Your Form 1120 Corporate Tax Return deadline is approaching fast.The IRS enforces steeper penalties than ever in 2026. After 18 years of working with corporations, I have watched the same costly errors repeat year after year. Missed deadlines drain money.Overlooked credits cost thousands. Misclassified income triggers audits. Every one of these mistakes is avoidable. This guide will help you prevent all of them before they damage your business financially.

Think of IRS Form 1120 as your corporation’s annual financial biography.You submit it directly to the federal government each year. It tells the IRS how much your business earned, what it spent, and what it owes. Specifically, it must capture every income source, every deductible expense, and every qualifying credit. According to the official IRS Instructions for Form 1120 (2025), corporations must file this return accurately and on time. All required schedules must accompany the submission. No exceptions apply.

What Is IRS Form 1120? Understanding the 1120 US Corporation Income Tax Return

IRS Form 1120 is the U.S. Corporation Income Tax Return.Corporations use it to report income, gains, losses, deductions, and credits each year. Additionally, it serves as the primary compliance document that C corporations submit to the federal government. It also determines exactly how much federal tax the corporation owes. Furthermore, it identifies any overpayment the corporation may carry forward to future years.

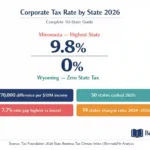

💡 Quick Tool: Calculating taxes manually across 50 states is complex. Use our State Corporate Tax 2026: 50-State Rates & Calculator to get instant results for your C Corp filing.

The form demands far more than simple number entry. Rather, it requires a comprehensive accounting of your corporation’s full financial activity. You must attach supporting schedules and reconciliation statements simultaneously. In many cases, you must also include additional disclosure forms. Think of it as a detailed financial audit of your business, and the IRS reads every single line with precision.

Purpose and Legal Foundation of Form 1120

C corporations exist as legally distinct taxpaying entities under U.S. law. Unlike sole proprietors or partners, a C corporation’s income does not flow through to the owners’ personal returns. Consequently, the corporation itself pays tax directly to the IRS. Officers must file the Annual Corporate Tax Return independently to account for all taxable activity. This legal separation creates both planning opportunity and direct compliance obligation for every C corporation.

The IRS uses Form 1120 to verify correct income reporting. It also checks that corporations pay the appropriate tax amount. Furthermore, it confirms that corporations claim only legally entitled deductions and credits. From an enforcement standpoint, Form 1120 additionally serves as the primary gateway for audit selection.Accuracy and completeness are therefore non-negotiable for any corporation filing the Federal Corporate Tax Return.

How the 1120 Corporation Return Differs From Other Tax Forms

Understanding which form your business must file is a legal requirement. The 1120 Corporation return applies exclusively to C corporations. These are entities taxed under Subchapter C of the Internal Revenue Code. S corporations, by contrast, file Form 1120-S as pass-through entities. Partnerships file Form 1065. Sole proprietors report business income on Schedule C attached to personal Form 1040.

Filing the wrong form does not pause the IRS penalty clock. The agency treats it as a failure to file from day one. Penalties begin accruing immediately thereafter. The IRS makes no distinction between accidental errors and deliberate omissions when assessing the initial penalty.

Who Must File an 1120 Corporation Return in 2026?

Every domestic C corporation organized under U.S. law must file a Business Federal Tax Return using Form 1120. Critically, this requirement does not depend on profitability at all. Even if a corporation had no taxable income, it may still need to file to remain compliant with IRS requirements. SDO CPA LLC Zero revenue does not equal zero filing obligation.A corporation showing zero income still confirms to the IRS that the entity was inactive. Skipping the filing is never an option, even for dormant corporations.

The filing requirement covers C corporations of all sizes equally. A pre-revenue startup incorporated in Delaware must file Form 1120. Similarly, a profitable manufacturing firm with $10 million in revenue must also file. Additionally, a corporation that operated for only six months must file a short-year Form 1120 for that period.The form scales in complexity based on financial activity.Nevertheless, the obligation to file never disappears, regardless of how slow business may have been.

Entities That Must File and Entities That Are Exempt

The IRS Form 1120 requirement covers domestic C corporations. It also applies to certain foreign corporations with income effectively connected to a U.S. trade or business. Personal holding companies additionally fall under this requirement. However, several specific entities file different returns instead. S corporations file Form 1120-S. Tax-exempt organizations under Section 501 file Form 990. Real estate investment trusts file Form 1120-REIT. Life insurance companies file Form 1120-L.

