfulness Assessment | Subjective, often inaccurate | Objective legal standard application |

| Criminal Risk Evaluation | Not addressed | Formal criminal exposure assessment |

| Programme Selection | Generic recommendations | Tailored strategy optimisation |

| Cost | Free (but catastrophically expensive) | £15,000-£200,000+ (wealth preservation investment) |

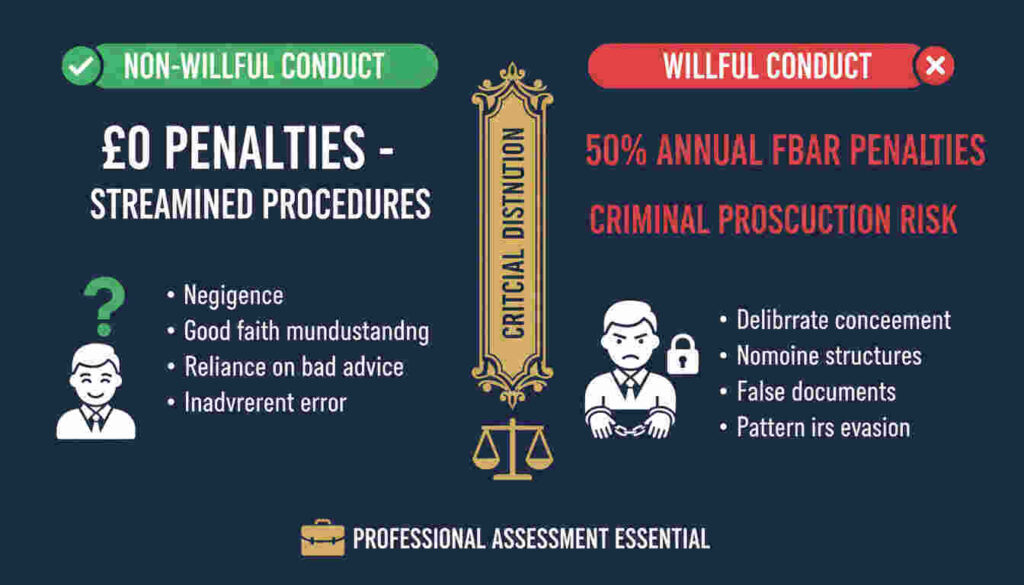

Fatal Mistake #2: Misunderstanding IRS Willful vs Non-Willful Conduct

The Multi-Million Pound Distinction

Crucially, the determination of IRS willful vs non-willful conduct represents the single most consequential factor in IRS back taxes resolution. Nevertheless, Reddit discussions consistently mischaracterise this legal standard, leading taxpayers toward self-assessments that prove catastrophically incorrect.

Specifically, willfulness in tax law means “voluntary, intentional violation of known legal duty.” Conversely, non-willfulness encompasses “negligence, inadvertence, mistake, or good faith misunderstanding of requirements.” Importantly, this distinction determines whether taxpayers face penalty elimination through Streamlined Procedures or multi-million-pound FBAR penalties approaching 50% of account balances annually.

Reddit’s Dangerous Oversimplification

Typically, Reddit contributors suggest that “if you didn’t know about the requirement, it’s non-willful.” However, this oversimplification ignores critical nuances in IRS willful vs non-willful conduct analysis. Indeed, the legal standard examines:

- Sophistication and education: Advanced degrees and professional experience elevate expectations

- Account size and complexity: Multi-million-pound holdings suggest deliberate structuring

- Efforts to conceal: Nominee ownership, encrypted communications, false documents

- Pattern of conduct: Systematic multi-year non-compliance versus isolated oversights

- Professional advice: Reliance on incompetent advisors versus deliberate disregard

Consequently, high-net-worth individuals with sophisticated international structures face substantially elevated willfulness risk—regardless of subjective ignorance claims. Therefore, professional evaluation of IRS willful vs non-willful conduct becomes essential before pursuing any IRS back taxes resolution strategy.

The Bermuda HNWI Complication

Moreover, Bermuda HNWI tax liability creates unique willfulness considerations. Specifically, individuals relocating to Bermuda’s zero-tax environment often receive incorrect advice suggesting US filing obligations cease. Subsequently, when these individuals pursue IRS back taxes resolution years later, the IRS scrutinises whether sophisticated investors could reasonably misunderstand citizenship-based taxation principles.

