You moved to Bermuda. No income tax. Good salary. Life is good.Then your accountant asks: “Are you still funding your Roth IRA?” You say yes. She winces. Turns out the foreign earned income exclusion (FEIE) you claimed last year may have quietly wiped out your Roth IRA Bermuda rules eligibility entirely, and you contributed anyway. Now you have an excess contribution sitting in your account, and the IRS charges 6% per year on that until you fix it. This happens more than people admit. So here’s exactly how the rules work for 2026, what the FEIE trap looks like in practice, and how to stay eligible without leaving money on the table.

Roth IRA Bermuda rules that still apply to you as a US citizen

US citizenship follows you everywhere. The IRS doesn’t care that Bermuda has zero personal income tax. You’re still a US taxpayer on worldwide income, which means every Roth IRA rule that applies to someone in Chicago applies to you in Hamilton. The IRS lays out every contribution rule, income limit, and withdrawal condition on the official IRS Roth IRA rules page.

Table: 2026 Roth IRA rules and amounts:

| Rule | Amount |

| Contribution limit (under 50) | $7,000 |

| Contribution limit (50 or older) | $8,000 |

| Income limit: full contribution (single) | MAGI below $150,000 |

| Income limit: phase-out (single) | $150,000 to $165,000 |

| Income limit: no contribution (single) | Above $165,000 |

| Income limit: full contribution (married filing jointly) | MAGI below $236,000 |

| Income limit: phase-out (married filing jointly) | $236,000 to $246,000 |

| Income limit: no contribution (married filing jointly) | Above $246,000 |

| Contribution deadline | April 15, 2027 |

Two conditions must be true before you contribute a single dollar. You need qualifying earned income at least equal to your contribution. And your MAGI must stay within the limits above.

Bermuda creates a problem with both.

The foreign earned income exclusion Roth IRA eligibility trap

This is the one that catches people.

The FEIE lets you exclude up to $126,500 of foreign earned income from your US federal tax return for 2024 (the 2026 figure will be slightly higher after inflation adjustments). It sounds clean: exclude the income, pay less US tax.

But the IRS uses a specific definition of “earned income” for IRA contribution purposes. And under that definition, any income you exclude through the FEIE gets stripped out of your earned income calculation for IRA eligibility.

So if you earn $90,000 in Bermuda and exclude all of it under FEIE: your earned income for Roth IRA purposes is $0. You can’t contribute anything. YourRoth IRA Bermuda rules eligibility is gone for that year.

If you earn $90,000 and exclude $83,000, keeping $7,000 unexcluded: your earned income is $7,000. You can contribute the full $7,000.

That $7,000 of unexcluded income gets taxed at your US marginal rate. For most Bermuda-based expats, that’s 22% on $7,000, which is $1,540 in US federal tax. You’re essentially paying $1,540 to keep your Roth IRA alive for one year.

Whether that’s worth it depends entirely on your time horizon and how much you value tax-free compounding in retirement. The Foreign Earned Income Exclusion lets US expats exclude up to $126,500 of foreign earned income from their US federal tax return.

How MAGI works when you live in Bermuda

Modified adjusted gross income for Roth IRA purposes is calculated differently than you might expect.

The IRS adds your FEIE exclusion back into your MAGI calculation. So even if you excluded $126,500 of income to reduce your federal tax bill, that $126,500 still counts toward your MAGI for Roth IRA income limit purposes.

Table: MAGI calculation example:

| Item | Amount |

| Bermuda salary | $180,000 |

| FEIE exclusion | $126,500 |

| Taxable income after FEIE | $53,500 |

| MAGI for Roth IRA purposes | $180,000 (FEIE added back) |

| Roth IRA eligibility (single filer) | Not eligible (above $165,000) |

So in this case you’d owe little to no US federal tax (thanks to the FEIE), but you’re also completely locked out of direct Roth IRA contributions because your MAGI is $180,000.

The backdoor Roth IRA is the only route left.

Backdoor Roth IRA: what it is and when you need it

If your MAGI is above $165,000 (single) or $246,000 (married), the backdoor Roth is how you get in.

The steps:

Step 1: Open a traditional IRA

Open a traditional IRA. Contribute up to $7,000. Don’t deduct it on your taxes. File Form 8606 to record it as a non-deductible (after-tax) contribution.

Step 2: Wait a few days

Wait a few days. No legal requirement, but it keeps the transaction clean.

Step 3: Convert to Roth IRA

Convert the traditional IRA to a Roth IRA. Your brokerage handles this with a form or a phone call.

