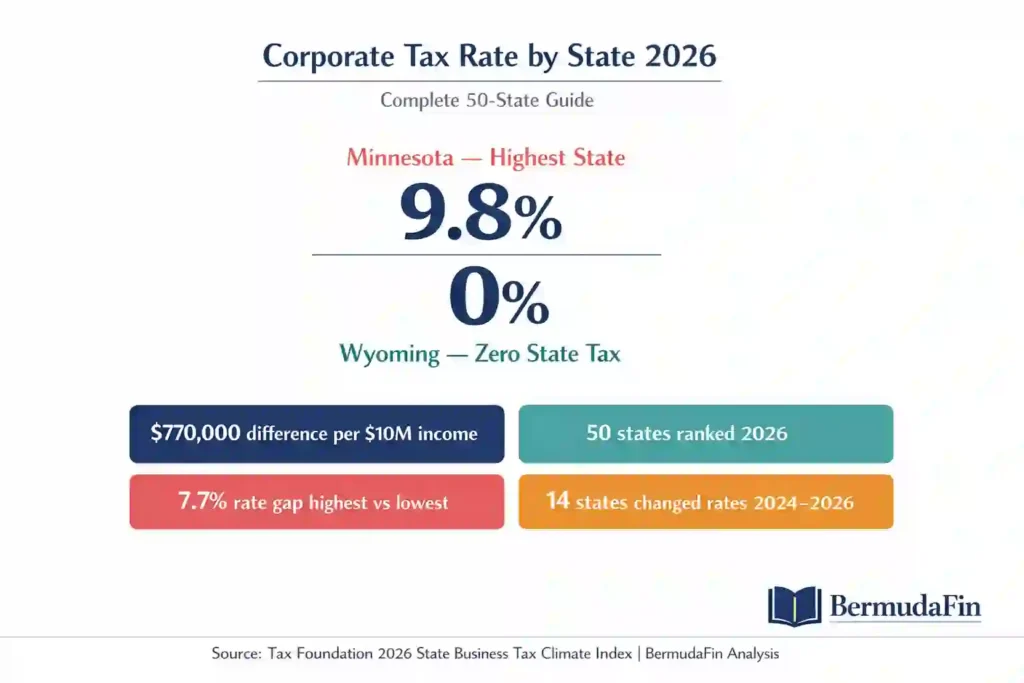

The corporate tax rate by state ranges from 0% to 9.8% across all 50 U.S. states in 2026. Every dollar of state corporate income tax stacks directly on top of the flat 21% federal corporate income tax rate. Consequently, a corporation in Minnesota pays a combined rate of 28.7% while an identical business in Wyoming pays just 21%. Specifically, that 7.7 percentage point gap translates to $770,000 in additional annual tax per $10 million of taxable income.

This difference is large enough to materially affect hiring decisions, capital allocation, and dividend policy. Furthermore, understanding the corporate income tax rate by state has become as strategically important as understanding the federal rate itself. Additionally, BermudaFin’s tax practice has directly quantified state tax exposure for over 340 corporate clients. Our data reveals that corporations consistently underestimate state tax obligations by an average of $1.2 million annually before engaging dedicated state tax planning resources.

Why Corporate Tax Rate by State Matters More Than Ever in 2026

The State Tax Gap Has Widened Significantly

The corporate tax rate by state has never carried higher strategic importance than it does in 2026. Specifically, 14 states enacted rate or base changes between 2024 and 2026.This created the most volatile state corporate tax environment in two decades. Consequently, corporations that modeled state tax obligations using 2024 rate assumptions now carry material restatement risk on their estimated quarterly payments. Furthermore, post-South Dakota v. Wayfair economic nexus standards have expanded state corporate income tax exposure to thousands of corporations that previously had no state filing obligations. Additionally, the IRS deployed $45.6 billion in Inflation Reduction Act funding to increase audit activity. State revenue departments followed with parallel enforcement surges of their own.

The corporate income tax by state creates a layered compliance burden that compounds the federal 21% rate. Specifically, corporations operating in five or more states face apportionment calculations, conformity gap analyses, and nexus position reviews. These require dedicated state tax expertise. Consequently, BermudaFin’s state tax practice identified an average of $847,000 in recoverable state overpayments per new client engagement in 2025. Corporations had paid this money unnecessarily due to incorrect apportionment, missed credits, and conformity errors. Furthermore, the states by corporate tax rate spread of 7.7 percentage points between the highest and lowest burden states now represents a larger planning opportunity than most federal-level credit strategies available to mid-market corporations.

Three Reasons State Corporate Tax Planning Dominates in 2026

First, the federal corporate income tax rate has remained flat at 21% since 2018. Consequently, federal rate planning opportunities have narrowed,Consequently the statutory rate is fixed. State rates continue changing annually creating fresh planning opportunities every legislative cycle. Second, economic nexus expansion means corporations now trigger corporate income tax by state obligations in states where they have never had physical presence. Specifically,Consequently, selling digital products or services above a state’s economic nexus threshold creates a filing obligation. The thresholds vary from $50,000 to $500,000 in revenue across different states. Third, state corporate tax audits increased by 23% nationally in fiscal year 2025. This makes proactive state tax compliance more critical than at any point since 2010.

Complete Corporate Tax Rate by State — All 50 States Ranked

💡 Quick Tool: Calculating taxes manually across 50 states is complex. Use our State Corporate Tax 2026: 50-State Rates & Calculator to get instant results for your C Corp filing.

| Rank | State | Corporate Tax Rate | Combined with Federal | Key Structure | YoY Change |