Additionally, the presence of complex offshore structures—trusts, foreign corporations, insurance wrappers—further elevates willfulness risk in IRS willful vs non-willful conduct assessments. Indeed, the IRS presumes that individuals establishing elaborate international arrangements possess sufficient sophistication to understand reporting obligations.

Fatal Mistake #3: Pursuing Partial Tax Disclosure Without Understanding Risks

The Risks of Partial Tax Disclosure: A Wealth Destruction Strategy

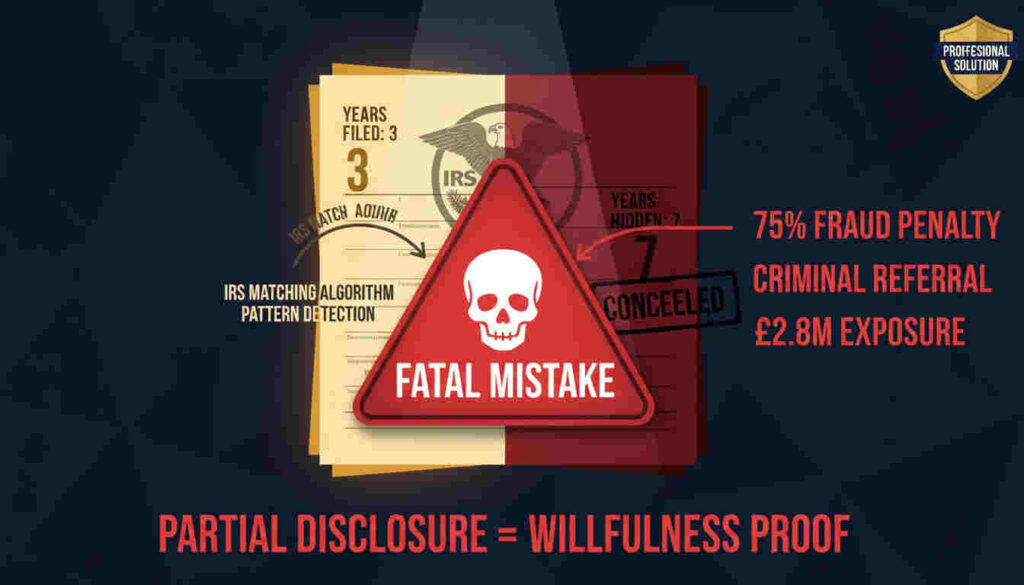

Alarmingly, one of Reddit’s most dangerous recommendations involves filing “some years” whilst omitting others during IRS back taxes resolution. Specifically, contributors frequently suggest addressing “the most recent 3-6 years” whilst hoping older years remain undiscovered. However, this strategy—partial disclosure—represents perhaps the single most catastrophic error in tax compliance.

Fundamentally, the risks of partial tax disclosure stem from the IRS interpretation that selective filing demonstrates awareness of obligations. Therefore, rather than mitigating liability, partial disclosure actually establishes willfulness—transforming what might have qualified for Streamlined Procedures penalty relief into a fraud investigation with enhanced penalties and criminal referral potential.

Real-World Consequences of Partial Disclosure

Consider the following case study illustrating risks of partial tax disclosure in IRS back taxes resolution:

Case Example: A Bermuda-based HNWI with 10 years of unfiled returns followed Reddit advice to file only the most recent 3 years. Subsequently, the IRS matched these filings against historical information returns (Forms W-2, 1099, K-1), discovered the pattern of non-compliance, and initiated a fraud investigation. Consequently, the taxpayer faced penalties exceeding 75% of tax owed plus criminal prosecution for making false statements—a £2.8 million liability that proper IRS back taxes resolution through comprehensive voluntary disclosure would have reduced to approximately £180,000.

The All-or-Nothing Principle

Accordingly, professional tax counsel universally advises the “all-or-nothing principle” for IRS back taxes resolution. Specifically, taxpayers must either file all required years or pursue formal voluntary disclosure programmes providing criminal protection. Indeed, partial compliance represents the worst possible approach—signaling awareness whilst maintaining concealment.