The entity’s legal structure not its revenue type or industry,determines which return it must file.Consequently, corporations with a valid S-corp election under Section 1362 must file Form 1120-S instead of Form 1120. Filing the wrong form, even accidentally, can result in penalties.The IRS calculates those penalties as though the corporation filed no return at all.

2026 Federal Corporate Tax Rates and What They Mean for Your Business

The federal corporate income tax rate for 2026 filings remains a flat 21% on all taxable income.This rate applies equally to all C corporations, regardless of size or annual revenue. Unlike the graduated brackets for individuals, there are no federal tiers for corporations. Every additional dollar of taxable income costs exactly 21 cents in federal tax. That is the full story at the federal level.

The Flat 21% Rate and Its Strategic Implications for Your Federal Corporate Tax Return

That flat structure simplifies rate planning considerably. You always know your marginal rate with certainty. Income fluctuations during the year change the total tax bill — but never the rate itself. However, this structure removes the bracket-threshold strategies that individual taxpayers often use. As a result, the entire tax minimization strategy for C corporations shifts to a different set of tools entirely.

Specifically, corporations must focus on maximizing deductions, capturing every available credit, and timing income recognition intelligently.The One Big Beautiful Bill Act, signed on July 4, 2025, created new Section 1062 regarding the gain from the sale or exchange of qualified farmland property to qualified farmers. It allows taxpayers to elect to pay the net income tax attributable to such gains in four equal annual installments. SDO CPA LLC Furthermore, state corporate income taxes add a significant layer on top of the federal 21%. Most states impose their own corporate tax, with rates varying dramatically by jurisdiction.Consequently, federal planning without simultaneous state tax planning remains inherently incomplete.

Key Deadlines and Penalties for the 2026 Form 1120 Corporate Tax Return

Filing your Form 1120 Corporate Tax Return on time is non-negotiable. Form 1120 is due on the 15th day of the 4th month after the end of the corporation’s tax year. Corporations with a short tax year ending on June 30, 2026, must file by September 15, 2026. They may use Form 7004 to request an automatic 7-month extension of time to file. Internal Revenue Service.

| Filing Situation | Deadline | Extension Available |

| Calendar-year C-Corps (Dec 31 FYE) | April 15, 2026 | October 15, 2026 via Form 7004 |

| Fiscal-year C-Corps (standard) | 15th day of 4th month after FYE | 6-month extension via Form 7004 |

| Fiscal-year C-Corps (June 30 FYE) | September 15, 2026 | 7-month extension via Form 7004 |

| Estimated Tax — Q1 2026 | April 15, 2026 | No extension available |

| Estimated Tax — Q2 2026 | June 15, 2026 | No extension available |

| Estimated Tax — Q3 2026 | September 15, 2026 | No extension available |

| Estimated Tax — Q4 2026 | December 15, 2026 | No extension available |

💡 Quick Tool: Calculating taxes manually across 50 states is complex. Use our State Corporate Tax 2026: 50-State Rates & Calculator to get instant results for your C Corp filing.

Late Filing vs Late Payment Penalties:Know the Critical Difference

The IRS punishes failure to file far more harshly than failure to pay. A corporation that does not file its tax return by the due date may face a penalty of 5% of the unpaid tax for each month or part of a month the return is late, up to a maximum of 25% of the unpaid tax. The minimum penalty for a return required to be filed in 2026 that is more than 60 days late is the smaller of the tax due or $525. SDO CPA LLC

The late-payment penalty, by comparison, runs at only 0.5% per month.That is significantly softer — but it still compounds daily. Interest on unpaid balances currently runs at 7% annually. Large corporations owing more than $100,000 face a higher interest rate — typically 2% above the standard rate after receiving a final IRS notice. Carta Always pay your estimated tax by April 15. Do this even when you file an extension.The extension covers paperwork only — never the tax payment itself.

Why the Extension Rule Catches So Many Business Owners Off Guard

Many corporations file Form 7004 and then assume they have more time to pay.This assumption is wrong, and it is expensive. An automatic extension only grants more time to file the paperwork. It does not grant more time to pay the tax. To avoid payment penalties during the extension period, pay your estimated tax balance by the original April deadline. Carta Every day you delay payment beyond April 15, interest and the late-payment penalty keep compounding separately. This distinction trips up experienced business owners every single year. Do not let it trap your corporation in 2026.