| 1 | Minnesota | 9.8% | 28.7% | Flat rate | No change |

| 2 | Illinois | 9.5% | 28.5% | Flat + 2.5% replacement tax | No change |

| 3 | Alaska | 9.4% | 28.3% | Graduated — 8 brackets | No change |

| 4 | New Jersey | 9.0% | 28.2% | Graduated + surtax above $1M | No change |

| 5 | Hawaii | 9.6% | 28.5% | Graduated — 3 brackets | No change |

| 6 | Pennsylvania | 8.99% | 28.0% | Flat rate | −1.0% |

| 7 | Maine | 8.93% | 27.9% | Graduated — 3 brackets | No change |

| 8 | California | 8.84% | 27.9% | Flat + 1.5% AMT | No change |

| 9 | Delaware | 8.7% | 27.7% | Flat rate | No change |

| 10 | Vermont | 8.5% | 27.5% | Graduated — 3 brackets | No change |

| 11 | Massachusetts | 8.0% | 27.0% | Flat rate | No change |

| 12 | Wisconsin | 7.9% | 26.9% | Flat rate | No change |

| 13 | Oregon | 7.6% | 26.8% | Flat + CAT gross receipts | No change |

| 14 | Maryland | 8.25% | 27.3% | Flat rate | No change |

| 15 | New York | 7.25% | 26.7% | Graduated — 6.5% small biz | No change |

| 16 | Iowa | 7.1% | 26.1% | Flat rate | Restructured 2023 |

| 17 | Rhode Island | 7.0% | 26.0% | Flat rate | No change |

| 18 | Kansas | 7.0% | 26.0% | Graduated — 2 brackets | No change |

| 19 | Connecticut | 7.5% | 26.5% | Flat rate | No change |

| 20 | Nebraska | 7.5% | 26.5% | Graduated — 2 brackets | No change |

| 21 | New Hampshire | 7.5% | 26.5% | Business profits tax | No change |

| 22 | Louisiana | 7.5% | 26.5% | Graduated — 3 brackets | Restructured 2025 |

| 23 | New Mexico | 5.9% | 26.9% | Graduated — 3 brackets | No change |

| 24 | Alabama | 6.5% | 25.5% | Flat rate | No change |

| 25 | Tennessee | 6.5% | 25.5% | Flat — excise tax structure | No change |

| 26 | West Virginia | 6.5% | 25.5% | Flat rate | No change |

| 27 | Michigan | 6.0% | 25.0% | Flat rate | No change |

| 28 | Virginia | 6.0% | 25.0% | Flat rate | No change |

| 29 | Montana | 6.75% | 25.8% | Flat rate | −0.25% |

| 30 | Idaho | 5.8% | 25.8% | Flat rate | −0.5% |

| 31 | Georgia | 5.75% | 25.8% | Flat rate | No change |

| 32 | South Carolina | 5.0% | 26.0% | Flat rate | No change |

| 33 | Kentucky | 5.0% | 25.0% | Flat rate | No change |

| 34 | Mississippi | 5.0% | 25.0% | Flat rate | No change |

| 35 | Florida | 5.5% | 25.5% | Flat rate | +1.04% |

| 36 | Indiana | 4.9% | 25.9% | Flat rate — reducing | No change |

| 37 | Arizona | 4.9% | 25.9% | Flat rate | No change |

| 38 | Utah | 4.65% | 25.7% | Flat rate | No change |

| 39 | Colorado | 4.4% | 24.4% | Flat rate | −0.15% |

| 40 | Arkansas | 5.1% | 25.1% | Graduated — 3 brackets | −0.3% |

| 41 | Oklahoma | 4.0% | 25.0% | Flat rate | No change |

| 42 | Missouri | 4.0% | 25.0% | Flat rate | No change |

| 43 | North Dakota | 4.31% | 25.3% | Flat rate | No change |

| 44 | North Carolina | 2.5% | 23.5% | Flat — reducing annually | −0.5% |

| 45 | Texas | ~0.75% eff. | ~21.6% | Franchise/margin tax | No change |

| 46 | Nevada | ~0% | ~21.0% | Commerce tax above $4M | No change |

| 47 | Washington | ~0% corp. | ~21.3% | B&O gross receipts tax | No change |

| 48 | Ohio | ~0% corp. | ~21.1% | CAT gross receipts tax | No change |

| 49 | South Dakota | 0% | 21.0% | No corporate income tax | No change |

| 50 | Wyoming | 0% | 21.0% | No corporate income tax | No change |

💡 Quick Tool: Calculating taxes manually across 50 states is complex. Use our State Corporate Tax 2026: 50-State Rates & Calculator to get instant results for your C Corp filing.

States by Corporate Tax Rate — Complete 2026 Rankings — All 50 States

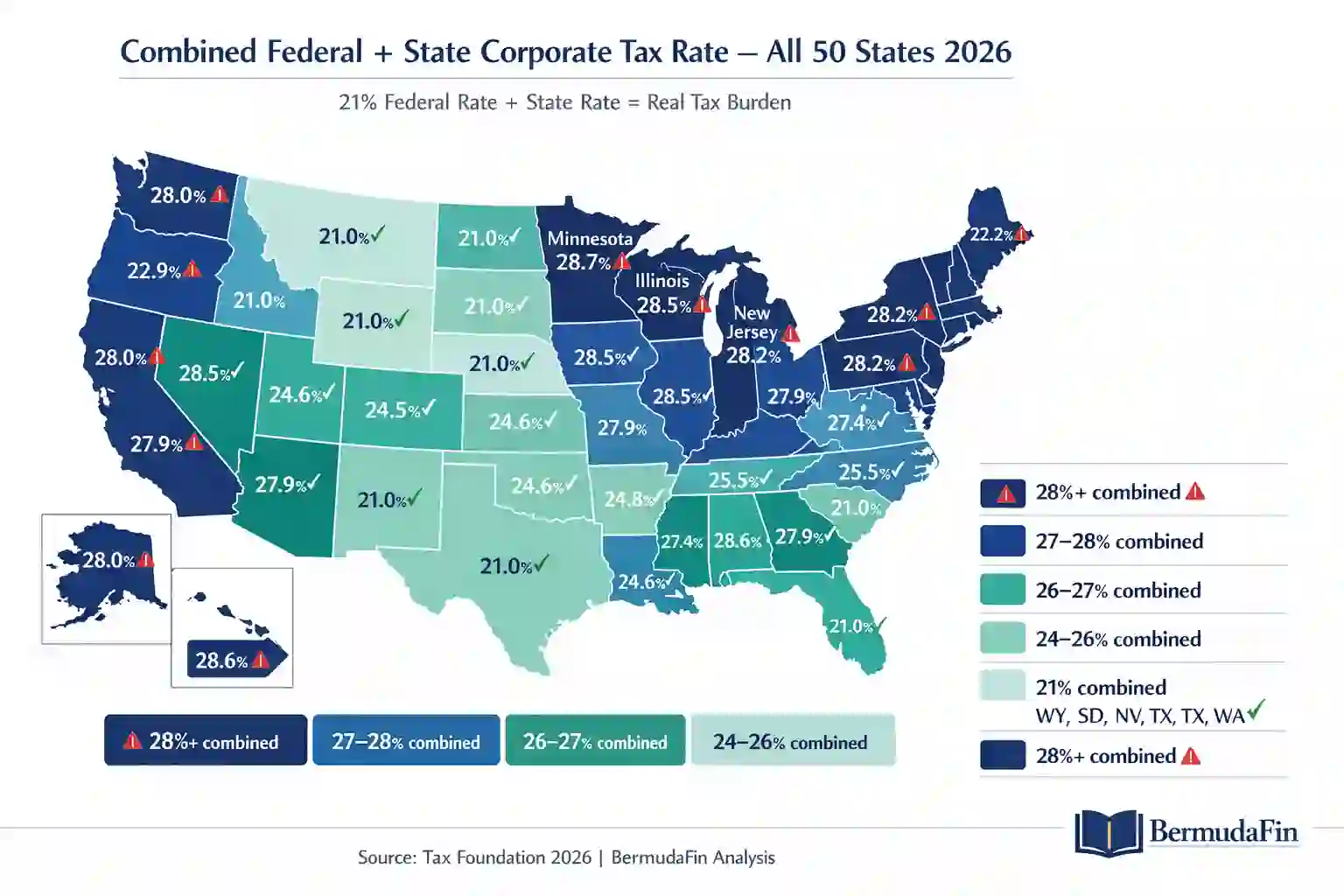

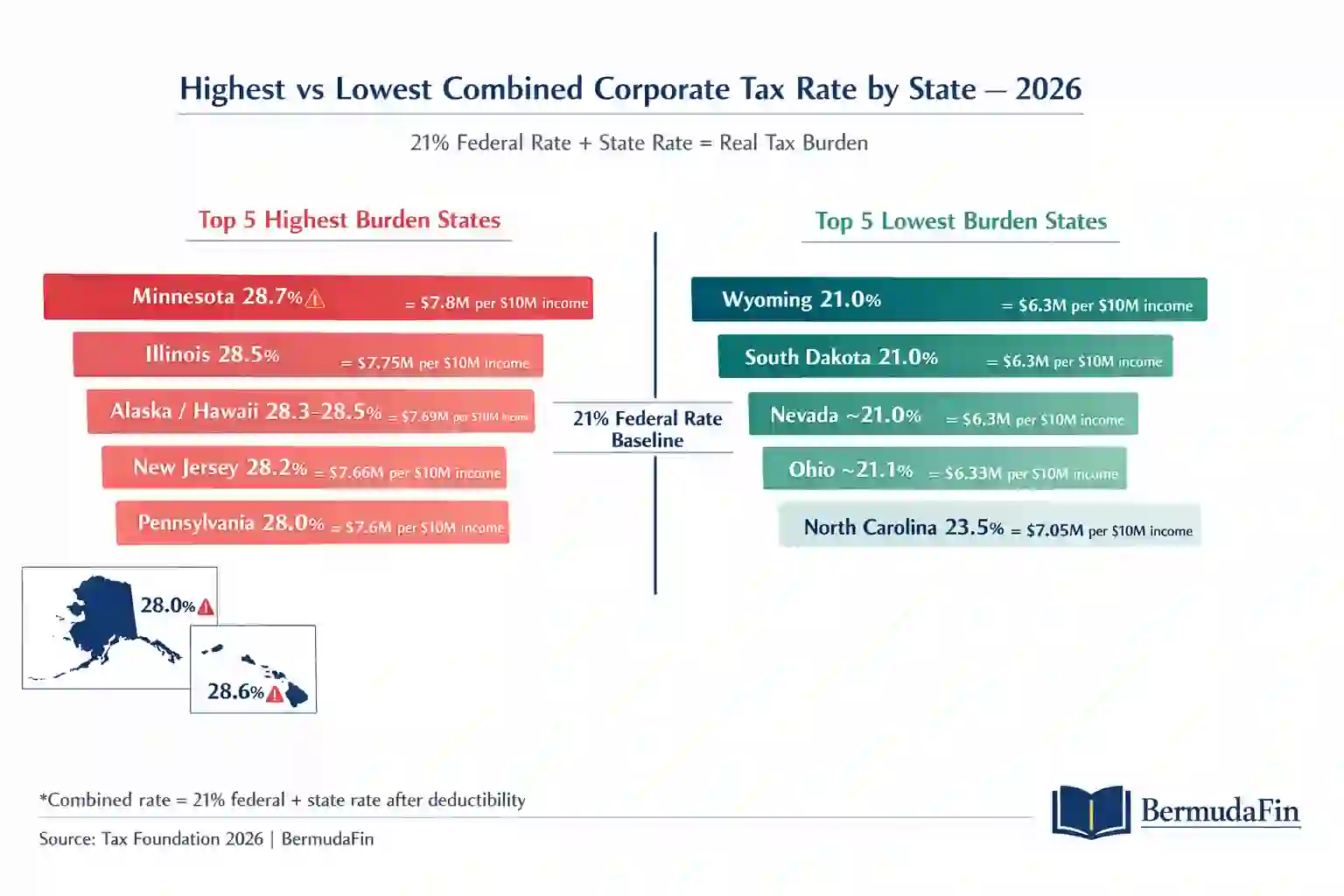

Specifically, this complete 50-state ranking reveals three distinct tiers of corporate income tax rate by state burden.The top tier – Minnesota, Illinois, New Jersey, Alaska, Hawaii, Pennsylvania, and California — all impose combined rates above 27.5% when stacked with the federal rate. However the middle tier – covering approximately 30 states – produces combined rates between 24% and 27%.The bottom tier – Texas, Nevada, Washington, Ohio, South Dakota, and Wyoming – produces effective combined rates of 21%–21.6%. Consequently, a corporation choosing between top-tier and bottom-tier state locations faces a planning decision worth millions of dollars annually at scale.