Fatal Mistake #4: DIY IRS Back Taxes Resolution for Complex International Holdings

When Self-Filing Becomes Financial Suicide

Understandably, the appeal of do-it-yourself IRS back taxes resolution stems from cost concerns. Nevertheless, for high-net-worth individuals with international holdings, self-filing frequently transforms manageable situations into catastrophic outcomes.

Particularly, Reddit forums encourage DIY approaches by downplaying complexity. However, successful IRS back taxes resolution involving foreign accounts, entities, and cryptocurrency demands expertise across multiple specialised areas:

International Information Reporting Requirements

Firstly, comprehensive IRS back taxes resolution requires navigating numerous international forms beyond standard tax returns:

- FinCEN Form 114 (FBAR): Foreign account reporting with £10,000+ aggregate balances

- Form 8938: Statement of Specified Foreign Financial Assets

- Form 5471: US persons with foreign corporations (CFC reporting)

- Form 3520: Foreign trust transactions and gift receipts

- Form 8621: Passive Foreign Investment Company annual reporting

- Form 8865: Foreign partnership reporting

Moreover, each form carries separate penalty regimes—ranging from £10,000 to £50,000 annually—for non-compliance. Therefore, DIY IRS back taxes resolution that omits required forms inevitably generates additional liability exceeding any professional fee savings.

Foreign Tax Credit vs FEIE Optimisation

Additionally, strategic decisions between Foreign Tax Credit (FTC) and Foreign Earned Income Exclusion (FEIE) substantially impact IRS back taxes resolution outcomes. Specifically, Bermuda HNWI tax liability presents unique challenges given zero foreign taxes paid—eliminating FTC benefits whilst maximising FEIE importance.

However, FEIE elections require sophisticated analysis of:

- Physical presence test requirements (330 days outside US)

- Bona fide residence determination

- Earned versus unearned income classifications

- Foreign housing expense calculations

- Self-employment tax obligations

Consequently, improper FEIE claims during DIY IRS back taxes resolution trigger immediate examination—often discovering additional compliance failures that professional preparation would have identified proactively.

Fatal Mistake #5: Ignoring the Statute of Limitations Reality

The Perpetual Exposure Myth

Persistently, Reddit contributors perpetuate the dangerous myth that “waiting out the statute of limitations” represents a viable IRS back taxes resolution strategy. However, this fundamentally misunderstands how limitation periods operate in tax law.

Specifically, two separate statutes govern IRS authority:

Assessment Statute of Limitations

Generally, the IRS maintains three years from return filing to assess additional tax. Nevertheless—and this proves critical for IRS back taxes resolution—the assessment statute never commences when returns remain unfiled. Therefore, the IRS retains indefinite authority to assess tax on any unfiled year, regardless of age.

Moreover, the IRS routinely discovers and assesses liabilities decades old. Indeed, recent cases involved assessments on returns from the 1970s and 1980s, subsequently collecting for an additional 10-year period following assessment.

Collection Statute of Limitations

Similarly, whilst the collection statute runs 10 years from assessment, this timeline only begins after the IRS formally assesses the liability. Consequently, for IRS back taxes resolution involving unfiled returns, no collection statute protection exists until returns are filed and assessed.

Furthermore, numerous tolling events suspend the collection statute:

- Bankruptcy proceedings (plus 6 months post-discharge)

- Collection Due Process appeals

- Offer in Compromise submissions

- Innocent spouse relief requests

- Taxpayer Advocate Service interventions

Therefore, the notion that taxpayers can simply “wait out” the IRS represents catastrophically flawed reasoning in IRS back taxes resolution planning.

Critical IRS Back Taxes Resolution Timeline Checklist

- Determine all unfiled tax years (typically 6-10 years recommended)

- Request IRS Wage & Income Transcripts for all years

- Assess criminal statute of limitations (generally 6 years, but tolled during concealment)

- Evaluate voluntary disclosure programme eligibility windows

- Calculate interest accumulation at current 8% annual rate

- Identify tolling events that may have extended statutes

- Determine if IRS has already prepared Substitute for Returns

- Assess whether statute reformation applies (fraud, substantial omission)

- Review foreign account reporting statutes (6 years from adequate disclosure)

- Engage professional counsel before initiating contact with IRS

Fatal Mistake #6: Underestimating Criminal Prosecution Risk

When Civil Tax Debt Becomes Criminal Exposure

Significantly, whilst Reddit discussions acknowledge criminal prosecution possibilities, they consistently underestimate actual risk factors in IRS back taxes resolution. Consequently, high-net-worth individuals pursuing DIY compliance inadvertently trigger red flags that professional counsel would categorically avoid.

