What to Do If You Haven’t Filed Taxes in Years: Executive Summary

If you haven’t filed taxes in years, you’re confronting more than administrative negligence, you’re facing amaterial threat to wealth preservation, international mobility, and corporate reputation. For sophisticatedinvestors, corporate executives, and global business owners, the accumulation of unfiled tax returns hastransformed into a high-stakes crisis requiring immediate strategic action. As we progress through 2026, taxenforcement mechanisms have evolved into increasingly sophisticated digital ecosystems capable of cross-referencing international financial data with unprecedented precision.

The confluence of enhanced global reporting frameworks, revised IRS compliance initiatives, and tightened international cooperation agreements has fundamentally transformed the landscape of tax enforcement. Thewindow of opportunity for penalty-free resolution continues to narrow, whilst the financial and reputationalconsequences of involuntary discovery escalate exponentially.

This comprehensive guide provides authoritative guidance on navigating the complexities of unfiled tax returns,leveraging available amnesty programmes, and implementing strategic compliance solutions tailored specifically for high-net-worth individuals operating in international jurisdictions.

Unfiled Tax Returns in 2026: Understanding the IRS Enforcement Landscape

The Evolution of IRS Enforcement Capabilities and Unfiled Tax Returns

The Internal Revenue Service has substantially enhanced its technological infrastructure through multi-yearCongressional appropriations exceeding $80 billion. These investments have fundamentally transformed theagency’s capacity to identify, pursue, and prosecute tax non-compliance. The modernised systems nowincorporate artificial intelligence algorithms capable of pattern recognition across disparate financial datasets,cross-border transaction monitoring, and predictive analytics that identify high-probability enforcement targets.

For international investors and executives with complex financial structures, this technological evolutionpresents significant implications. The IRS can now seamlessly correlate:

- Foreign Bank Account Reports (FBARs) with offshore account balances

- Cryptocurrency transactions across decentralised exchanges

- International wire transfers flagged through correspondent banking relationships

- Beneficial ownership information newly required under Corporate Transparency Act provisions

- Real estate transactions recorded in land registries worldwide

Critical 2026 Regulatory Developments Affecting Unfiled Tax Returns

Several pivotal regulatory changes have materialised in 2026, fundamentally altering the risk calculus forindividuals with historical non-compliance:

Passport Revocation Thresholds: For the 2026 tax year, the IRS may trigger passport revocation procedureswhen “seriously delinquent” tax debt exceeds $66,000. This represents a material escalation from previousthresholds and creates immediate complications for internationally mobile executives and investors who dependupon unrestricted travel for business operations.

Enhanced Voluntary Disclosure Framework: The IRS proposed revised penalty structures for the VoluntaryDisclosure Practice (VDP) in early 2026, introducing a 90-day public comment period concluding 22 March2026. The proposed “predictable” penalty framework aims to standardise outcomes for voluntary disclosures,though final regulations remain pending at the time of writing.

Foreign Earned Income Exclusion Increases: The Foreign Earned Income Exclusion (FEIE) threshold hasincreased to $130,000 for the 2025 tax year (filed in 2026). This adjustment provides substantial relief forAmerican expatriates with moderate foreign-sourced income, as many may owe zero actual tax liability oncecompliance is restored through available amnesty programmes.

The Anatomy of Tax Non-Compliance: Understanding Your Exposure

What Happens If You Haven’t Filed Taxes for Multiple Years

The penalty structure for unfiled tax returns operates on an accelerating scale designed to compel immediatecompliance. The failure-to-file penalty constitutes 5% of the unpaid tax liability for each month (or partialmonth) that a return remains outstanding, accumulating to a maximum of 25% over five months.

However, this represents merely the foundation of potential liability. When a return exceeds 60 days past thefiling deadline (including extensions), a minimum penalty applies. For returns due in 2026, this minimumpenalty equals $525 or 100% of the unpaid tax—whichever amount is lesser.