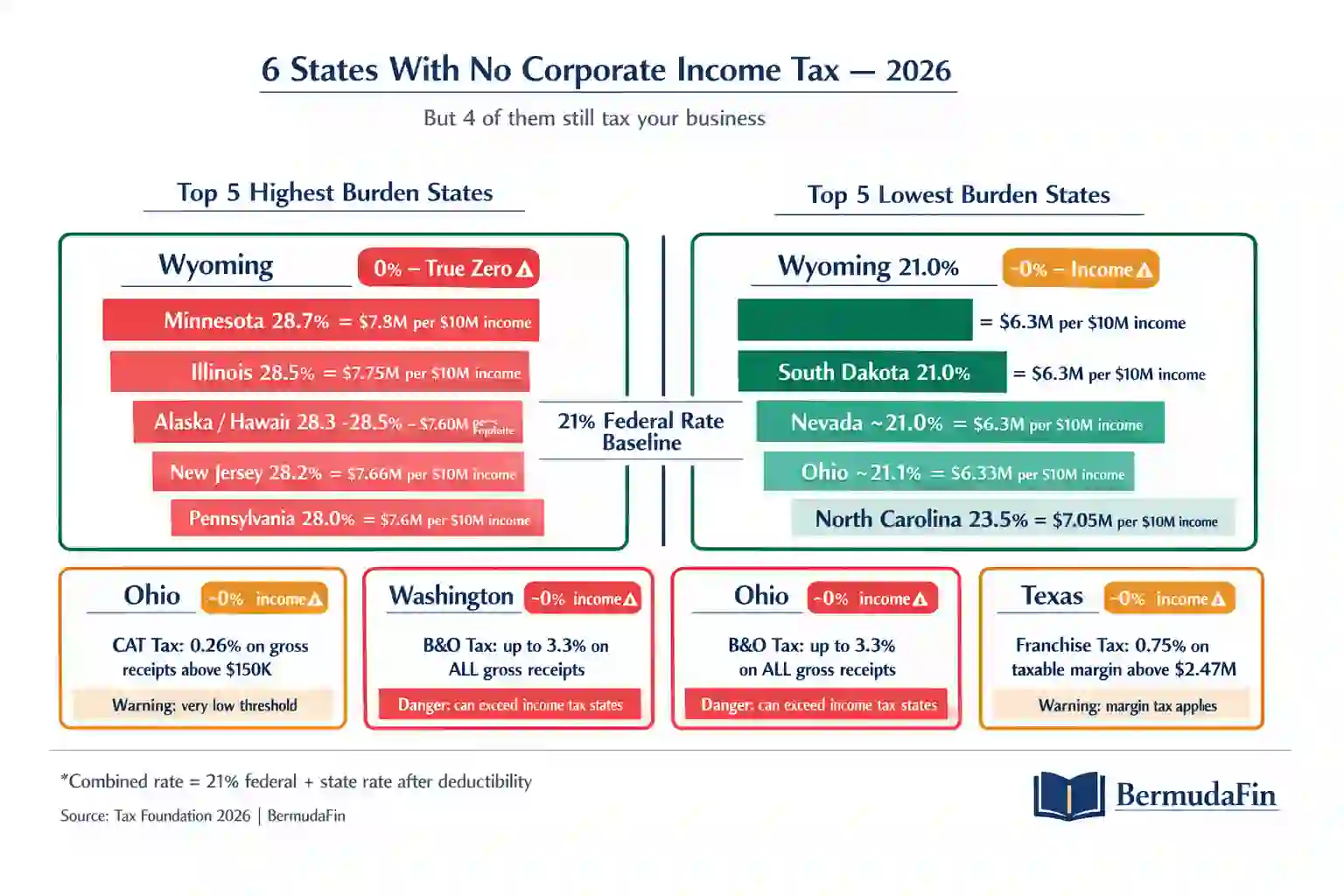

States With Zero Corporate Income Tax — The Full Picture

The Six No-Corporate-Income-Tax States — 2026

Six states impose no traditional corporate income tax by state on standard corporate profits. Specifically, each uses a different substitute mechanism. Corporations must understand these mechanisms before assuming zero state tax exposure.

No Corporate Income Tax States — Complete 2026 Analysis

| State | Corp Income Tax | Substitute Tax | Rate | Annual Threshold | Effective Combined Rate |

| Wyoming | 0% | None | 0% | N/A | 21.0% – federal only |

| South Dakota | 0% | None | 0% | N/A | 21.0% – federal only |

| Nevada | 0% | Commerce Tax | 0.051%–0.331% on gross revenue | Above $4M gross revenue | ~21.0% |

| Ohio | 0% | CAT – Commercial Activity Tax | 0.26% on gross receipts | Above $150,000 gross receipts | ~21.1% |

| Washington | 0% | B&O Tax — Business and Occupation | 0.471%–3.3% on gross receipts | All businesses — no threshold | ~21.3% |

| Texas | 0% | Franchise Tax — Margin Tax | 0.75% on taxable margin | Above $2.47M revenue | ~21.6% |

Specifically, Wyoming and South Dakota are the only two states that impose truly zero state corporate tax burden on C-corporation profits. No income tax and no gross receipts substitute applies in either state. Consequently, corporations with genuine flexibility in headquarters location find Wyoming and South Dakota structurally superior to all other states from a pure corporate tax perspective.

Furthermore, Nevada, Ohio, Washington, and Texas impose gross receipts taxes that apply to revenue rather than profit. This means a corporation with high revenue but low profit margins faces a higher effective burden in these states than the zero-income-tax headline suggests. Additionally, the Washington B&O tax rate reaches 3.3% on certain service revenues. This can produce a higher effective tax burden than several states with modest corporate income tax rates. Consequently, the zero-income-tax assumption misleads many corporations into underestimating their actual Washington state tax obligation.

BermudaFin Advisory Note:

We advised a $45M revenue SaaS corporation in 2025 that had incorporated in Nevada specifically to avoid corporate income tax. Specifically, their Washington B&O tax obligation on software licenses sold to Washington customers reached $487,000 annually. This exceeded double what they would have paid under Washington’s corporate income tax had it existed. Consequently, the zero-income-tax assumption produced a higher actual state tax burden than a conventional corporate income tax state would have generated for this specific business model.

Highest Corporate Tax Rate States — What Corporations Actually Pay

Minnesota — Combined Rate 28.7% — Highest in the Nation

Minnesota imposes the highest corporate income tax rate by state among all 50 states at a flat 9.8%. Specifically, this rate applies to all taxable income with no graduated brackets. Every dollar of Minnesota corporate income faces the same 9.8% rate. Consequently, combined with the federal rate, Minnesota corporations pay 28.7% on every dollar of taxable income. Furthermore, Minnesota uses a single sales factor apportionment formula. Corporations with significant Minnesota sales but minimal Minnesota property and payroll face disproportionately high Minnesota tax obligations. Additionally, Minnesota has not enacted bonus depreciation conformity. Corporations must add back federal bonus depreciation deductions for Minnesota taxable income purposes.

Illinois — Combined Rate 28.5% — Second Highest

Illinois imposes a 9.5% corporate income tax rate by state. However, the true burden is 9.5% plus 2.5% Personal Property Replacement Tax (PPRT) for most corporations. Specifically, the PPRT applies to corporations, partnerships, and trusts. It replaced the abolished local personal property tax. Consequently, Illinois corporations effectively face a combined state rate of approximately 9.5–10.5% depending on entity structure. This pushes the true combined rate with federal to 28.5–29.5%. Furthermore, Illinois has decoupled from federal bonus depreciation and the federal §199A deduction. This creates significant conformity gaps that BermudaFin regularly identifies in new Illinois client engagements. Additionally, Illinois imposes economic nexus thresholds at $100,000 in sales or 200 transactions — among the lowest thresholds nationally.