Step 4: File Form 8606

File Form 8606 again to document the conversion. This is what tells the IRS you already paid tax on the money and owe nothing on conversion.

The catch: the pro-rata rule

If you have other pre-tax IRA money sitting anywhere (rollover IRA from an old 401k, a SEP-IRA from self-employment), the IRS treats all your IRA money as one pool when you convert. The taxable portion of your conversion gets calculated proportionally. File Form 8606 with your return — full instructions are in IRS Publication 590-A, which covers every IRA contribution and conversion rule.

Cross-Border Brokerage Hurdles from Bermuda

While you may legally qualify for a Roth IRA Bermuda rules under the IRS code, executing this strategy from Bermuda presents distinct practical challenges. Specifically, major U.S. financial institutions like Vanguard, Fidelity, and Charles Schwab strictly monitor compliance with the USA PATRIOT Act alongside local foreign financial regulations. Consequently, if you update your residential profile to a Bermuda address, many brokerages will immediately freeze your ability to open new accounts or make ongoing mutual fund purchases.

To overcome these roadblocks, savvy expats rely on two primary workarounds:

- Interactive Brokers (IBKR): Industry experts widely regard this platform as the friendliest major custodian for international U.S. expats because the firm explicitly accommodates foreign residential addresses.

- Maintain a Domestic Base: Alternatively, many expats retain a permanent U.S. mailing address — such as a trusted family home — tied directly to their financial profiles. Ultimately, this tactic keeps traditional, state-side accounts active and unrestricted.

Table: Pro-rata rule scenarios

| Scenario | Pre-tax IRA balance | After-tax contribution | Conversion taxable % |

| Clean backdoor | $0 | $7,000 | 0% taxable |

| Pro-rata applies | $63,000 | $7,000 | 90% taxable |

| Pro-rata applies | $133,000 | $7,000 | 95% taxable |

The fix for the pro-rata problem: roll your pre-tax IRA money into your current employer’s 401k before doing the backdoor. That clears the pool. Then your $7,000 conversion is 100% tax-free.

Roth IRA vs traditional IRA vs 401k: which one fits a Bermuda expat

Most Bermuda-based US expats overthink this. The accounts aren’t competing — they solve different problems at different income levels.

A traditional IRA gives you a tax deduction now and a tax bill later. A Roth IRA takes the tax hit now and gives you tax-free money in retirement. A 401k does what a traditional IRA does but with a much higher contribution limit and, if your employer offers matching, free money on top.

The FEIE complicates both IRAs. It can wipe out your earned income eligibility entirely, which the 401k doesn’t care about at all.

So the practical answer for most Bermuda expats: contribute to your 401k first up to the employer match, then fund the Roth IRA if you still have qualifying earned income after your FEIE calculation. If your MAGI is above $165,000, skip the direct Roth contribution and run the backdoor route instead.

The table below breaks down exactly where each account wins and where it doesn’t.

Full comparison — Roth IRA vs Traditional IRA vs 401k

| Feature | Roth IRA | Traditional IRA | 401k |

| 2026 contribution limit | $7,000 / $8,000 | $7,000 / $8,000 | $23,500 / $31,000 |

| Tax on contributions | After-tax | Pre-tax | Pre-tax |

| Tax on growth | Tax-free | Tax-deferred | Tax-deferred |

| Tax on withdrawal | Tax-free (qualified) | Taxed as income | Taxed as income |

| Income limit to contribute | Yes | No | No |

| Required minimum distributions | None | Age 73 | Age 73 |

| FEIE reduces eligibility | Yes (earned income) | Yes (earned income) | No |

| Backdoor available | Yes | N/A | No |

| Employer match possible | No | No | Yes |

| Best for | Expecting higher tax in retirement | Expecting lower tax in retirement | Have employer match |

Most Bermuda-based expats with employer-sponsored 401k access should contribute enough to get the full employer match first. Then put $7,000 into a Roth IRA. Then go back to the 401k with whatever’s left.

That sequence captures the free employer money before anything else.

The self-employed expat problem

If you run your own business from Bermuda, the calculation gets messier.

Your net self-employment income counts as earned income for Roth IRA purposes. But you also owe self-employment tax (15.3% on the first $168,600 of net SE income), and you can deduct half of that. That deduction slightly reduces your MAGI.

