If you’re a US citizen living in Bermuda, the Roth IRA question comes up fast. Bermuda has no income tax. You probably earn well. And the IRS still considers you fully taxable on worldwide income, no matter where you sleep.

So can you still contribute to a Roth IRA from Hamilton? The answer is yes, with conditions. And those conditions catch a lot of expats off guard.

What a Roth IRA actually is?

A Roth IRA is a US retirement account funded with after-tax dollars. You contribute money that’s already been taxed, it grows tax-free, and you pull it out in retirement completely tax-free.

The IRS created it in 1997 under Senator William Roth. It’s been the same basic structure ever since. Contribute after tax, grow tax-free, withdraw tax-free after 59½.

Simple idea. The complications come from the income limits, the foreign earned income exclusion, and the self-employment wrinkle that trips up every Bermuda-based freelancer or business owner.

The IRS created it in 1997 under Senator William Roth — read the full IRS Roth IRA rules directly on their official page.

Roth IRA income limits for 2026

For 2026, the Roth IRA contribution limit is $7,000 if you’re under 50. If you’re 50 or older, it’s $8,000 (the $1,000 catch-up contribution).

But here’s the income filter the IRS applies before you can contribute a single dollar.

Single filers

- Full contribution: modified adjusted gross income (MAGI) below $150,000

- Partial contribution: MAGI between $150,000 and $165,000

- No contribution: MAGI above $165,000

Married filing jointly

- Full contribution: MAGI below $236,000

- Partial contribution: MAGI between $236,000 and $246,000

- No contribution: MAGI above $246,000

Your MAGI for Roth IRA purposes includes wages, self-employment income, rental income, and foreign income even after the Foreign Earned Income Exclusion (FEIE). More on that in a moment.

Roth IRA income phase-out ranges: 2026

| Filing Status | Full Contribution | Partial Contribution | No Contribution |

|---|---|---|---|

| Single / Head of Household | MAGI below $150,000 | $150,000 to $165,000 | Above $165,000 |

| Married filing jointly | MAGI below $236,000 | $236,000 to $246,000 | Above $246,000 |

| Married filing separately | $0 (lived with spouse) | $0 to $10,000 | Above $10,000 |

The foreign earned income problem Bermuda expats run into

The Foreign Earned Income Exclusion lets US expats exclude up to $126,500 of foreign earned income from US federal tax for 2024. That sounds like a clean way to reduce your tax bill.

But it creates a Roth IRA trap.

The IRS requires you to have earned income at least equal to your Roth contribution to contribute at all. Earned income, for IRA purposes, means wages or self-employment income after subtracting the FEIE.

So if you earn $80,000 in Bermuda and exclude all of it under FEIE, your earned income for IRA purposes is $0. You can’t contribute to a Roth IRA at all that year, because your eligible earned income is zero.

The fix some expats use: don’t claim the full FEIE. Leave enough earned income on the table to cover your $7,000 contribution. You’ll owe a bit of US tax on that $7,000, but you keep your Roth IRA eligibility alive.

It’s a deliberate trade-off. Whether it makes sense depends on your tax rate and how much you value the Roth’s long-term compounding.

Roth IRA rules for Bermuda residents: what’s different

Living in Bermuda doesn’t change the IRS rules that apply to you as a US citizen. You’re still subject to every contribution limit, income threshold, and withdrawal rule that applies to someone in Atlanta or Denver.

What’s different is your starting position.

Bermuda has zero personal income tax. So your Bermuda employer won’t withhold US taxes automatically. You’re responsible for quarterly estimated payments to the IRS yourself. Miss those and you’re looking at underpayment penalties by April.

Also, any Bermuda-source income you earn gets reported on your US return. The Foreign Tax Credit won’t help you offset Bermuda income (there’s no Bermuda income tax to credit). The FEIE is your main tool, but as explained above, it cuts both ways for Roth IRA eligibility.

Can a US expat open a Roth IRA from Bermuda?