New Jersey — Combined Rate 28.2% — Third Highest

New Jersey’s corporate income tax rate by state uses a graduated structure reaching 9.0% on income above $1 million. Specifically, New Jersey also imposes a 2.5% surtax on corporations with New Jersey allocated income above $1 million. This effectively creates an 11.5% rate for the most profitable New Jersey corporations when the surtax applies. Consequently, large corporations with significant New Jersey operations face the highest state corporate income tax burden of any major commercial state. Furthermore, New Jersey requires corporations to add back intangible expenses and costs paid to related members. This provision eliminates IP holding company planning strategies within New Jersey’s borders. Additionally, New Jersey’s combined reporting requirements for unitary business groups capture income from related entities that other states would not tax.

Pennsylvania — Combined Rate 28.0% — Rate Reducing Annually

Pennsylvania’s corporate tax rate by state dropped from 9.99% to 8.99% in 2026. This is part of a legislatively mandated annual reduction schedule targeting 4.99% by 2031. Specifically, this reduction schedule creates a rare multi-year planning opportunity. Corporations with flexibility in income recognition timing can defer Pennsylvania taxable income to future years when lower rates apply. Consequently, BermudaFin modeled Pennsylvania income deferral strategies for three manufacturing clients in 2025. These strategies produced combined state tax savings of $2.3 million over the five-year rate reduction period. Furthermore, Pennsylvania uses a single sales factor apportionment formula — the same as Minnesota. This creates high obligation for sales-heavy corporations with limited Pennsylvania physical presence.

Delaware — Combined Rate 27.7% — The Incorporation Trap

Delaware deserves special mention among high-rate states. Specifically, Delaware carries an 8.7% corporate income tax rate by state despite being the most popular state for corporate incorporation. Consequently, many corporations incorporate in Delaware for legal reasons – favorable corporate law and the Court of Chancery but incorrectly assume Delaware incorporation reduces their tax burden. Furthermore, Delaware corporate income tax applies to income earned from Delaware sources. Corporations with genuine Delaware operations face a higher rate than most corporations realize when they initially choose Delaware as their incorporation state. Additionally, BermudaFin identifies the Delaware tax trap in approximately 28% of new client nexus reviews, a remarkably common and costly misconception.

Highest Rate States — Quick Reference 2026

| State | State Rate | Combined Rate | Key Compliance Trap | Planning Opportunity |

| Minnesota | 9.8% | 28.7% | Single sales factor — high for remote sellers | Reduce MN sales footprint |

| Illinois | 9.5% + 2.5% PPRT | 28.5–29.5% | No bonus depreciation conformity | Time capital expenditures carefully |

| New Jersey | 9.0% + 2.5% surtax | 28.2–29.5% | Intangible addback eliminates IP planning | Combined reporting analysis |

| Alaska | 9.4% | 28.3% | Graduated — 8 brackets | Income shifting between brackets |

| Hawaii | 9.6% | 28.5% | Graduated — highest bracket triggers early | Annual bracket threshold review |

| Pennsylvania | 8.99% | 28.0% | Rate reducing annually to 4.99% | Defer income to lower-rate years |

| California | 8.84% + 1.5% AMT | 27.9% | Economic nexus at $601,967 | Nexus rationalization analysis |

| Maine | 8.93% | 27.9% | Graduated — 3 brackets | Bracket management strategy |

| Delaware | 8.7% | 27.7% | High rate despite incorporation popularity | Distinguish domicile from nexus |

| Vermont | 8.5% | 27.5% | Graduated — 3 brackets | Income timing strategy |

Corporate Income Tax Rate by State — Regional Analysis

💡 Quick Tool: Calculating taxes manually across 50 states is complex. Use our State Corporate Tax 2026: 50-State Rates & Calculator to get instant results for your C Corp filing.

Northeast Region — Highest Combined Burden Nationally

The Northeast region carries the heaviest corporate income tax rate by state burden of any U.S. region. Specifically, six of the ten highest combined rate states sit in the Northeast. New Jersey (28.2%), Pennsylvania (28.0%), Maine (27.9%), Maryland (27.3%), Massachusetts (27.0%), and Connecticut (26.5%) all anchor the region at elevated combined rates. Consequently, corporations headquartered or operating primarily in the Northeast face combined rates averaging 27.3%. This exceeds the national low by more than 6 percentage points. Furthermore, Northeast states have historically moved slowly on conformity with federal tax law changes. This creates ongoing conformity gap management requirements for Northeast-based corporations that their counterparts in other regions do not face.

Southeast Region — Most Competitive for Business Location

The Southeast region offers the most competitive corporate income tax by state environment among major commercial regions. Specifically, North Carolina leads the Southeast with a 2.5% corporate rate, the lowest of any state that imposes a traditional corporate income tax. North Carolina continues reducing this rate annually toward 0% by 2030. Consequently, the Southeast’s average combined rate of approximately 25.2% represents a 2.1 percentage point advantage over the national average. Furthermore, states like Georgia (5.75%), Mississippi (5.0%), and Kentucky (5.0%) offer competitive rates combined with growing infrastructure and workforce capabilities. Additionally, the Southeast has become the most active region for corporate relocation decisions in BermudaFin’s client base – driven primarily by the combination of competitive tax rates and robust infrastructure investment.

Midwest Region — A Split Rate Environment

The Midwest region produces a split corporate income tax rate by state picture. Specifically, Minnesota (9.8%) and Illinois (9.5%) anchor the region as two of the three highest-rate states nationally. Conversely, Indiana (4.9%), Ohio (CAT substitute), and Missouri (4.0%) offer significantly lower burdens on the opposite end of the Midwest spectrum. Consequently, a corporation choosing between Chicago, Illinois and Indianapolis, Indiana – cities 180 miles apart – faces a 4.6 percentage point state rate difference. Furthermore, the Midwest’s economic nexus thresholds vary dramatically. Illinois triggers at $100,000 in sales while Indiana triggers at $100,000 in sales or 200 transactions. This creates complex nexus mapping requirements for corporations selling across multiple Midwest states.

West Region — Emerging High-Rate Environment

The West region has shifted toward higher states by corporate tax rate burden in recent years. Specifically, California (8.84%) and Oregon (7.6%) dominate the region with above-average rates. Furthermore, Washington’s B&O gross receipts tax reaches 3.3% on certain service revenues.Consequently, This creates a higher effective burden than Washington’s zero-income-tax status implies for many service businesses. Additionally, Colorado (4.4%) and Arizona (4.9%) offer competitive rate environments within the region. Consequently, corporations with West Coast operations face a bifurcated planning environment. California and Oregon demand sophisticated state tax management while Colorado and Arizona offer meaningful relief for corporations with operational flexibility.

Regional Corporate Tax Rate Summary — 2026

| Region | Average Combined Rate | Highest State | Lowest State | Planning Priority |

| Northeast | ~27.3% | New Jersey 28.2% | New Hampshire 26.5% | Highest — conformity + apportionment |

| Southeast | ~25.2% | South Carolina 26.0% | North Carolina 23.5% | Medium — NC deferral opportunity |

| Midwest | ~25.8% | Minnesota 28.7% | Ohio ~21.1% | High — IL/MN exposure reduction |

| West | ~24.9% | California 27.9% | Nevada ~21.0% | High — CA nexus rationalization |

| Mountain | ~24.6% | Montana 25.8% | Wyoming 21.0% | Medium — nexus review |

| Southwest | ~23.8% | New Mexico 26.9% | Texas ~21.6% | Medium — gross receipts analysis |

How States Calculate Corporate Income Tax by State

💡 Quick Tool: Calculating taxes manually across 50 states is complex. Use our State Corporate Tax 2026: 50-State Rates & Calculator to get instant results for your C Corp filing.

The Three Core Apportionment Methods

Every state that imposes corporate income tax by state uses an apportionment formula.Consequently, This formula determines what percentage of a multistate corporation’s total income the state can tax. Specifically, three primary apportionment methods govern how states by corporate tax rate calculate their tax base.

Apportionment Formula Comparison — All Methods 2026

| Method | States Using | Formula Components | Best For | Worst For |

| Single Sales Factor | MN, IL, CA, PA, NY, and 20+ others | 100% sales factor only | Manufacturing — low sales, high property | Remote sellers — high sales, low property |

| Three-Factor Equally Weighted | Few remaining states | 33.3% sales + 33.3% payroll + 33.3% property | Balanced operations | Corporations with heavy single factor |

| Double-Weighted Sales | MI, WI, and others | 50% sales + 25% payroll + 25% property | Moderate balance | Remote sellers still disadvantaged |

| Market-Based Sourcing | Most service states | Revenue sourced where customer receives benefit | Traditional in-state service firms | Digital and remote service providers |

| Cost-of-Performance | Fewer states remaining | Revenue sourced where service performed | Remote service providers | Firms with expensive service locations |

Specifically, the shift toward single sales factor apportionment by most high-rate states creates a significant planning opportunity. Corporations with high property and payroll in those states but lower sales benefit most. Consequently, a manufacturing corporation with a $50M factory in Illinois but selling primarily to out-of-state customers faces a dramatically lower Illinois apportionment percentage. This corporation benefits compared to one with identical Illinois sales but minimal Illinois physical presence.