Step-by-Step Breakdown of Form 1120 Sections

💡 Quick Tool: Calculating taxes manually across 50 states is complex. Use our State Corporate Tax 2026: 50-State Rates & Calculator to get instant results for your C Corp filing.

Filing Form 1120 for the first time can feel overwhelming.The form runs multiple pages. Required schedules can add dozens of additional pages for complex corporations. Understanding the logical structure, however, transforms this intimidating document into a manageable workflow. Here is precisely how the key sections fit together for your Annual Corporate Tax Return.

Page 1 of the Form 1120 Corporate Tax Return — Income and Identifying Information

Page 1 begins with your corporation’s identifying information. You enter your legal name, EIN, date of incorporation, state of incorporation, and total assets at year-end.These figures must match your articles of incorporation and prior-year returns exactly.Any discrepancy at the identification level delays processing immediately and can trigger manual IRS review.

The income section — Lines 1 through 11 — captures all revenue sources.This includes gross receipts (Line 1a), cost of goods sold (Line 2), gross profit (Line 3), dividends received (Line 4), interest income (Line 5), rents (Line 6), royalties (Line 7), capital gains (Line 8), and other income (Lines 9–10).Every line must reconcile perfectly to your financial statements.Omitting even small income categories — such as business savings account interest, frequently triggers IRS notices and follow-up inquiries.

Deductions Section — Where Legitimate Tax Reduction Happens on Your Business Federal Tax Return

The deductions section — Lines 12 through 29 — is where real tax savings happen. You can claim officer compensation (Line 12), wages and salaries (Line 13), repairs (Line 14), bad debts (Line 15), rent (Line 16), taxes and licenses (Line 17), interest expense (Line 18), charitable contributions (Line 19), depreciation (Line 20), advertising (Line 22), pension contributions (Line 23), and employee benefit programs (Line 24). Each category carries specific rules and documentation requirements under the Internal Revenue Code.

Claiming a deduction without adequate substantiation is not aggressive planning — it is an audit invitation. If you lack a receipt or contract supporting a deduction, the IRS will disallow it entirely.Maintain all documentation throughout the year.Do not wait until filing time to gather records.

Schedules and Supplementary Forms Required With Form 1120

Beyond Page 1, several key schedules are required depending on your corporation’s financial profile.Schedule L provides the corporation’s balance sheet as of the beginning and end of the tax year. Corporations with $10 million or more in total assets must file Schedule M-3. This schedule answers questions about financial statements and reconciles net income or loss to taxable income reported on Form 1120. SDO CPA LLC

Furthermore, complete every applicable entry space on Form 1120. Do not enter “See Attached” or “Available Upon Request” instead of completing the actual entry spaces. SDO CPA LLC A technically deficient return may be treated as unfiled.Consequently, the failure-to-file penalty clock keeps running even after the corporation submits the incomplete document. This is a critically important rule that many preparers overlook under deadline pressure.

Essential Documents for Your Business Federal Tax Return

Smart corporations begin gathering documents in January.That is the moment the tax year closes. Waiting until March or April creates dangerous time pressure.That pressure consistently results in missed deductions and documentation gaps.Consequently, early preparation delivers one of the highest returns on invested time before filing season begins.

| Document Category | Specific Items Required |

| Financial Statements | Year-end income statement, balance sheet, general ledger trial balance |

| Revenue Records | Gross receipts, sales invoices, 1099-K statements from payment processors |

| Expense Documentation | Receipts, invoices, and contracts for all deducted expenses |

| Payroll Records | W-2s, Form 941s, officer compensation breakdown, payroll summaries |

| Asset & Depreciation | Fixed asset schedule, purchase/disposal records, Form 4562 workpapers |

| Banking & Investments | Year-end bank statements, brokerage statements, 1099-DIV and 1099-INT |

| Prior-Year Returns | Last year’s Form 1120 for NOL carryforward amounts and comparison |

| Ownership Records | Cap table, stock ledger, documentation of any ownership changes |

| Foreign Activity | Foreign income documentation, Form 5471 if applicable |

| Credits & Special Items | R&D expense records, energy credit documentation, Form 3800 workpapers |

Why Document Organization Directly Impacts Your Tax Liability on the Federal Corporate Tax Return

Getting organized early accomplishes far more than reducing stress. It gives your CPA adequate time to identify planning opportunities. It also allows time to catch errors and request missing information.Specifically, corporations that scramble at the last minute consistently leave legitimate deductions unclaimed. Documentation was simply unavailable at filing time. Additionally, a well-organized file dramatically reduces audit risk. Clean, reconciled records signal to the IRS that your return reflects careful and professional preparation throughout the year.