Yes. US citizens can open and contribute to a Roth IRA regardless of where they live, as long as they have qualifying earned income and stay within the MAGI limits.

The practical issue is that most US brokerage firms won’t open new accounts for people with a foreign address. Fidelity, Schwab, and Vanguard all have this policy to some degree. Some will let you keep an existing account but won’t allow new account openings once you update your address to a foreign country.

The options people actually use:

- Keep a US mailing address (a family member’s address, a US-based mail forwarding service)

- Open the account before you leave the US

- Use a broker that explicitly accepts expat clients (Interactive Brokers is the most commonly cited option)

Whatever you do, don’t list a foreign address on a new account application and then claim FEIE on the same return without understanding the earned income issue first. The IRS cross-references these.

Roth IRA vs 401k for expats: which one actually makes sense

Both accounts grow tax-free in different ways. The comparison matters a lot depending on whether your Bermuda employer offers a US-style 401k.

When a 401k wins

If your employer offers a 401k with a match, contribute at least enough to get the full match. That’s 100% instant return on your money before any market gains. The 2026 employee contribution limit is $23,500 (or $31,000 if you’re 50+). Traditional 401k contributions reduce your current taxable income, which helps if you’re in a higher bracket.

When a Roth IRA wins

The Roth IRA wins on flexibility. There’s no required minimum distribution (RMD) at 73. You can let the money sit and grow forever if you want. And the $7,000 annual limit, while small compared to a 401k, builds up meaningfully over 20 years.

For Bermuda expats specifically: if you expect your US tax rate in retirement to be higher than it is now (because you might move back to a high-tax state), the Roth’s tax-free withdrawal is worth a lot. You lock in today’s tax treatment.

The honest answer

Most expats with access to both should use both. Contribute enough to the 401k to capture the match, then put the rest into a Roth IRA up to the $7,000 limit.

Roth IRA vs traditional IRA vs 401k: side-by-side comparison for US expats

| Feature | Roth IRA | Traditional IRA | 401k (Traditional) | Solo 401k |

|---|---|---|---|---|

| 2026 contribution limit | $7,000 / $8,000 (50+) | $7,000 / $8,000 (50+) | $23,500 / $31,000 (50+) | $70,000 total |

| Tax on contributions | After-tax (no deduction) | Pre-tax (deductible) | Pre-tax (deductible) | Pre-tax (deductible) |

| Tax on growth | Tax-free | Tax-deferred | Tax-deferred | Tax-deferred |

| Tax on withdrawal | Tax-free (qualified) | Taxed as income | Taxed as income | Taxed as income |

| Income limit to contribute | Yes ($165k single / $246k married) | No limit (deduction phases out) | No income limit | No income limit |

| Early withdrawal penalty | 10% on earnings under 59½ | 10% on all funds under 59½ | 10% under 59½ | 10% under 59½ |

| Required minimum distributions | None (ever) | Starts at age 73 | Starts at age 73 | Starts at age 73 |

| Employer match available | No | No | Yes | No (you are the employer) |

| Backdoor strategy available | Yes | N/A | No | No |

| FEIE impact on eligibility | Yes (reduces earned income) | Yes (reduces earned income) | No impact | No impact |

| Best for expats who | Expect higher tax rate in retirement | Expect lower tax rate in retirement | Have employer match available | Are self-employed in Bermuda |

| Works from Bermuda | Yes (with brokerage that accepts expats) | Yes (same brokerage issue) | Only if employer offers it | Yes (self-employed) |

| 5-year rule applies | Yes | No | No | No |

| Roth conversion possible | Already Roth | Yes (convert to Roth) | Yes (in-plan conversion) | Yes (convert to Roth) |

| Penalty-free contribution withdrawal | Yes (anytime) | No | No | No |

Roth IRA income limits for self-employed expats in Bermuda

If you run your own business from Bermuda, the calculation gets messier.