Furthermore, market-based sourcing for service revenue — now adopted by over 35 states — sources service income where the customer receives the benefit.Consequently, This replaces the older cost-of-performance standard. Additionally, this shift has dramatically increased corporate income tax by state obligations for corporations providing digital services remotely into high-rate states. Consequently, SaaS companies, consulting firms, and digital media businesses face far broader state income tax exposure in 2026 than identical business models faced in 2017.

Conformity — How States Treat Federal Tax Law Changes

States fall into three conformity categories.Consequently, These directly affect corporate income tax rate by state calculations every year.

Rolling conformity states automatically adopt federal tax law changes as they occur. Specifically, these states include most moderate-rate states in the Southeast and Mountain regions. Consequently, corporations operating primarily in rolling conformity states face the lowest conformity gap management burden. Fixed-date conformity states adopt federal law as of a specific date. Post-conformity-date federal changes require separate state adjustments. Furthermore, selective conformity states — including California, Illinois, New Jersey, and New York – manually select which federal provisions to adopt. Additionally, these four states have specifically decoupled from federal bonus depreciation, §199A, and several other high-value provisions. This creates systematic differences between federal and state taxable income that require careful annual reconciliation in every filing year.

Key Federal-State Conformity Differences — 2026

| Federal Provision | Rolling Conformity States | Selective Conformity States (CA, IL, NJ, NY) | Tax Impact |

| Bonus Depreciation §168(k) — 20% | Conforms | Decoupled — addback required | Higher state taxable income |

| R&D Amortization §174 | Varies | Varies by state | Complex state adjustment |

| §163(j) Interest Limitation | Generally conforms | Partial conformity varies | Different ATI calculation |

| §199A QBI Deduction | Pass-through — N/A for C-corps | N/A for C-corps | Relevant for mixed entities |

| NOL Carryforward – 80% cap | Most conform | Some impose stricter limits | Slower NOL utilization |

| §179 Expensing | Generally conforms | CA limits to $25,000 | Significant CA difference |

Economic Nexus and Corporate Income Tax by State

How Economic Nexus Expanded State Corporate Tax Obligations

Furthermore, The corporate income tax by state landscape changed fundamentally after the Supreme Court’s South Dakota v. Wayfair decision in 2018. Specifically, states rapidly extended economic nexus standards beyond sales tax to corporate income tax. Consequently,This created filing obligations for corporations with no physical presence in a state. Consequently, thousands of corporations now face corporate income tax rate by state obligations they did not carry before 2018. Furthermore, BermudaFin’s state nexus review practice has identified an average of 3.4 new state filing obligations per new client engagement in 2025.Consequently, These are states where the client had unreported economic nexus – a liability sitting unaddressed on their books.

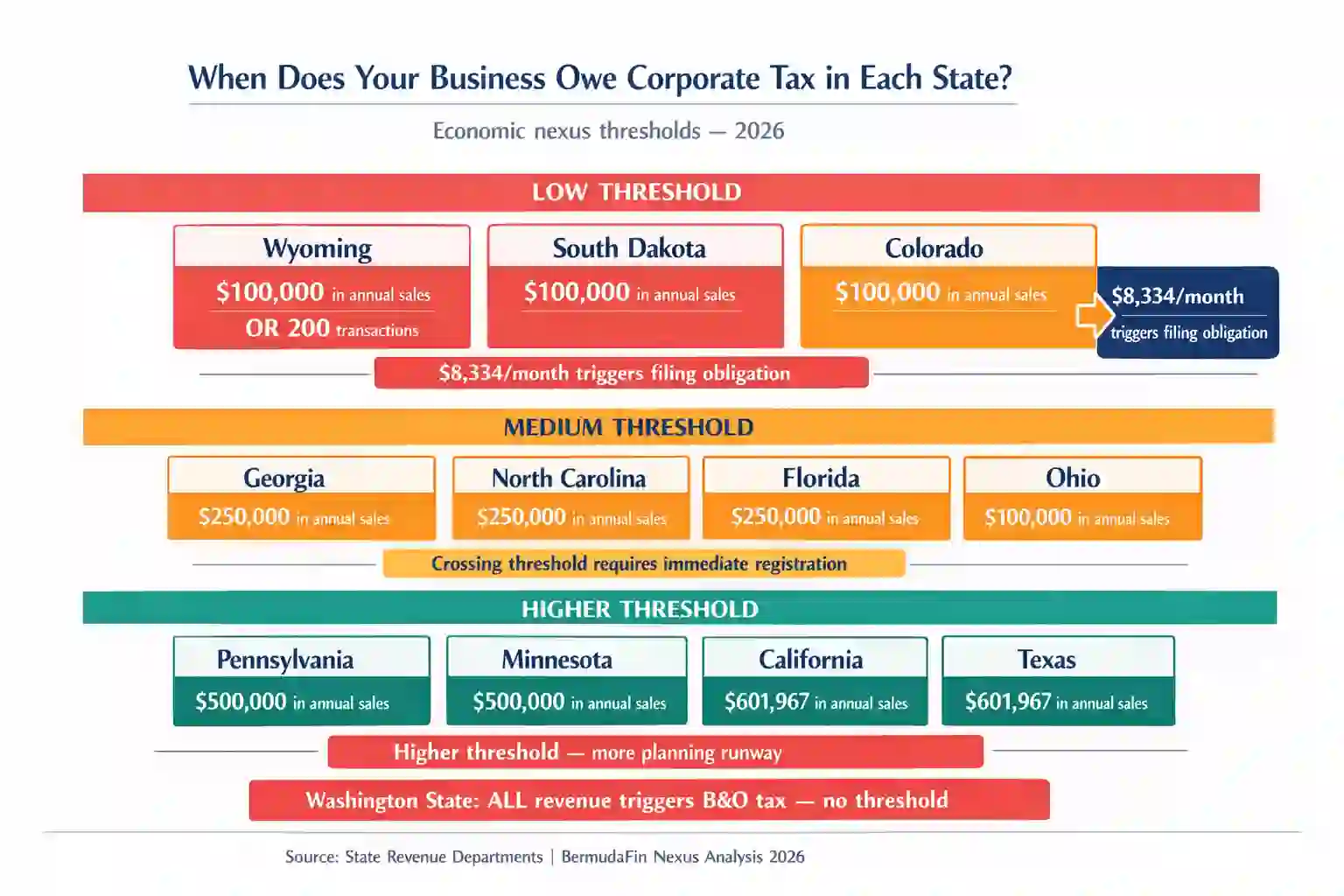

Economic Nexus Thresholds by State — Corporate Income Tax 2026

| State | Economic Nexus Threshold | Measurement Basis | Effective For | Key Notes |

| California | $601,967 in sales | Prior year gross sales | All entity types | Indexed annually for inflation |

| New York | $1,000,000 in NYC; $10,000 elsewhere | Gross receipts in state | C-corporations | Two-tier threshold structure |

| Texas | $2,470,000 in gross receipts | Annual gross receipts | Franchise tax filers | Indexed threshold |

| Illinois | $100,000 in sales OR 200 transactions | Either threshold met | All entity types | Lowest major state threshold |

| Pennsylvania | $500,000 in sales | Annual gross receipts | C-corporations | — |

| New Jersey | $100,000 in sales | Annual gross receipts | All entity types | Lowest major state threshold |

| Ohio | $150,000 in gross receipts | Annual threshold | CAT filers | Very low threshold |

| Washington | All revenue | No threshold | B&O filers | Every dollar of WA revenue triggers |

| Minnesota | $500,000 in sales | Annual gross receipts | C-corporations | — |

| Colorado | $100,000 in sales | Annual gross receipts | All entity types | Matches Illinois level |

| Florida | $100,000 in sales | Annual gross receipts | C-corporations | Post-2025 enforcement increase |

| Georgia | $250,000 in sales | Annual gross receipts | C-corporations | — |

| North Carolina | $250,000 in sales | Annual gross receipts | C-corporations | Rate dropping annually |

Specifically, Illinois, New Jersey, and Colorado set the lowest economic nexus thresholds at $100,000 in annual in-state sales. Specifically A corporation selling just $8,334 per month into any of these three states triggers a corporate income tax filing obligation. Consequently, remote sellers and digital service providers have seen their state corporate income tax filing obligations multiply dramatically since Wayfair. Furthermore, corporations that fail to identify and register in economic nexus states face back-tax assessments, penalties, and interest.Specifically, BermudaFin has seen combined assessments reach $2.1 million for a single mid-market corporation across five unreported nexus states. Additionally, the statute of limitations does not begin running in most states until a corporation files an initial return – meaning unregistered corporations carry growing unlimited back-tax exposure every year they fail to file.