Illustrative Calculation:

Consider a high-net-worth individual with $500,000 in unreported income generating a $150,000 tax liability:

- Month 1: $7,500 penalty (5% of $150,000)

- Month 2: Additional $7,500 (cumulative: $15,000)

- Month 3: Additional $7,500 (cumulative: $22,500)

- Month 4: Additional $7,500 (cumulative: $30,000)

- Month 5: Additional $7,500 (cumulative: $37,500, maximum reached)

This $37,500 penalty applies to a single tax year. For individuals with three, five, or ten years of non-compliance, these penalties compound across multiple years whilst simultaneously accruing daily compoundedinterest on both the underlying tax liability and the assessed penalties.

Planning to hire local employees in Bermuda to satisfy your Economic Substance Requirements? Before you hire, calculateyour exact payroll tax liability for 2026.

Use our free Bermuda Payroll Tax Calculator 2026 — instant results, no signup required.

Failure-to-Pay Penalties: The Compounding Crisis

Distinct from the failure-to-file penalty, the failure-to-pay penalty assesses at 0.5% of unpaid tax per month,continuing indefinitely until the liability is satisfied. This rate escalates to 1% if the tax remains unpaid 10 daysfollowing IRS issuance of a levy notice.

Notably, when both penalties apply concurrently, the failure-to-file penalty reduces by the failure-to-pay amount(0.5%) for any overlapping month, resulting in a combined 5% monthly penalty during the first five months.After the failure-to-file penalty reaches its 25% maximum, the failure-to-pay penalty continues accruing at 0.5%monthly until reaching its own 25% ceiling.

Interest Accumulation: The Silent Wealth Erosion

Interest on unpaid tax liabilities compounds daily at rates established quarterly by the IRS. As of January 2026,the prevailing rate stands at approximately 8% annually for individual underpayments. Unlike penalties, interestcannot be abated under any circumstances except when the IRS commits procedural errors causing delayedassessments.

The compounding mechanism ensures that a £100,000 tax liability left unaddressed for five years transformsinto approximately £148,000 through interest accumulation alone—before considering any applicable penalties.

The Substitute for Return (SFR): When the IRS Files on Your Behalf

Perhaps the most financially damaging consequence of prolonged non-compliance manifests when the IRSexercises its statutory authority under Internal Revenue Code Section 6020(b) to prepare a Substitute for Return(SFR).

SFR Mechanics and Timeline:

Approximately 10-12 months following a unfiled tax return’s due date (including any extension periods), the IRS initiates aprogressive notice sequence:

1. CP59 Notice: Initial communication indicating no return on file

2. CP515 Notice: Follow-up correspondence with escalating language

3. CP516 Notice: Further escalation

4. CP518 Notice: Final pre-SFR warning

5. Notice LT16: Combined balance due and missing return notification

Following this sequence, if the taxpayer fails to respond, the IRS Automated Substitute for Return (ASFR)Program generates an SFR using third-party information reports (Forms W-2, 1099, K-1). The ASFR system—operating on advanced computing platforms at IRS facilities in Austin, Texas; Brookhaven, New York; andFresno, California—automatically calculates tax liability based exclusively on reported income.

Critical Limitations of SFRs:

The IRS constructs SFRs using the least favourable assumptions:

- Filing status: Single or Married Filing Separately (never Married Filing Jointly or Head of Household)

- Standard deduction only (no itemised deductions)

- Zero dependents

- No tax credits (Foreign Tax Credit, Child Tax Credit, education credits, etc.)

- No business expense deductions

- No retirement contribution deductions

- No capital loss deductions

For high-net-worth individuals with sophisticated tax planning structures, an SFR typically overstates actual taxliability by 40-60% or more. The SFR assessment becomes legally enforceable, triggering collection actionsincluding federal tax liens, bank account levies, and wage garnishments.

Post-SFR Notices:

Following SFR preparation, taxpayers receive:

- CP2566 Notice: 30-day notification of proposed assessment

- CP3219N Notice (90-Day Letter): Notice of Deficiency providing final opportunity to contest

Failure to respond results in permanent assessment, though taxpayers retain the right to file accurate returnsreplacing the SFR even after assessment—though penalties and interest continue accruing during deliberation.

Strategic Pathways to Compliance: The 2026 Amnesty Programme Landscape

Streamlined Filing Compliance Procedures: The Premier Expatriate Solution

The Streamlined Filing Compliance Procedures represent the most advantageous compliance pathway forAmerican citizens and green card holders residing abroad who can demonstrate non-willful conduct. Thisprogramme effectively eliminates penalties for qualifying taxpayers whilst requiring disclosure of only the mostrecent compliance years.