Self-employment income counts as earned income for Roth IRA purposes. But you also pay self-employment tax (15.3% on the first $168,600 of net self-employment income for 2024), which you can deduct. That deduction slightly reduces your MAGI.

The sequence:

- Calculate net self-employment income (revenue minus business expenses)

- Deduct half of self-employment tax (this reduces your MAGI)

- Apply the FEIE if you qualify

- Whatever earned income remains after FEIE, that’s what you can contribute up to (capped at $7,000)

If you exclude all your self-employment income through FEIE, you’re back to the same zero-earned-income problem. Same trade-off applies: leave some income unexcluded to fund your Roth.

One option worth knowing: a SEP-IRA or Solo 401k might make more sense than a Roth IRA if you’re self-employed and your income is well above the Roth limits anyway. The backdoor Roth becomes the route at that point.

Roth IRA for Bermuda expats vs domestic US residents: key differences

| Factor | US Domestic Resident | Bermuda-Based US Expat |

|---|---|---|

| Qualifying earned income | Wages, self-employment income | Same, but FEIE can reduce eligible amount to zero |

| MAGI calculation | Straightforward | Must add back FEIE exclusion amount |

| State tax on withdrawal | Depends on state | No Bermuda tax, but US state tax may apply if you return |

| Brokerage account access | All major brokers | Limited, most require US address |

| Foreign tax credit available | N/A | No Bermuda income tax to credit |

| Quarterly estimated payments | Optional (withholding covers most) | Required (no employer withholding to IRS) |

| Form filing requirements | Form 5329 if early withdrawal | Form 5329 + Form 8606 + possibly FBAR |

| Risk of missed contribution | Low (easy US bank transfer) | Moderate (international transfer timing, currency conversion) |

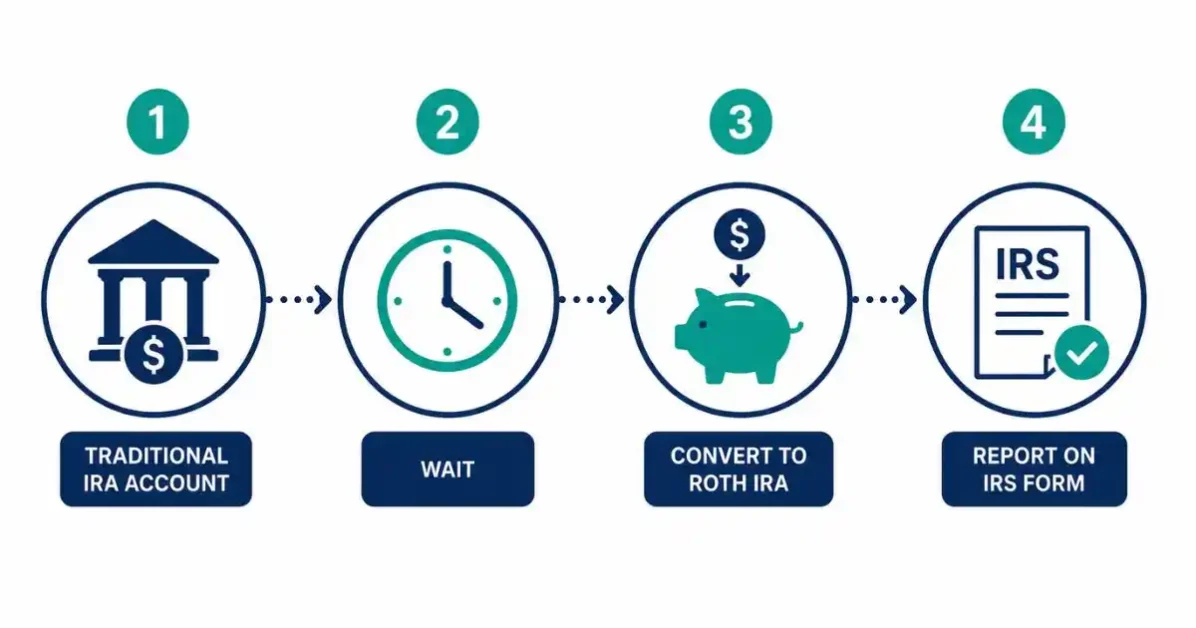

Backdoor Roth IRA step by step for high earners

If your MAGI is above $165,000 (single) or $246,000 (married), you can’t contribute directly to a Roth IRA. The backdoor Roth is the legal workaround.