Factors Elevating Criminal Referral Risk

Specifically, the IRS Criminal Investigation division prioritizes cases exhibiting:

- Large dollar amounts: Tax deficiencies exceeding £70,000 annually

- Sophisticated concealment: Nominee structures, encrypted communications, document destruction

- Pattern and practice: Systematic multi-year non-compliance

- Public prominence: Professionals in tax/finance/law facing enhanced deterrence value

- Badge of fraud: False statements, backdated documents, obstructive conduct

Moreover, Bermuda HNWI tax liability cases attract particular scrutiny given the jurisdiction’s offshore reputation. Therefore, individuals with complex Bermuda structures pursuing IRS back taxes resolution must recognise elevated criminal investigation risk compared to domestic taxpayers.

Voluntary Disclosure as Criminal Protection

Fortunately, the IRS Voluntary Disclosure Practice provides near-absolute criminal prosecution protection. Specifically, Internal Revenue Manual provisions specify that timely, truthful, complete voluntary disclosures generally preclude criminal referral absent extraordinary circumstances (terrorism financing, money laundering, organised crime connections).

However, critical timing requirements govern voluntary disclosure eligibility. Namely, disclosure must occur before IRS contact regarding the specific years or issues. Subsequently, once examination commences or criminal investigation initiates, voluntary disclosure protection becomes unavailable.

Therefore, professional IRS back taxes resolution strategies prioritise voluntary disclosure timing to secure criminal immunity—a protection that Reddit’s “just file the returns” approach categorically fails to provide.

Fatal Mistake #7: Neglecting Programme-Specific Compliance Requirements

Why Generic Filing Advice Fails

Finally, perhaps Reddit’s most pervasive failure involves generic “just file your returns” recommendations that ignore programme-specific requirements essential for optimal IRS back taxes resolution. Indeed, the IRS maintains several distinct compliance pathways, each with precise eligibility criteria and submission protocols.

Streamlined Filing Compliance Procedures

Primarily, the Streamlined Procedures offer complete penalty elimination for non-willful taxpayers. However, eligibility demands:

- Precise three-year return coverage (tax years 2023, 2024, 2025 for 2026 submissions)

- Six-year FBAR filing (2020-2025)

- Form 14653 non-willfulness certification with detailed narrative

- Physical presence requirement (330+ days abroad for SFOP) or 5% penalty (SDOP)

- Specific mailing address (Austin, TX processing centre)

Consequently, DIY IRS back taxes resolution attempts frequently fail programme requirements through:

- Insufficient non-willfulness narrative detail

- Incorrect year coverage

- Missing international information returns

- Inadequate FBAR maximum balance calculations

- Improper physical presence documentation

Moreover, Streamlined Procedures rejections result in referral to standard examination procedures with full statutory penalties—transforming what should have been penalty-free IRS back taxes resolution into six-figure or seven-figure liability.

Voluntary Disclosure Practice Protocols

Similarly, the Voluntary Disclosure Practice maintains specific submission requirements:

- Preliminary disclosure letter to IRS Criminal Investigation

- Six to eight years of returns (IRS determines exact requirement)

- Comprehensive narrative explaining non-compliance

- Payment arrangements for full tax, interest, and agreed penalties

- Cooperation with subsequent IRS examination

Importantly, the proposed 2026 VDP penalty framework modifications (public comment period concluding 22 March 2026) may provide increased certainty. Nevertheless, final regulations remain pending, making professional guidance essential for navigating transitional rules.