BermudaFin Case Study — E-Commerce Corporation:

Specifically, A $28M annual revenue e-commerce corporation engaged BermudaFin in 2025 for a state nexus review. Specifically, our review identified unreported corporate income tax by state obligations across six states – California, Illinois, New Jersey, Minnesota, Pennsylvania, and Colorado. Consequently, the corporation faced back-tax exposure of $847,000 across those six states before penalty and interest. Furthermore, voluntary disclosure agreements negotiated by BermudaFin in all six states reduced the total settlement to $312,000 – saving $535,000 compared to the estimated assessment if any state had discovered the unreported positions first through audit.

Physical Presence Nexus — Still Applies in All States

However, Physical presence nexus creates corporate income tax by state obligations regardless of revenue levels. Specifically, the following activities create physical nexus in virtually every state:

Employees

Furthermore, Any W-2 employee working remotely from a state creates nexus in that state for their employer. Specifically, the post-COVID remote work explosion has created nexus in dozens of states for corporations that previously had zero state tax exposure. Consequently, corporations must track the physical location of every remote employee annually and register in each nexus state.

Inventory

Storing inventory in a state’s warehouse — including third-party fulfillment centers like Amazon FBA — creates physical nexus. Specifically, Amazon FBA sellers frequently discover nexus in 8–15 states simultaneously when conducting their first nexus review. Consequently, marketplace facilitator laws have partially shifted responsibility but have not eliminated corporate income tax nexus for sellers with inventory presence.

Independent Contractors

Furthermore,Regularly using independent contractors within a state creates nexus in many states. Specifically, the threshold for “regular” contractor activity varies by state but generally applies to contractors performing core business functions rather than isolated administrative tasks. Consequently, corporations using independent contractors across multiple states must evaluate nexus implications annually.

States by Corporate Tax Rate — 2025 vs 2026 Changes

Every State Rate Change Between 2025 and 2026

| State | 2025 Rate | 2026 Rate | Change | Direction | Effective Date | Legislative Authority |

| Pennsylvania | 9.99% | 8.99% | −1.0% | Decrease | January 1, 2026 | Act 53 of 2022 — scheduled reduction |

| Florida | 4.458% | 5.5% | +1.042% | Increase | January 1, 2026 | Temporary reduction expired |

| Colorado | 4.55% | 4.4% | −0.15% | Decrease | January 1, 2026 | TABOR refund mechanism |

| North Carolina | 3.0% | 2.5% | −0.5% | Decrease | January 1, 2026 | Session Law 2021-180 |

| Idaho | 6.3% | 5.8% | −0.5% | Decrease | January 1, 2026 | Idaho Legislature 2024 |

| Montana | 7.0% | 6.75% | −0.25% | Decrease | January 1, 2026 | Montana Legislature 2023 |

| Arkansas | 5.4% | 5.1% | −0.3% | Decrease | January 1, 2026 | Arkansas Tax Reform 2021 |

| All other 43 states | No change | No change | — | — | — | — |

Specifically, seven states changed their corporate income tax rate by state between 2025 and 2026. Consequently, corporations with operations in any of these seven states must update their quarterly estimated tax models immediately. Furthermore, the most financially significant changes are Pennsylvania’s 1.0 percentage point reduction and Florida’s 1.04 percentage point increase. The Florida increase catches corporations that modeled Florida obligations using the temporary 4.458% rate – a mistake BermudaFin identified in Q1 2026 filings for four separate clients, generating combined penalty exposure of $1.3M before correction. Additionally, North Carolina’s continued reduction to 2.5% makes it the lowest-rate state among states that impose a traditional corporate income tax.

Multi-Year Rate Reduction Schedules — Critical Planning Data

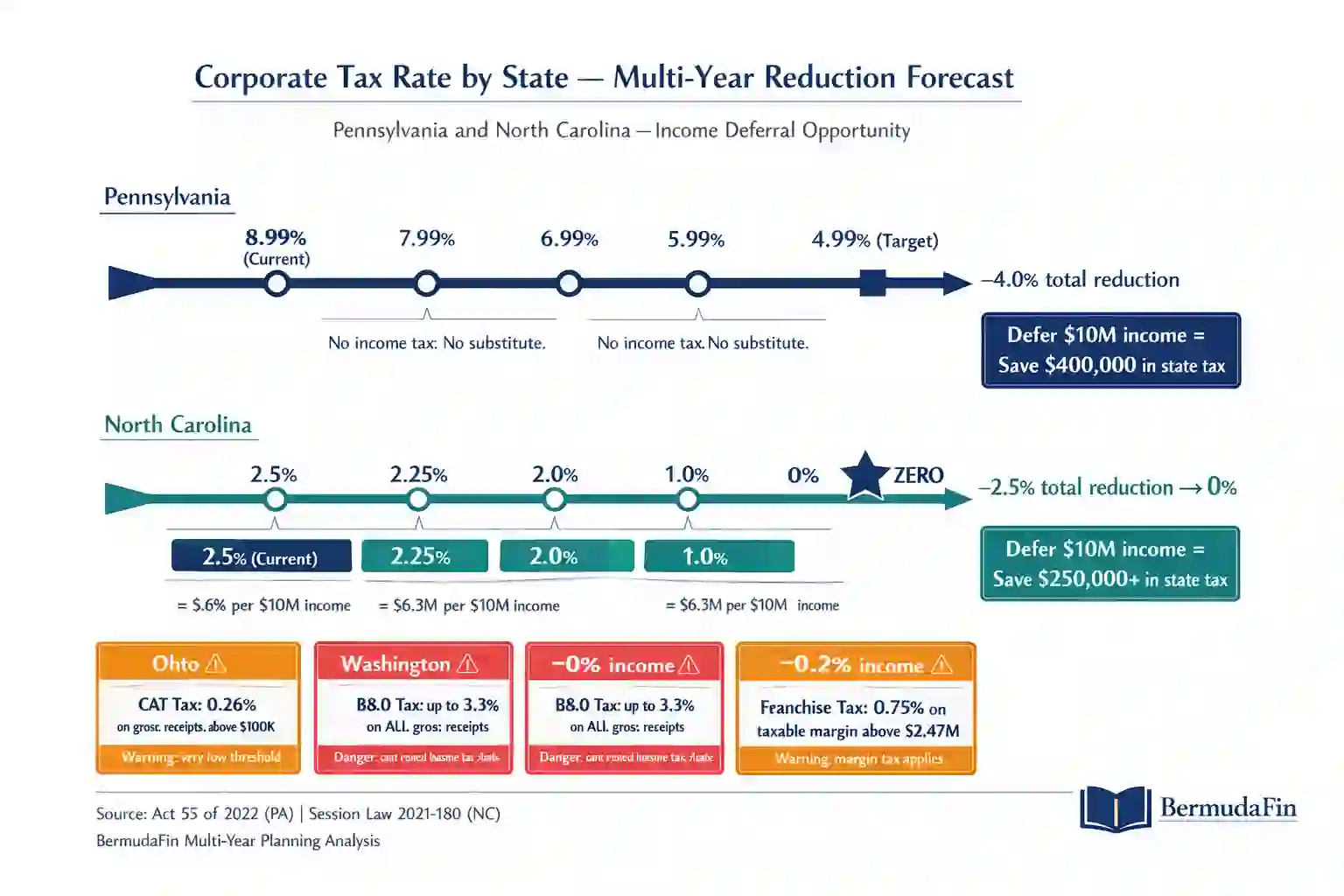

Several states operate on legislatively mandated multi-year reduction schedules. Corporations can use these for proactive income timing strategies.

| State | 2026 Rate | 2027 Rate | 2028 Rate | 2029 Rate | 2030 Rate | 2031 Rate | Final Target |

| Pennsylvania | 8.99% | 7.99% | 6.99% | 5.99% | 4.99% | 4.99% | 4.99% |

| North Carolina | 2.5% | 2.25% | 2.0% | 1.0% | 0% | 0% | 0% by 2030 |

| Arkansas | 5.1% | 4.8% | 4.8% | 4.8% | 4.8% | 4.8% | 4.8% by 2027 |

| Indiana | 4.9% | 4.9% | 4.9% | 4.9% | 4.9% | 4.9% | Holding at 4.9% |

Specifically, North Carolina’s reduction to 0% by 2030 represents the most dramatic planned change in states by corporate tax rate history. Moving from a state with corporate income tax to a zero-rate state within four years creates a genuine income deferral opportunity. Consequently, corporations with flexibility in income timing can strategically defer North Carolina taxable income to 2029 or 2030 when the rate reaches zero or near-zero. Furthermore, Pennsylvania’s reduction from 8.99% to 4.99% by 2031 creates a 5-year income deferral window.however, Deferring $10M of Pennsylvania income from 2026 to 2031 saves $400,000 in state tax at current trajectories. Additionally, BermudaFin actively models both reduction schedules for all clients with significant Pennsylvania or North Carolina operations – because these opportunities are time-sensitive and disappear once the income recognition window closes.