Streamlined Foreign Offshore Procedures (SFOP): Eligibility Criteria

To qualify for SFOP, taxpayers must satisfy these requirements:

1. Physical Presence Requirement: Resided outside the United States for at least 330 days during one ofthe last three calendar years covered by the submission

2.Non-Willfulness: Previous failures to file tax returns and FBARs resulted from non-willful conduct(genuine ignorance, reliance on incompetent advice, or reasonable misunderstanding of obligations)

3.Voluntary Disclosure: Submission occurs before IRS contact regarding the specific years or issues

4.Current Year Compliance: Taxpayer commits to future timely filing

Required Submissions:

- Three most recent delinquent unfiled tax returns (as of January 2026: tax years 2022, 2023, and 2024)

- Six most recent delinquent FBARs (FinCEN Form 114)

- Form 14653: Certification of non-willful conduct with narrative explanation

Penalty Relief:

Qualifying taxpayers receive complete elimination of:

- Failure-to-file penalties

- Failure-to-pay penalties

- FBAR penalties (which can otherwise reach $10,000 per account per year for non-willful violations, or50% of account balance for willful violations)

- Accuracy-related penalties

Tax and interest remain due on any outstanding liability. However, with the 2025 FEIE threshold at $130,000,many expatriates discover zero actual tax liability after applying this exclusion alongside Foreign Tax Creditsfor taxes paid to residence countries.

Strategic Considerations:

The Streamlined Procedures were established in 2014 and have processed over 60,000 successful submissions.However, these programmes exist at IRS discretion and could be modified or terminated without advancenotice. The March 2018 closure of the Offshore Voluntary Disclosure Program (OVDP) demonstrated theagency’s willingness to eliminate favourable compliance pathways when utilisation reaches critical mass.

Sophisticated advisors recommend immediate action for eligible taxpayers rather than awaiting potentialprogramme modifications.

Streamlined Domestic Offshore Procedures (SDOP): For US Residents

American taxpayers residing within the United States may access modified Streamlined Procedures, thoughwith less favourable terms than SFOP:

Key Differences from SFOP:

- 5% penalty on the highest aggregate foreign account balance during the covered years

- Same filing requirements (three years returns, six years FBARs)

- Non-willfulness certification still required

The 5% penalty, whilst modest compared to standard FBAR penalties potentially exceeding 50% of accountbalances, still represents material cost for individuals with substantial offshore holdings. A taxpayer with $10million in foreign accounts faces a $500,000 penalty under SDOP.

Delinquent FBAR Submission Procedures: For Compliant Filers

Taxpayers who filed all required unfiled tax returns but inadvertently omitted FBAR filings may utilise the DelinquentFBAR Submission Procedures:

Eligibility Requirements:

- All required tax returns timely filed

- All income from foreign accounts properly reported on returns

- No current civil examination or criminal investigation

- No prior IRS contact regarding delinquent FBARs

Submission Requirements:

- Delinquent FBARs for all applicable years (up to six years)

- Brief statement explaining reasonable cause for late filing

This procedure typically results in zero penalties for qualifying taxpayers, though the IRS reserves discretion toassess penalties if reasonable cause is inadequate.

Delinquent International Information Return Submission Procedures for Delinquent Tax Filings

Similar relief exists for taxpayers who filed returns and FBARs but omitted other international informationforms:

- Form 8938 (Statement of Specified Foreign Financial Assets)

- Form 5471 (Information Return of US Persons with Respect to Certain Foreign Corporations)

- Form 3520 (Annual Return to Report Transactions with Foreign Trusts and Receipt of Certain ForeignGifts)

- Form 8621 (Information Return by a Shareholder of a Passive Foreign Investment Company or QualifiedElecting Fund)

Standard penalties for these forms range from $10,000 to $50,000 annually, with some violations generatingpenalties equal to 40% of unreported asset values. The procedures provide penalty relief when reasonable causeexists.

Voluntary Disclosure Practice (VDP): For Willful Non-Compliance

Taxpayers unable to certify non-willfulness must pursue the Voluntary Disclosure Practice. This programmeaccepts willfully non-compliant taxpayers seeking to avoid criminal prosecution whilst resolving civil taxobligations.