The sequence:

- Calculate net self-employment income (revenue minus business deductions)

- Deduct half of self-employment tax

- Apply the FEIE if you qualify

- Whatever earned income remains after FEIE is what you can contribute (up to $7,000)

If you exclude all your self-employment income through the FEIE, you’re back to zero earned income for IRA purposes. Same trap, same solution: leave enough unexcluded to fund the contribution, accept the tax cost on that amount. For self-employed expats with income well above the Roth income limits, a Solo 401k often makes more sense. Higher contribution limits ($70,000 total for 2026), and the FEIE income exclusion doesn’t affect 401k eligibility.

What happens if you contributed when you weren’t eligible

The IRS calls this an excess contribution. The penalty is 6% of the excess amount per year, every year the excess stays in the account.

If you contributed $7,000 in 2025 but had zero qualifying earned income (because you excluded everything via FEIE): you have a $7,000 excess contribution. That’s $420 in penalties for 2025. Then another $420 for 2026 if you don’t fix it. And so on.

Table: Excess contribution fix options

| Option | How it works | Deadline |

| Withdraw the excess | Pull out the $7,000 plus any earnings on it | By tax filing deadline (April 15, 2027 for 2026) |

| Recharacterize | Move it to a traditional IRA instead | By tax filing deadline |

| Apply to next year | If you’ll be eligible next year, let it count as a 2027 contribution | Must be eligible next year |

Withdrawing the excess after the deadline means you still pay the 6% penalty for the year(s) it was in the account, plus income tax and a 10% penalty on any earnings you withdraw.

Fix it before April 15. Don’t wait.

Roth IRA withdrawal rules for Bermuda residents in 2026

The rules are the same whether you live in Bermuda or Boston.

Table: Withdrawal rules by type

| Withdrawal type | Age | Tax | Penalty |

| Contributions (your principal) | Any age | None | None |

| Qualified earnings | 59½ or older, account 5+ years old | None | None |

| Early earnings withdrawal | Under 59½ | Yes | 10% |

| First-time home purchase | Any age | None on up to $10,000 | None |

| Disability | Any age | None | None |

| Required minimum distributions | Never | N/A | N/A |

The 5-year clock starts January 1 of the year you make your first Roth contribution, regardless of when in that year you actually contributed. Contribute in December 2022? Your 5-year clock started January 1, 2022. You hit the 5-year mark on January 1, 2027.

After 59½ and 5 years: everything comes out tax-free. That’s the whole point.

No required minimum distributions ever. Your Roth IRA Bermuda rules can sit and compound until you die and pass to heirs. That’s a real advantage over a traditional IRA or 401k, which force you to start pulling money at 73 whether you need it or not.

Roth IRA vs The Bermuda National Pension Scheme (NPS)

If you work in Bermuda for more than a few temporary contract blocks, you will automatically enroll in the local National Pension Scheme (NPS).

Your Earnings in Bermuda:

├──► 1st Priority: Bermuda NPS (Secure Employer Match)

│

└──► 2nd Priority: Roth IRA / Backdoor Roth ($7,500 Cap)

│

└──► Result: Tax-Free U.S. Compounding Growth

While the NPS provides a structured vehicle for your retirement, it simultaneously creates a distinct disadvantage for U.S. citizens. Specifically, the IRS does not recognize the Bermuda NPS as a qualified tax-advantaged account like a domestic 401(k). Consequently, growth inside this local Bermuda pension often triggers complex Passive Foreign Investment Company (PFIC) reporting requirements. Furthermore, these investments can generate unexpected annual tax exposure on your U.S. return.

By contrast, maximizing your Roth IRA Bermuda rules gives you total control over your asset allocation. Ultimately, this strategy secures zero U.S. tax on your investment growth and eliminates Required Minimum Distributions (RMDs) entirely.