Step 1: Open a traditional IRA

Open a traditional IRA at your chosen brokerage. Contribute up to $7,000 (or $8,000 if 50+). Don’t deduct this contribution on your taxes. File Form 8606 to document it as a non-deductible contribution.

Step 2: Wait

Some tax advisors recommend waiting a few days to a few weeks before converting. There’s no legal requirement to wait, but it avoids an argument with the IRS about the “step transaction doctrine.”

Step 3: Convert to Roth IRA

Ask your brokerage to convert the traditional IRA to a Roth IRA. This is a Roth conversion. You pay tax on any earnings that occurred between contribution and conversion (usually minimal if you convert quickly).

Step 4: File Form 8606

This form tracks your non-deductible contribution and the conversion. It’s what proves to the IRS you already paid tax on the original $7,000 and owe nothing more on conversion.

The pro-rata rule problem

If you have other pre-tax IRA money sitting anywhere (a rollover IRA from an old 401k, a SEP-IRA), the IRS applies the pro-rata rule. This means your conversion gets taxed proportionally based on your total IRA balance, not just the $7,000 you just put in.

Example: you have $63,000 in a rollover IRA and you add $7,000 non-deductible. Your total IRA balance is $70,000. Only 10% of any conversion is tax-free ($7,000 / $70,000). The other 90% is taxable. The backdoor Roth becomes far less efficient.

The clean workaround: roll your pre-tax IRA money into your current employer’s 401k before doing the backdoor. That clears the pro-rata problem.

File Form 8606 with your return — the full instructions are in IRS Publication 590-A, which covers every IRA contribution rule in one place.

Roth IRA vs backdoor Roth IRA: when each one applies

| Situation | Direct Roth IRA | Backdoor Roth IRA |

|---|---|---|

| MAGI under $150,000 (single) | Yes, contribute directly | Not needed |

| MAGI $150,000 to $165,000 | Partial contribution only | Can top up via backdoor |

| MAGI above $165,000 | Not eligible | Use this route |

| Have pre-tax IRA balance | No issue | Pro-rata rule applies, watch carefully |

| No other IRA accounts | No issue | Clean conversion, no pro-rata problem |

| Self-employed with SEP-IRA | No issue | Pro-rata issue, consider rolling to Solo 401k first |

Roth IRA withdrawal rules after 60

At 60, you’re past the 59½ threshold, so you can take qualified distributions from your Roth IRA completely tax-free and penalty-free, as long as the account has been open for at least 5 years.

That 5-year rule runs from January 1 of the year you made your first Roth contribution, regardless of the actual date you opened it. So if you opened and contributed in December 2022, your 5-year clock started January 1, 2022. You’d hit the 5-year mark on January 1, 2027.

Roth IRA withdrawal rules: what you can take out and when

| Withdrawal Type | Age | Tax | Penalty | Notes |

|---|---|---|---|---|

| Contributions (your principal) | Any age | None | None | Always available, no restrictions |

| Earnings (qualified distribution) | 59½ or older + 5-year rule met | None | None | Completely tax-free |

| Earnings (early withdrawal) | Under 59½ | Yes, as income | 10% | Avoid unless exception applies |

| First-time home purchase | Any age | None on up to $10,000 | None | Lifetime limit of $10,000 earnings |

| Disability | Any age | None | None | Must meet IRS disability definition |

| Death (inherited Roth) | Any age | None | None | 10-year rule applies to non-spouse beneficiaries |

| Required minimum distributions | Never | N/A | N/A | Roth IRA has no RMDs |

What you can always withdraw tax-free

Your original contributions (the money you put in, not earnings) can be withdrawn at any age without tax or penalty. The Roth IRA lets you pull back your principal any time. Only the earnings have restrictions.