C-Corp vs S-Corp Filing: Why Form 1120 Matters for Your Business Structure

The difference between filing Form 1120 and Form 1120-S reflects a fundamental difference in how your business pays tax. A C corporation pays a flat 21% federal tax on profits at the entity level directly. Shareholders then face tax again on their personal returns when they receive dividends.This is the well-known “double taxation” characteristic of C-corp status. By contrast, an S corporation pays no federal entity-level tax at all. Instead, profits pass through directly to shareholders.Shareholders then report them on personal returns at rates from 10% to 37%.

Despite the double-taxation concern, C-corp status carries significant advantages. Retained earnings reinvest in the business at the 21% corporate rate. That rate is substantially lower than the top individual rate of 37%. This creates a meaningful tax deferral advantage for growth-oriented businesses specifically. Additionally, C-corps carry no restrictions on the number or type of shareholders.They also support multiple classes of stock. Consequently, businesses planning to pursue venture capital or a public offering must operate as C-corps. There is essentially no alternative structural path for those businesses.

How to Reduce Your Federal Corporate Tax Liability Legally in 2026

Reducing your Federal Corporate Tax Return liability is entirely legal. You achieve it through IRS-sanctioned deductions, credits, and timing strategies. The most impactful tools available to C corporations in 2026 include accelerated depreciation on qualifying capital investments. Furthermore, the R&D tax credit under Section 41 provides a dollar-for-dollar tax reduction, not merely a deduction against income.The Section 179 immediate expensing election also allows qualifying business assets to be deducted fully in the year of purchase. Strategic timing of income and expense recognition across tax years rounds out the core toolkit.

Retirement plan contributions represent a significantly underutilized opportunity for closely held C corporations.Contributions to qualified plans, including defined benefit pension plans, 401(k) plans, and SEP-IRAs — are fully deductible by the corporation.Simultaneously, these contributions provide tax-advantaged savings for owner-employees. Charitable contributions are additionally deductible up to 10% of taxable income. Any unused excess carries forward for five years. Working with an experienced CPA who specializes in corporate tax is consequently not an expense — it consistently generates measurable, real-dollar savings that most business owners would otherwise miss entirely.

Common Mistakes to Avoid When Filing Form 1120 Corporate Tax Return

After nearly two decades of preparing corporate tax returns, the same errors surface repeatedly. Proper preparation and professional guidance prevent almost all of them. Here are the most costly mistakes and exactly how to avoid each one.

Misclassifying owner compensation

Ranks among the most scrutinized issues on Form 1120. Officers must report their salaries separately on Schedule E. The IRS closely examines whether that compensation is reasonable relative to services actually provided. Paying a sole officer zero salary while taking large distributions raises an immediate red flag. The IRS actively looks for payroll tax avoidance patterns in closely held corporations and it finds them regularly.

Failing to reconcile book income to taxable income

On Schedule M-1 or M-3 is another expensive and common mistake. GAAP financial statements differ from tax accounting in key areas. Specifically, depreciation methods, revenue recognition timing, and treatment of prepaid expenses diverge significantly. Unexplained book-to-tax differences on Schedule M-1 consequently rank as one of the most reliable audit triggers in corporate tax examination.They frequently result in time-consuming correspondence that disrupts normal business operations for months.

Missing quarterly estimated tax payments

Traps corporations into penalties even when they ultimately file on time. C-corporations expecting to owe $500 or more must make payments by April 15, June 15, September 15, and December 15.Each quarter runs independently of the others. Catching up in a later quarter does not retroactively erase the penalty from an earlier missed installment. Furthermore, the penalty for each missed quarter compounds separately throughout the full year, making early quarters especially costly to miss.

Overlooking available tax credits

Perhaps the most expensive mistake in pure dollar terms.The R&D credit, the general business credit (Form 3800), energy efficiency incentives, and employment-based credits are all available to qualifying corporations. However, claiming them requires documentation gathered throughout the year, not just at filing time. Many corporations consequently leave these credits unclaimed simply because their preparer lacked the required contemporaneous records to support the claim.