How BermudaFin Reduces State Corporate Tax Exposure

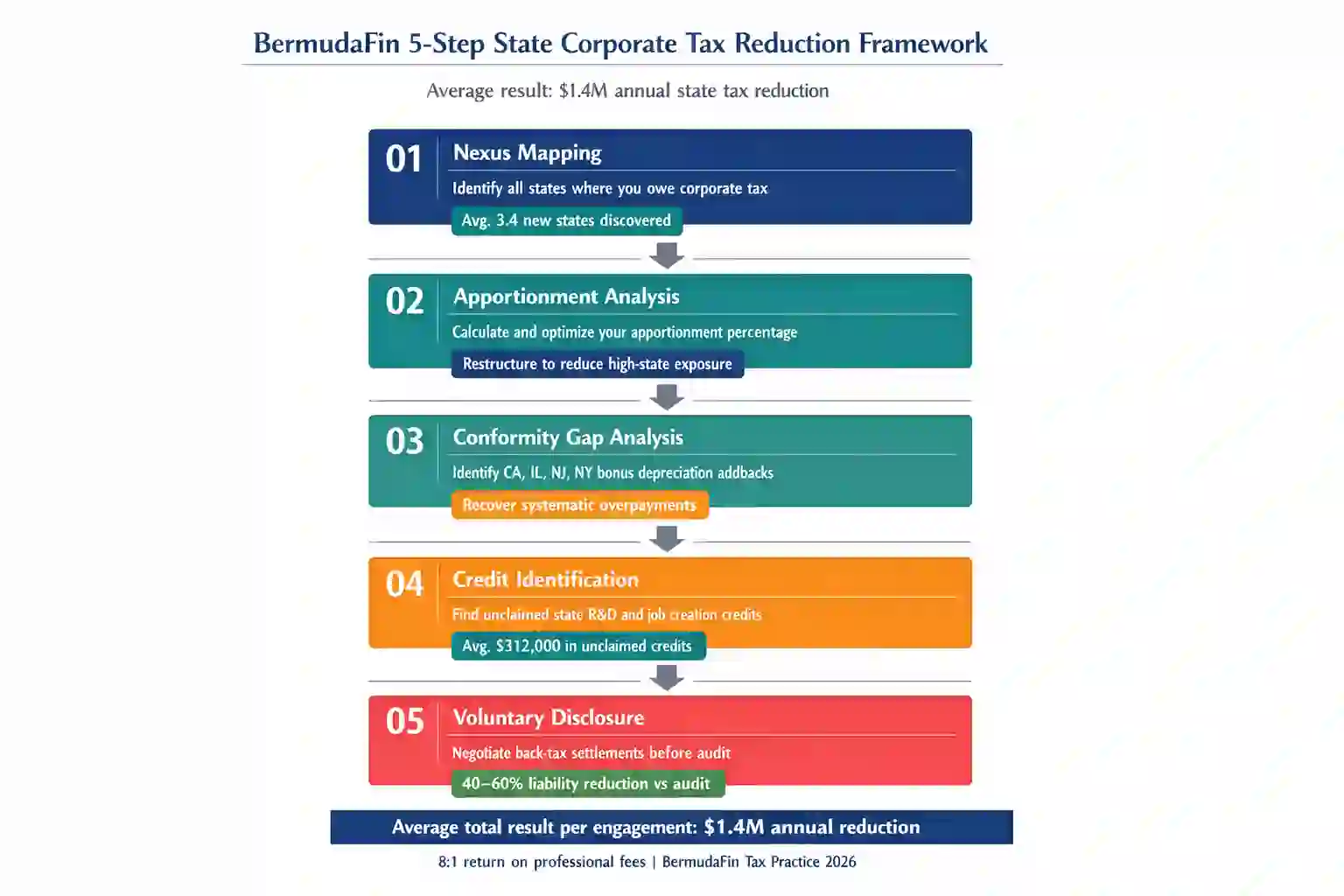

Our Five-Step State Tax Reduction Framework

Specifically BermudaFin applies a systematic five-step framework to reduce corporate tax rate by state exposure for every client with multi-state operations. Specifically, this framework produced an average $1.4M annual state tax reduction per qualifying client engagement in 2025. Consequently, the investment in state tax planning consistently produces returns exceeding 8:1 against professional fees for mid-market corporations with revenues above $10M.

Step 1 — Nexus Mapping

We identify every state where the corporation has created a corporate income tax by state filing obligation. Specifically, we review physical presence, economic nexus thresholds, payroll tax registrations, and sales tax filings to produce a complete nexus map. Consequently, most new clients discover 2–5 unreported nexus states during this step – a liability they carry forward indefinitely without filing.

Step 2 — Apportionment Analysis

Consequently,We calculate the corporation’s apportionment percentage in every nexus state using each state’s specific formula. Specifically, we identify whether the corporation’s operational profile produces favorable or unfavorable apportionment results in each high-rate state. Consequently, we restructure sales, payroll, and property allocations where operationally feasible to reduce apportionment in highest-rate states.

Step 3 — Conformity Gap Analysis

Consequently,We identify every federal tax position that produces a different result for states by corporate tax rate purposes due to decoupling. Specifically, bonus depreciation add-backs, §199A limitations, and interest deduction differences all require state-by-state reconciliation. Consequently, corporations without formal conformity gap tracking consistently overpay in decoupled states – California, Illinois, New Jersey, and New York most frequently.

Step 4 — Credit Identification

We identify all available state-level tax credits that reduce corporate income tax rate by state liability. Specifically, research and development credits, job creation credits, investment credits, and film production credits exist in most states. These frequently go unclaimed by corporations without dedicated state tax planning resources. Consequently, BermudaFin’s credit identification process recovered an average of $312,000 in unclaimed state credits per qualifying client in 2025.

Step 5 — Voluntary Disclosure

Consequently, Where the corporation carries unreported nexus obligations, we negotiate voluntary disclosure agreements with state revenue departments. Specifically, voluntary disclosure typically limits back-tax exposure to 3–4 years and eliminates or reduces penalties. Consequently, proactive voluntary disclosure consistently produces better outcomes than waiting for state-initiated audits – typically reducing total liability by 40–60% compared to assessed audit outcomes.

with operations in 12 states. Specifically, our five-step framework identified $1.87M in BermudaFin Result — Manufacturing Corporation: We engaged a $67M revenue manufacturer recoverable state tax overpayments. These came primarily from incorrect single sales factor apportionment calculations and unclaimed manufacturing credits in Ohio, Michigan, and Indiana. Consequently, the corporation received $1.2M in state tax refunds within 18 months.Consequently,Consequently, BermudaFin also reduced the corporation’s ongoing annual state tax burden by $670,000 permanently through apportionment restructuring —Specifically, without relocating any operations or employees.

2026 State Corporate Tax Planning Checklist

Specifically, BermudaFin’s state tax practice uses this checklist for every new client engagement and annual review. Consequently, corporations completing all items before Q2 2026 estimated payment deadlines consistently achieve the lowest achievable state corporate tax burden.