VDP Framework:

- Submission of six to eight years of returns (IRS determines exact requirement)

- Payment of all unfiled tax returns, interest, and applicable penalties

- Substantial penalty assessment (typically 20-40% of highest aggregate account balance)

- Cooperation with IRS examination process

The 2026 proposed penalty framework aims to increase predictability, though final regulations remain subject tomodification following the public comment period concluding 22 March 2026.

Criminal Prosecution Risk Mitigation:

VDP’s primary benefit lies in near-total elimination of criminal prosecution risk. Internal Revenue Manualprovisions specify that VDP participants generally avoid criminal referral absent extraordinary aggravatingfactors (money laundering, terrorism financing, organised crime connections).

For ultra-high-net-worth individuals with potential willfulness exposure, VDP represents the sole pathway toresolution with reasonable assurance against incarceration.

IRS Fresh Start Initiative: Debt Management Solutions

Taxpayers achieving filing compliance but unable to immediately satisfy outstanding liabilities may accessFresh Start Initiative programmes:

Offer in Compromise (OIC):

Settlement of total tax debt for less than full amount owed based on:

- Doubt as to liability

- Doubt as to collectability

- Effective tax administration (exceptional circumstances)

The IRS evaluates OIC applications using “Reasonable Collection Potential” formulas incorporating:

- Net realisable equity in assets

- Future income potential

- Necessary living expenses

Acceptance rates historically approximate 40%, with successful offers settling debts for 10-30% of originalbalances. However, the IRS scrutinises OIC applications from high-income professionals and business ownersintensely, often rejecting applications from individuals with substantial income potential.

Instalment Agreements:

Monthly payment plans permitting debt resolution over time:

- Guaranteed instalments: Liabilities under $10,000

- Streamlined instalments: Liabilities under $100,000 (2026 threshold increase)

- Partial payment instalments: Extended agreements with payments insufficient to satisfy full liabilitybefore collection statute expiration

The failure-to-pay penalty reduces from 0.5% to 0.25% monthly when valid instalment agreements exist.

Currently Not Collectible (CNC) Status:

Temporary suspension of collection activities for taxpayers demonstrating that payment would prevent basicliving expense coverage. CNC status doesn’t eliminate liability but halts active collection whilst financialcircumstances remain distressed.

Practical Implementation: Strategic Steps for Achieving Compliance

Phase One: Comprehensive Financial Reconstruction

Document Assembly:

Gather all available financial records:

- Bank statements (domestic and foreign)

- Brokerage statements

- Investment account records

- Business financial statements

- Cryptocurrency transaction logs

- Real estate transaction documentation

- Foreign pension and retirement account statements

IRS Transcript Acquisition:

Request IRS Wage and Income Transcripts for all relevant years. These transcripts reflect all Forms W-2, 1099,and K-1 filed with your taxpayer identification number, providing foundation for income reconstruction whenoriginal records are unavailable.

Transcripts are accessible through:

- IRS online account (irs.gov)

- Form 4506-T submission

- Third-party authorisation to tax professionals

Gap Analysis:

Compare IRS transcripts against personal records to identify:

- Unreported income sources

- Missing tax years

- Inconsistencies requiring explanation

- Foreign accounts requiring FBAR disclosure

Phase Two: Programme Selection and Eligibility Verification

Non-Willfulness Assessment:

Critically evaluate the facts and circumstances surrounding historical non-filing:

- Were you aware of filing obligations?

- Did you receive professional advice suggesting filing was unnecessary?

- Was non-filing the result of ignorance regarding US citizenship-based taxation?

- Were foreign accounts disclosed on professional advice that it was sufficient?

Non-willfulness represents “conduct that is due to negligence, inadvertence, or mistake or conduct that is theresult of a good faith misunderstanding of the requirements of the law.” Mere disagreement with tax policy doesnot constitute non-willfulness.

Residency Verification:

For SFOP eligibility, confirm 330-day physical presence outside the United States using:

- Passport entry/exit stamps

- Foreign residence permits

- Employment records

- School enrolment documentation for dependent children

- Lease agreements

- Utility bills

Professional Consultation:

Engage experienced international tax counsel with substantial Streamlined Procedures experience. The non-willfulness certification represents the most scrutinised element of submissions, and inadequate explanationsresult in rejection and referral to more punitive programmes or examination.