[Tax Information Exchange Agreements]

IRS Back Taxes Resolution Programme Comparison Matrix

| Programme | Penalty Relief | Years Required | Willfulness | Criminal Protection | Professional Fees |

|---|---|---|---|---|---|

| Streamlined (SFOP) | 100% elimination | 3 returns, 6 FBARs | Non-willful only | Not primary purpose | £15,000-£50,000 |

| Streamlined (SDOP) | 5% offshore penalty | 3 returns, 6 FBARs | Non-willful only | Not primary purpose | £15,000-£50,000 |

| Voluntary Disclosure | 20-40% offshore penalty | 6-8 years | Accepts willful | Near-absolute | £50,000-£200,000+ |

| Delinquent FBAR | Zero if reasonable cause | All delinquent years | Non-willful only | None | £5,000-£15,000 |

| Traditional Filing | None (full statutory) | All unfiled years | N/A | None | £5,000-£25,000 |

Risk Mitigation & Common Pitfalls in IRS Back Taxes Resolution

Professional Strategies for Minimising Exposure

Having identified the seven fatal mistakes, it is essential to understand professional risk mitigation strategies for successful IRS back taxes resolution. Specifically, high-net-worth individuals must implement comprehensive compliance protocols addressing both immediate resolution and long-term wealth preservation.

Comprehensive Financial Forensics

Initially, proper IRS back taxes resolution demands exhaustive financial reconstruction. Specifically, this involves:

- Requesting IRS Wage & Income Transcripts for all years

- Obtaining foreign financial institution statements

- Reconstructing cryptocurrency transactions via blockchain analysis

- Analysing bank deposits for unreported gross receipts

- Identifying all foreign account maximum balances for FBAR

- Cataloguing beneficial ownership interests requiring disclosure

Moreover, professional IRS back taxes resolution counsel employs forensic accountants to ensure no income source remains undiscovered—preventing subsequent “quiet disclosure” allegations that would destroy voluntary disclosure protections.

Objective Willfulness Assessment

Subsequently, qualified practitioners conduct formal IRS willful vs non-willful conduct assessments using objective legal standards rather than subjective taxpayer beliefs. This analysis examines:

- Educational background and professional sophistication

- Prior tax compliance history

- Account size suggesting deliberate structuring

- Affirmative concealment efforts (nominees, encryption)

- Professional advice received and followed

- Pattern of conduct across multiple years

Consequently, this objective assessment determines optimal programme selection for IRS back taxes resolution—maximising penalty relief whilst ensuring eligibility requirements are satisfied.

Strategic Programme Selection

Following willfulness determination, professionals evaluate programme eligibility across multiple pathways. Particularly for Bermuda HNWI tax liability cases, this analysis considers:

- Physical presence requirements for SFOP (330+ days abroad annually)

- Account size thresholds triggering enhanced scrutiny

- Foreign tax credit availability (minimal for Bermuda residents)

- FEIE optimisation strategies

- Criminal exposure warranting VDP protection

Therefore, professional IRS back taxes resolution provides tailored strategies rather than Reddit’s one-size-fits-all recommendations.

Comprehensive FAQ: IRS Back Taxes Resolution for HNWIs

Undoubtedly, the most catastrophic error involves pursuing IRS back taxes resolution through partial disclosure—filing some years whilst omitting others. This strategy signals awareness of obligations whilst maintaining concealment, transforming potential non-willful cases into willful fraud investigations with enhanced penalties and criminal referral risk.

The IRS willful vs non-willful conduct distinction determines whether taxpayers face complete penalty elimination (Streamlined Procedures for non-willful) or penalties approaching 50% of foreign account balances annually (willful FBAR violations). Consequently, this single determination can represent multi-million-pound liability differences in IRS back taxes resolution.

Absolutely. Reddit’s crowdsourced guidance lacks legal privilege protection, comprehensive factual development, and jurisdictional expertise. Moreover, following generic “just file the returns” advice without understanding programme-specific requirements frequently results in Streamlined Procedures rejections, triggering full statutory penalties that proper IRS back taxes resolution would have eliminated entirely.

The most prevalent common tax filing errors 2026 include cryptocurrency transaction misclassification, foreign pension plan misreporting, PFIC holdings without required elections, inadequate FBAR maximum balance calculations, and missing international information returns (Forms 5471, 3520, 8621). These errors substantially complicate IRS back taxes resolution and generate additional penalty exposure.

High-net-worth individuals require professional tax audit defense because complex international holdings demand specialised expertise across multiple disciplines—international tax law, foreign trust regulations, PFIC rules, treaty analysis, and criminal tax defense. Additionally, professional representation provides attorney-client privilege protection absent from Reddit discussions, safeguarding sensitive communications during IRS back taxes resolution.