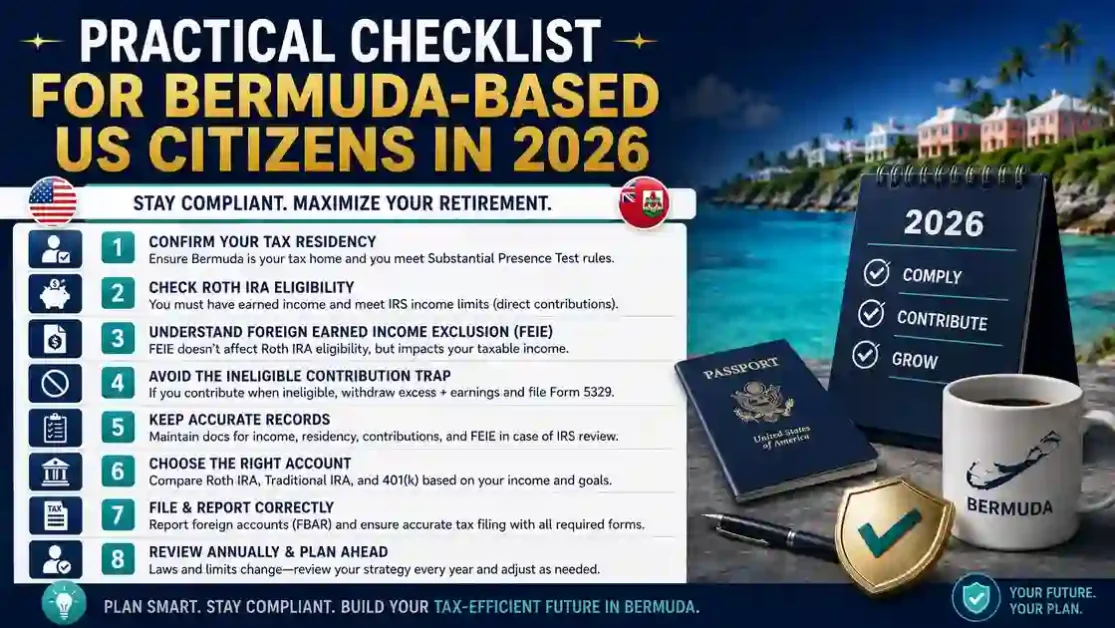

Practical checklist for Bermuda-based US citizens in 2026

Before you contribute to a Roth IRA Bermuda rules this year, run through this:

Pre-contribution checklist

| Check | Question | Action if no |

| Earned income | Do I have US qualifying earned income after FEIE? | Don’t contribute |

| MAGI limit | Is my MAGI below $150,000 (single) or $236,000 (married)? | Use backdoor route |

| Pro-rata risk | Do I have pre-tax IRA balances elsewhere? | Roll to 401k first |

| Excess contribution | Did I over-contribute in a prior year? | Fix before April 15 |

| Brokerage access | Does my brokerage accept my Bermuda address? | Use Interactive Brokers or keep US address |

| Form 8606 | Am I filing Form 8606 for non-deductible contributions? | Add to your return |

| Quarterly estimates | Am I paying IRS quarterly estimated taxes? | Set up EFTPS payments |

The FEIE decision: a real trade-off

Some Bermuda expats choose to partially waive the FEIE specifically to maintain Roth IRA eligibility. It’s a deliberate decision and it makes sense in the right circumstances.

If you earn $60,000 in Bermuda:

Table: FEIE strategy comparison

| FEIE Strategy | Federal tax on unexcluded income | Roth IRA eligibility |

| Exclude all $60,000 | $0 | Not eligible (zero earned income) |

| Exclude $53,000, keep $7,000 | ~$1,540 (22% bracket) | Eligible for full $7,000 contribution |

| Exclude nothing | Taxed on full $60,000 | Eligible, but larger US tax bill |

Paying $1,540 in tax to fund a $7,000 Roth IRA Bermuda rules contribution that grows tax-free for 25 years is probably worth it for most people under 45. After that, you’re looking at a shorter compounding window and the math gets closer.

I’d probably still do it at 50. Maybe not at 60.

FAQ: Roth IRA rules for US citizens in Bermuda

- Can I open a Roth IRA from Bermuda?

Yes, if you have a US brokerage account. Most major brokers (Fidelity, Vanguard, Schwab) won’t open new accounts for people with a foreign address on file. Keep a US mailing address or use Interactive Brokers, which explicitly serves international clients.

- Does the FEIE affect my 401k eligibility?

No. The FEIE exclusion doesn’t reduce your 401k contribution eligibility. You can contribute fully to a 401k regardless of how much foreign income you exclude.

- What if I'm married and one spouse has no income?

A spousal Roth IRA lets you contribute on behalf of a non-working spouse, as long as the working spouse has enough earned income to cover both contributions. The income limits still apply based on your combined MAGI.

- Can I contribute to both a Roth IRA and a 401k?

Yes. The contribution limits are separate. You can max out a 401k at $23,500 and still contribute $7,000 to a Roth IRA in the same year, as long as you meet the Roth income requirements.

- What's the contribution deadline for the 2026 tax year?

April 15, 2027. Filing an extension doesn’t extend this deadline.

Disclaimer:

This article covers general tax information for US citizens living in Bermuda. Your specific situation depends on your income, filing status, FEIE elections, and IRA history. Work with a CPA who specializes in US expat taxation before making any contribution or conversion decisions.