Phase Three: Return Preparation and Submission

Return Preparation Priorities:

For the three required tax years under Streamlined Procedures:

1.Accurate Income Reporting: Include all worldwide income regardless of source

2.Foreign Tax Credit Optimisation: Claim credits for foreign taxes paid to avoid double taxation

3.FEIE Maximisation: Where applicable, exclude eligible foreign earned income

4.Foreign Account Reporting: Accurately disclose all foreign financial accounts on Schedule B and Form8938

5.International Information Returns: Complete all required forms (5471, 3520, 8621, etc.)

FBAR Completion:

File delinquent FBARs electronically through FinCEN’s BSA E-Filing System. Required disclosures include:

- Maximum account balances during calendar year

- Account numbers

- Financial institution details

- Account ownership type

Certification Drafting:

The Form 14653 certification and narrative explanation demand meticulous attention. Effective narratives:

- Provide specific facts demonstrating non-willfulness

- Avoid conclusory statements (“I didn’t know” without supporting facts)

- Reference specific advice received or reasonable beliefs held

- Demonstrate genuine remorse and commitment to future compliance

Submission Methodology:

Mail complete Streamlined Procedure packages to:

- SFOP: Internal Revenue Service, 3651 South I-H 35, Stop 6063 AUSC, Austin, TX 78741

- SDOP: Same address with different marking requirements

Submission via certified mail with return receipt provides proof of timely filing.

Phase Four: Post-Submission Management

IRS Processing Timeline:

Streamlined submissions typically require 6-12 months for processing. During this period:

- Maintain detailed records of submission

- Monitor IRS account transcripts for processing activity

- Respond promptly to any IRS correspondence

- Continue timely filing of current-year returns

Potential Outcomes:

1.Silent Acceptance: Most common outcome; IRS processes returns without contact

2.Request for Additional Information: IRS requests supporting documentation or clarification

3.Rejection and Reclassification: IRS determines conduct was willful; redirects to VDP or examination

4.Partial Acceptance: IRS accepts some years whilst examining others

Rejection Implications:

Rejection from Streamlined Procedures doesn’t preclude alternative resolution, but eliminates penalty-freeoption. Rejected taxpayers may:

- Enter VDP with higher penalties

- Face standard examination with full penalties

- Contest IRS determination through appeals procedures

Advanced Considerations for Sophisticated Investors

Cross-Border Business Structures and Controlled Foreign Corporations

American taxpayers with ownership in foreign corporations face extraordinary complexity through Subpart Fand Global Intangible Low-Taxed Income (GILTI) provisions. Form 5471 reporting requirements imposepenalties of $10,000 per corporation per year for non-compliance, with additional penalties of $10,000 permonth continuing after IRS notification.

Planning Considerations:

- Evaluate whether foreign entities qualify as Controlled Foreign Corporations (CFCs)

- Assess Subpart F income requiring current US taxation

- Calculate GILTI inclusions under current law

- Consider implications of 2017 Tax Cuts and Jobs Act transition tax on accumulated foreign earnings

- Analyse foreign tax credit availability and limitation calculations

Passive Foreign Investment Company (PFIC) Complications

Foreign mutual funds, exchange-traded funds, insurance products, and pooled investment vehicles frequentlyqualify as PFICs, triggering punitive tax treatment absent timely elections.

Compliance Challenges:

- Excess distribution regime imposing tax plus interest charge

- Annual reporting requirements on Form 8621

- Qualified Electing Fund (QEF) elections permitting current income taxation

- Mark-to-Market (MTM) elections for marketable securities

Many taxpayers discover PFIC holdings years after acquisition, often through foreign insurance policies orforeign pension plans. Retroactive QEF elections are generally prohibited, leaving taxpayers subject todisadvantageous excess distribution calculations.