The risks of partial tax disclosure include establishing willfulness through selective filing, triggering fraud investigations, facing enhanced penalties exceeding 75% of tax, criminal prosecution for false statements, and destroying voluntary disclosure eligibility. Consequently, professional counsel universally advises comprehensive disclosure for IRS back taxes resolution rather than partial compliance strategies promoted on Reddit.

Bermuda HNWI tax liability creates unique challenges because zero foreign taxes paid eliminate Foreign Tax Credit benefits, necessitating FEIE optimisation. Moreover, complex offshore structures common among Bermuda residents elevate willfulness risk in IRS back taxes resolution, whilst Bermuda’s offshore reputation attracts enhanced IRS scrutiny compared to traditional expatriate locations.

No. The assessment statute of limitations never commences when returns remain unfiled, granting the IRS indefinite authority to pursue historical liabilities. Therefore, “waiting out the statute” represents catastrophically flawed reasoning in IRS back taxes resolution planning. The IRS routinely assesses tax on returns decades old, then collects for an additional 10-year period following assessment.

The IRS does not publish official acceptance rates for Streamlined Procedures. However, professional practitioners report silent acceptance (no IRS contact) for approximately 85-90% of properly prepared submissions. Conversely, DIY IRS back taxes resolution attempts face substantially higher rejection rates due to inadequate non-willfulness narratives, missing forms, and programme requirement failures.

Professional fees for IRS back taxes resolution vary by complexity: Streamlined Procedures (£15,000-£50,000), complex multi-jurisdiction cases (£30,000-£75,000), Voluntary Disclosure Practice (£50,000-£200,000+), and criminal tax defence (£100,000-£500,000+). However, these fees typically represent 10-30% of penalties avoided through proper programme selection—making professional representation a wealth preservation investment rather than discretionary expense.

Yes, through timely participation in the Voluntary Disclosure Practice before IRS contact. VDP provides near-absolute criminal protection per Internal Revenue Manual provisions, precluding prosecution absent extraordinary circumstances. However, this protection requires initiating IRS back taxes resolution voluntarily before the IRS discovers non-compliance—emphasising the critical importance of immediate professional consultation.

Failed IRS back taxes resolution attempts result in full statutory penalty assessment, potential criminal referral, asset seizure through liens and levies, passport revocation for liabilities exceeding $66,000 (2026 threshold), and destruction of future voluntary disclosure eligibility. Moreover, failed submissions often reveal additional compliance failures that properly prepared disclosures would have addressed proactively.

Conclusion: Strategic Imperatives for Successful IRS Back Taxes Resolution

In conclusion, the landscape of IRS back taxes resolution in 2026 demands sophisticated professional intervention that Reddit’s crowdsourced wisdom simply cannot provide. Indeed, the seven fatal mistakes identified throughout this guide—relying on anonymous advice, misunderstanding willfulness, pursuing partial disclosure, attempting DIY resolution, ignoring statute realities, underestimating criminal risk, and neglecting programme requirements—each represent wealth destruction strategies capable of transforming manageable situations into multi-million-pound catastrophes.

Moreover, for high-net-worth individuals with Bermuda HNWI tax liability and complex international holdings, the margin for error has effectively disappeared. Consequently, the enhanced IRS enforcement capabilities, strengthened international cooperation frameworks, and sophisticated AI-powered detection algorithms ensure that historical assumptions about “the IRS won’t discover” no longer hold validity.

Therefore, successful IRS back taxes resolution requires immediate action across three strategic imperatives:

Three Strategic Imperatives for IRS Back Taxes Resolution

1. Immediate Professional Engagement: Retain qualified tax counsel with demonstrable IRS back taxes resolution expertise before initiating any IRS contact. Specifically, seek practitioners with international compliance specialisation, Streamlined Procedures volume experience, and Voluntary Disclosure Practice familiarity. Verify credentials through bar associations, professional liability insurance confirmation, and client references.

2. Comprehensive Voluntary Disclosure: Pursue all-or-nothing compliance through legitimate IRS programmes rather than partial filing strategies. Particularly, engage forensic financial reconstruction to ensure no income sources remain undiscovered, preventing subsequent “quiet disclosure” allegations that destroy programme protections and criminal immunity.

3. Objective Willfulness Assessment: Obtain professional evaluation of IRS willful vs non-willful conduct using legal standards rather than subjective taxpayer beliefs. This determination fundamentally impacts programme eligibility, penalty exposure, and criminal risk—making it perhaps the single most consequential factor in IRS back taxes resolution outcomes.