What happens if you withdraw earnings early

If you’re under 59½ and take earnings out, you owe income tax on those earnings plus a 10% penalty. Exceptions exist for disability, first-time home purchase (up to $10,000 lifetime), and a few other specific situations.

After 73

No required minimum distributions on a Roth IRA. This is one of the real advantages over a traditional IRA or 401k, which force RMDs starting at 73. You can let a Roth IRA compound indefinitely and pass it to heirs if you don’t need the money.

Roth IRA contribution deadline for 2026

You can contribute to your 2026 Roth IRA any time from January 1, 2026, through April 15, 2027 (the federal tax filing deadline for the 2026 tax year).

If you file for an extension, that does not extend your IRA contribution deadline. The deadline is April 15, 2027, whether or not you request more time to file your return.

One practical move: contribute early in the calendar year rather than waiting until April. Every extra month of tax-free compounding adds up over decades. If you contribute $7,000 in January vs. April, that’s 3 to 4 extra months of growth every single year, compounded over 20 or 30 years.

The math on that is real. Do it early.

How the Roth IRA fits into a Bermuda-based financial plan

Bermuda residents who are US citizens sit in an unusual position: high earning potential, zero local income tax, but full US tax exposure.

The Roth IRA is one of the few tax-advantaged US accounts that still works cleanly for you, provided you manage the earned income issue carefully.

The practical checklist:

- Confirm you have qualifying earned income after any FEIE claim

- Stay within the MAGI limits or plan to use the backdoor route

- Keep a US mailing address with a brokerage that accepts expat clients

- File Form 8606 every year you make a non-deductible contribution

- Coordinate your Roth with any 401k your employer offers

- Talk to a CPA who actually knows expat tax. Not every CPA does.

The Roth IRA won’t solve everything. But for a US expat in Bermuda building long-term wealth, it’s one of the better tools available.

401k vs Roth IRA: which one to fund first in 2026

| Priority | Action | Why |

|---|---|---|

| 1st | Contribute to 401k up to employer match | 100% instant return before any market gains |

| 2nd | Fund Roth IRA up to $7,000 | Tax-free growth, no RMDs, flexible withdrawal |

| 3rd | Max out 401k to $23,500 | Still pre-tax, still growing tax-deferred |

| 4th | Backdoor Roth if income too high | Keeps Roth access open regardless of MAGI |

| 5th | Taxable brokerage account | No contribution limits, but no tax advantage |

FAQ: Roth IRA

- Can Bermuda residents contribute to a Roth IRA?

Yes, if you’re a US citizen with qualifying earned income and MAGI within the limits. The earned income must not be fully excluded by the FEIE.

- Does the foreign earned income exclusion affect Roth IRA eligibility?

Directly. The FEIE reduces your earned income for IRA contribution purposes. If you exclude all your foreign income, your eligible earned income for IRA purposes drops to zero.

- What's the 2026 Roth IRA contribution limit?

$7,000 if you’re under 50. $8,000 if you’re 50 or older.

- Is the backdoor Roth IRA legal?

Yes. It’s a legal strategy. The IRS hasn’t moved to eliminate it. Just file Form 8606 correctly and watch the pro-rata rule if you have other pre-tax IRA accounts.

- Roth IRA vs 401k: which one should a Bermuda expat prioritize?

Get the full employer 401k match first (free money). Then fund a Roth IRA up to $7,000. If you have more to invest after that, go back to the 401k.

Disclaimer:

This article covers general tax information for educational purposes. Your situation depends on your specific income, filing status, and IRA history. Work with a CPA who specializes in US expat taxation before making contribution or conversion decisions.