Filing an incomplete return

Technical error that many preparers overlook under deadline pressure. Specifically, do not enter “See Attached” or “Available Upon Request” instead of completing the actual entry spaces on Form 1120. SDO CPA LLC The IRS may treat an incomplete return as unfiled. Consequently, the failure-to-file penalty clock keeps running even after submission, costing the corporation additional money every single month.

Conclusion:Take Full Control of Your Form 1120 Corporate Tax Return in 2026

The Form 1120 Corporate Tax Return is the most important annual compliance document your C corporation produces. Critically, it is also one of the most powerful tax planning tools available.Treat it as a strategic exercise, not a last-minute obligation. With the federal corporate tax rate firmly at 21% and legislative stability now in place following the One Big Beautiful Bill Act, the primary opportunity for reducing your tax bill lies in maximizing legitimate deductions, capturing every available credit, and making smart timing decisions consistently throughout the year.

For calendar-year C-corporations, the Form 1120 deadline is April 15, 2026.Filing Form 7004 extends that deadline to October 15, 2026. However, that extension covers only the paperwork, not the tax payment itself. Carta Start gathering your financial records now. Review your quarterly estimated payments carefully. Above all, work with a qualified CPA or enrolled agent who specializes in corporate tax compliance.Engage them well before deadline pressure begins to build in March and April.

Professional recommendation from 10years of corporate tax practice:

Schedule your corporate tax planning meeting no later than February of each year.Use that session to review financial statements, project tax liability, and identify deduction and credit opportunities.Confirm your full filing calendar at that same meeting. Proactive planning always costs less in time, money, and stress than reactive problem-solving after an IRS notice arrives.

For personalized guidance on your corporation’s Form 1120 filing, consult a licensed CPA or enrolled agent with documented expertise in U.S. corporate tax law. The IRS also provides free official resources at IRS.gov/corporations.

FAQ: About the Form 1120 Corporate Tax Return

- 1. What is Form 1120 and who must file it in 2026?

Form 1120 is the U.S. Corporation Income Tax Return. Corporations use it to report income, deductions, credits, and tax owed to the IRS annually. Even if a corporation had no taxable income, it may still need to file to remain compliant with IRS requirements. SDO CPA LLC Every domestic C corporation must file it each year, regardless of income level, profitability, or business activity during the period.

- 2. What is the Form 1120 filing deadline for 2026?

Form 1120 is due on the 15th day of the 4th month after the end of the corporation’s tax year. Internal Revenue Service For calendar-year C-corporations, that means April 15, 2026. Corporations with a short tax year ending on June 30, 2026, must file by September 15, 2026, and may use Form 7004 to request an automatic 7-month extension of time to file. Internal Revenue Service

- 3. What penalties apply for filing Form 1120 late in 2026?

A corporation that does not file its tax return by the due date may face a penalty of 5% of the unpaid tax for each month or part of a month the return is late, up to a maximum of 25% of the unpaid tax. The minimum penalty for a return required to be filed in 2026 that is more than 60 days late is the smaller of the tax due or $525. The IRS will not impose the penalty if the corporation can show that the failure to file on time was due to reasonable cause. SDO CPA LLC

- 4. Does filing Form 7004 give more time to pay corporate taxes?

No — and this is one of the most dangerous misconceptions in corporate tax planning. An automatic extension only grants more time to file the paperwork. It does not grant more time to pay the tax. Pay your estimated tax balance by the original April deadline to avoid payment penalties during the extension period. Carta Interest and late-payment penalties begin accruing immediately on any unpaid balance after April 15 — regardless of your extended filing deadline.

- 5. Can a C corporation skip filing Form 1120 if it had no income?

Absolutely not. Even if a corporation had no taxable income, it may still need to file Form 1120 to remain compliant with IRS requirements. SDO CPA LLC A zero-income return confirms to the IRS that the corporation was inactive during the period. Failure to file — even a zero-income return — triggers the same failure-to-file penalties. The IRS applies those penalties to inactive corporations with the same force it applies to profitable ones.

Official IRS References:

- IRS Form 1120 Instructions (2025)

- IRS Publication 509 — Tax Calendars (2026)

- IRS Publication 542 — Corporations

- IRS Failure-to-File Penalty Information

- IRS Corporations Tax Center

💡 Quick Tool: Calculating taxes manually across 50 states is complex. Use our State Corporate Tax 2026: 50-State Rates & Calculator to get instant results for your C Corp filing.

Pingback: Unfiled Taxes Consequences: 10 Years Reddit Legal Advice ✓