The Cost of Inaction

Furthermore, delayed action on IRS back taxes resolution creates escalating exposure through daily compounding interest at 8% annually, increasing criminal statute complications, and potential programme terminations without advance notice. Indeed, the 2018 Offshore Voluntary Disclosure Program closure demonstrated that favourable compliance pathways can disappear suddenly—leaving non-participants exposed to maximum statutory penalties without amnesty eligibility.

Additionally, for individuals with Bermuda HNWI tax liability, the enhanced BMA cooperation with international tax authorities means that historical barriers to information discovery have largely dissolved. Therefore, the traditional assumption that “Bermuda structures provide concealment” no longer reflects 2026 enforcement realities.

Your Next Steps

Consequently, if you face IRS back taxes resolution challenges involving international holdings, multiple unfiled years, or substantial foreign account balances, immediate professional consultation becomes essential. Specifically:

- Request IRS Wage & Income Transcripts for all potentially unfiled years to understand what the IRS already knows

- Conduct preliminary financial inventory identifying all foreign accounts, entities, and beneficial ownership interests

- Engage qualified international tax counsel with Bermuda-US tax coordination expertise

- Obtain objective willfulness assessment determining optimal programme selection

- Initiate comprehensive voluntary disclosure before IRS contact to secure criminal protection

Ultimately, the difference between successful IRS back taxes resolution preserving wealth and catastrophic outcomes destroying it lies in professional guidance versus Reddit’s well-intentioned but fundamentally flawed crowdsourced advice. Therefore, for high-net-worth individuals, professional representation represents not discretionary expense but essential wealth preservation investment.

Professional Disclaimer

Jurisdictional Limitations: This guide provides educational information regarding US federal tax compliance and should not be construed as legal, tax, or financial advice applicable to individual circumstances. Tax law varies substantially across jurisdictions, with material differences between federal and state requirements, international tax treaty provisions, and foreign country obligations creating complexity requiring individualised professional analysis.

Jurisdictional Limitations: This guide provides educational information regarding US federal tax compliance and should not be construed as legal, tax, or financial advice applicable to individual circumstances. Tax law varies substantially across jurisdictions, with material differences between federal and state requirements, international tax treaty provisions, and foreign country obligations creating complexity requiring individualised professional analysis.

No Professional Relationship: Nothing contained herein creates an attorney-client relationship, accountant-client relationship, or any professional advisory relationship between readers and the author or affiliated entities. Readers should not transmit confidential information without first establishing formal engagement agreements with qualified practitioners operating within applicable regulatory frameworks.

Information Currency: Whilst every effort has been made to ensure accuracy as of January 2026, tax law evolves continuously through legislation, regulation, administrative guidance, and judicial decisions. The Voluntary Disclosure Practice penalty framework modifications subject to public comment through 22 March 2026 may substantially alter compliance programme parameters. Readers must verify current law with qualified professionals before implementing strategies.

Bermuda Context: This guide is authored from a Hamilton, Bermuda perspective by professionals advising US persons on US tax obligations. Bermuda’s zero-income-tax status creates particular complexity for US citizens and residents, as foreign tax credits provide limited benefit when minimal foreign taxes are paid. Such individuals must prioritise Foreign Earned Income Exclusion optimisation and engage professionals familiar with US-Bermuda tax coordination.

Regulatory Compliance: Services requiring licensure (legal representation, tax return preparation, investment advice) must be provided only by appropriately credentialed professionals operating within regulatory frameworks of relevant jurisdictions including IRS Circular 230 (US tax practice), state bar associations (legal practice), state boards of accountancy (CPA practice), and SEC/FINRA regulations (investment advice).

External Resources: Recommended authoritative sources include: Internal Revenue Service (www.irs.gov), FinCEN (www.fincen.gov), US Department of State (www.travel.state.gov), Bermuda Monetary Authority (www.bma.bm), Bermuda Government (www.gov.bm). Readers must independently verify all information through primary sources.

Professional Representation Recommendation: Given severe consequences associated with IRS back taxes resolution errors—including six-figure penalties, criminal prosecution, asset seizure, and passport revocation—readers are strongly urged to engage qualified professional representation rather than relying exclusively on self-research or anonymous internet advice.