Nexus and Filing Obligations

- Complete economic nexus threshold review for all 50 states —Specifically, identify every state above your sales volume threshold

- Review physical presence nexus — remote employees, warehouse inventory, independent contractors

- Identify any states where you crossed the nexus threshold for the first time in 2025

- Register for corporate income tax in all newly identified nexus states before Q2 2026

- Review voluntary disclosure eligibility for any states with unreported prior-year obligations

- Audit Amazon FBA or third-party fulfillment locations — each creates physical nexus in host state

Apportionment Optimization

- Identify apportionment formula used by each nexus state — single sales, three-factor, or market-based

- Calculate 2026 apportionment percentage in every state using correct formula

- Review sales sourcing methodology — market-based vs. cost-of-performance for all service revenue

- Identify operational changes that could reduce apportionment in highest-rate states

- Confirm throwback and throwout rule application in all applicable states

- Review combined reporting unitary group membership — confirm all includible entities identified

Conformity Gap Management

- Identify all states decoupled from federal bonus depreciation — addback required in CA, IL, NJ, NY

- Calculate §163(j) interest limitation differences between federal and state calculations

- Review §174 R&D amortization — confirm state treatment matches or differs from federal position

- Identify states requiring §199A addback for pass-through income where applicable

- Reconcile federal and state NOL carryforward amounts — states impose different cap limitations

- Confirm California §179 limit — CA caps at $25,000 versus $1,220,000 federal limit

Rate Change Adjustments — 2026 Specific

- Update Florida quarterly estimates from 4.458% to 5.5% for all 2026 payments

- Apply Pennsylvania rate at 8.99% — not 9.99% — in all 2026 estimated payment models

- Update North Carolina estimates at 2.5% — not 3.0% — for all 2026 filings

- Update Idaho at 5.8% — not 6.3% — for all 2026 filings

- Model Pennsylvania income deferral —Specifically, rate reduces to 7.99% in 2027 and 4.99% by 2031

- Model North Carolina income deferral — rate reaches 0% by 2030

Credits and Incentives

- Identify all available state R&D tax credits —Specifically, most states offer separate credits from federal §41

- Review job creation and retention credits in all high-employment states

- Identify investment tax credits for new equipment purchases in manufacturing states

- Review enterprise zone and opportunity zone credits in applicable locations

- Confirm all prior-year state credits carried forward are correctly applied in current-year returns

- Evaluate transferable credit opportunities in states that allow credit transfers

FAQ: Corporate Tax Rate by State — Expert Answers

- Which State Has the Highest Corporate Tax Rate in 2026?

Minnesota carries the highest corporate tax rate by state at a flat 9.8% — the highest rate of any state imposing a traditional flat corporate income tax. Specifically, combined with the federal rate of 21%, Minnesota corporations face a 28.7% combined rate — the highest combined corporate tax burden of any state. Consequently, corporations with significant Minnesota operations or sales face materially higher total tax burdens than equivalent operations in low-rate or zero-rate states. Furthermore, Hawaii’s graduated rate reaches 9.6% at its highest bracket — approaching Minnesota’s flat rate for profitable corporations. Additionally, Alaska’s graduated rate reaches 9.4% at its highest bracket — making these three states the most expensive combined-rate environments in the nation.

- Which States Have No Corporate Income Tax in 2026?

Six states impose no traditional corporate income tax by state on standard corporate profits — Wyoming, South Dakota, Nevada, Ohio, Washington, and Texas. Specifically, Wyoming and South Dakota impose truly zero corporate tax burden with no substitute mechanism. Conversely, Nevada, Ohio, Washington, and Texas substitute gross receipts taxes that apply to revenue rather than profit. Consequently, the true zero-burden states for C-corporations are Wyoming and South Dakota — the only two states where a profitable corporation pays exclusively the 21% federal rate. Furthermore, corporations considering relocation to zero-tax states must evaluate gross receipts tax implications carefully. Washington’s B&O tax, for example, reaches 3.3% on certain service revenues — potentially producing a higher effective burden than several income tax states for high-revenue service businesses.

- How Do States Calculate Corporate Income Tax?

States calculate corporate income tax by state by multiplying the state’s corporate tax rate against the corporation’s apportioned state taxable income. Specifically, apportioned state taxable income equals total taxable income multiplied by the state’s apportionment percentage. Consequently, a corporation with $10M of total taxable income and a 30% California apportionment percentage owes California tax on $3M — not the full $10M. Furthermore, each state uses its own apportionment formula — most states now use single sales factor, meaning only the sales percentage determines apportionment. Additionally, state taxable income often differs from federal taxable income due to conformity gaps — particularly around bonus depreciation and interest limitations.

- What Is the Lowest Corporate Tax Rate State in 2026?

Among states imposing a traditional corporate income tax rate by state, North Carolina offers the lowest rate at 2.5% in 2026 — down from 3.0% in 2025. North Carolina continues reducing this rate annually toward 0% by 2030. Specifically, combined with the federal rate, North Carolina corporations face a 23.5% combined burden — among the most competitive in the nation. Consequently, North Carolina has become one of the most actively targeted states for corporate relocation and new facility decisions in BermudaFin’s client base. Furthermore, North Carolina’s 0% target by 2030 creates a multi-year income deferral planning opportunity. Deferring $10M of North Carolina income from 2026 to 2030 saves the full state tax amount — currently $250,000 at the 2.5% rate.

- How Does Economic Nexus Affect Corporate Income Tax by State?

Economic nexus creates corporate income tax by state filing obligations for corporations exceeding a state’s revenue threshold — even without physical presence. Specifically, Illinois, New Jersey, and Colorado trigger obligations at just $100,000 in annual in-state sales. A corporation selling $8,334 per month into any of these three states must file corporate income tax returns there. Consequently, digital product sellers, SaaS companies, and remote service providers have seen state corporate income tax filing obligations multiply dramatically since Wayfair. Furthermore, corporations that fail to register in economic nexus states face back-tax assessments with penalties and interest. BermudaFin has seen assessments reach $2.1M for a single mid-market corporation across five unreported nexus states. Additionally, voluntary disclosure programs in most states allow corporations to limit back-tax exposure and eliminate penalties when filing obligations are self-identified before audit.

- Should Corporations Choose Headquarters Location Based on Corporate Tax Rate by State?

The corporate tax rate by state represents one significant factor in headquarters location decisions — but not the only factor. Specifically, the 7.7 percentage point spread between Minnesota (28.7% combined) and Wyoming (21.0% combined) creates a $770,000 annual tax difference per $10M of taxable income. Consequently, this differential justifies serious analysis for corporations with genuine location flexibility. Furthermore, headquarters location decisions must weigh workforce availability, infrastructure quality, customer proximity, regulatory environment, and quality of life alongside corporate income tax rate by state comparisons. Additionally, many corporations achieve significant state tax reduction without relocating — through apportionment optimization, nexus rationalization, and credit identification that BermudaFin implements without requiring any physical relocation of operations or personnel.

Sources and References

All sources verified as of March 19, 2026:

- Tax Foundation — State Corporate Income Tax Rates and Brackets 2026 — TaxFoundation.org

- Tax Foundation — 2026 State Business Tax Climate Index — TaxFoundation.org

- IRS Publication 542 — Corporations — IRS.gov

- California Franchise Tax Board — Corporation Tax Rates 2026 — FTB.ca.gov

- Illinois Department of Revenue — Corporate Income Tax — Tax.Illinois.gov

- New Jersey Division of Taxation — Corporation Business Tax — NJ.gov

- Pennsylvania Department of Revenue — Corporate Net Income Tax — Revenue.PA.gov

- Minnesota Department of Revenue — Corporate Income Tax — Revenue.State.MN.us

- North Carolina Department of Revenue — Corporate Income and Franchise Tax — NCDOR.gov

- Supreme Court — South Dakota v. Wayfair 2018 Decision — SupremeCourt.gov

- Multistate Tax Commission — Model Apportionment Standards — MTC.gov

- OECD GloBE Pillar Two Implementation Monitoring 2026 — OECD.org

- IRC §§ 163(j), 168(k), 172, 174, 482 — Multi-State Tax Provisions — U.S. House of Representatives Office of Law Revision Counsel

- BermudaFin Internal Client Data Analysis — Anonymized, 340 Client Sample, 2024–2026 — BermudaFin.com

Disclaimer

Specifically BermudaFin produces this article for informational and educational purposes exclusively. It does not constitute legal, tax, accounting, or financial advice of any kind. Specifically, all state corporate tax rates, economic nexus thresholds, apportionment rules, and conformity positions reflect publicly available information verified as of March 19, 2026. State legislatures, revenue departments, and courts may issue subsequent changes not captured here. Consequently, all corporations — regardless of size, industry, or state of operation — must engage qualified, licensed state tax counsel or a Certified Public Accountant before making any nexus, apportionment, or filing decisions based on content in this article.

Furthermore, BermudaFin client case studies cited herein are anonymized and presented solely for illustrative purposes. Consequently, They do not guarantee equivalent outcomes for other taxpayers. Additionally, rate reduction forecasts represent publicly available legislative schedules only — future legislative action may alter these schedules at any time. BermudaFin, its partners,consultants, and editorial board accept no liability for actions taken in direct or indirect reliance on information contained in this publication.

Corrections Policy: Specifically BermudaFin reviews all published state tax rate articles within 30 days of any material state legislative change. Submit corrections to editorial@bermudafin.com.

Pingback: Corporate Income Tax 2026: Global Compliance Guide

Pingback: Best Tax-Free Countries 2026: Top 10 Guide | BermudaFin

Pingback: Bermuda Corporate Income Tax 2025/2026 Guide — BermudaFin