Real Estate Holdings and Tax Lien Properties

High-net-worth investors frequently acquire real estate through tax lien certificates and deed sales. Propertiesacquired through these mechanisms present specific compliance considerations:

Tax Lien Investment Structures:

When properties fail to generate redemption (owner payback), investors may acquire title through foreclosure.This creates:

- Ordinary income from interest received during redemption period

- Capital asset treatment upon property acquisition

- Potential depreciation recapture upon eventual sale

- Self-employment tax considerations if systematic acquisition occurs

State-Specific Variations:

Tax lien investment regulations vary substantially by jurisdiction. Investors operating across multiple statesmust navigate:

- Interest rate limitations (ranging from 0% to 24% annually)

- Redemption periods (12 months to 3 years typically)

- Foreclosure procedures and timelines

- Junior lien priority resolution

Enhanced due diligence proves essential, as properties with environmental contamination, structural defects, ortitle defects create liability exceeding invested capital.

Cryptocurrency and Digital Asset Reporting

The IRS treats cryptocurrency as property rather than currency, creating reporting obligations on everytransaction regardless of magnitude. High-volume traders may generate thousands of taxable events annually.

Compliance Requirements:

- Report all dispositions on Form 8949 and Schedule D

- Calculate basis and gain/loss for each transaction

- Track hard forks and airdrops as ordinary income

- Maintain detailed records of wallet addresses and transaction histories

The Infrastructure Investment and Jobs Act of 2021 imposed expansive information reporting requirements oncryptocurrency exchanges and brokers, effective in phases through 2026. Enhanced third-party reporting willenable IRS cross-referencing against taxpayer returns with unprecedented precision.

Risk Mitigation and Common Pitfalls

The Perils of Delayed Action

Statute of Limitations Misconceptions:

A pervasive myth suggests that unfiled tax returns become uncollectible after a specified period. This reflectsfundamental misunderstanding of limitations statutes:

- Assessment Limitation:

- Generally three years from return filing date (not due date)

- Collection Limitation:

- Ten years from assessment date

- Criminal Prosecution Limitation:

- Generally six years from return due date

Critical Reality: When no unfiled tax returns, the assessment statute never commences. The IRS retains indefiniteauthority to assess tax on unfiled years. The collection statute similarly never begins running until assessmentoccurs.

Taxpayers who “wait out” the IRS discover that decades-old liabilities remain enforceable, often with penaltiesand interest exceeding the original tax by multiples.

The Expensive Fallacy of “Waiting for Amnesty

Historical Precedent:

The 2009-2018 Offshore Voluntary Disclosure Program (OVDP) generated billions in revenue and encouragedvoluntary compliance. Many taxpayers deferred action, anticipating more favourable successor programmes.

The OVDP closed permanently in September 2018. No general tax amnesty has emerged as replacement. TheStreamlined Procedures, whilst generous, provide more limited relief than OVDP in certain circumstances andcould terminate without advance notice.

Strategic Implications:

Available programmes represent the most favourable resolution terms likely to exist. Delaying action pendinghypothetical future amnesties constitutes high-risk speculation exposing taxpayers to:

- Programme elimination or restriction

- Enhanced penalties under revised frameworks

- Involuntary IRS discovery triggering maximum penalties without amnesty eligibility

Documentation Inadequacy and Reconstruction Challenges

Common Documentation Failures:

- Incomplete bank records for dormant foreign accounts

- Lost brokerage statements for liquidated positions

- Unavailable basis information for inherited property

- Missing cryptocurrency exchange records from defunct platforms

Remediation Strategies:

- Contact foreign financial institutions directly for historical statements

- Utilise tax treaty exchange of information provisions

- Reconstruct transactions through blockchain explorers for cryptocurrency

- Obtain valuations from professional appraisers for inherited property

- Request IRS third-party information through transcript services

Incomplete documentation should never prevent filing. Reasonable good-faith estimates with disclosedassumptions prove vastly superior to continued non-filing.

The False Security of Nominee Structures

Ineffective Strategies:

Some non-compliant taxpayers attempt to obscure ownership through:

- Nominee ownership arrangements with foreign relatives

- Shell companies in non-reporting jurisdictions

- Undisclosed beneficial ownership in foreign trusts

Reality of Modern Enforcement:

- Common Reporting Standard (CRS) facilitates automatic exchange of financial account informationamong 100+ countries

- Foreign Account Tax Compliance Act (FATCA) requires foreign financial institutions to report USaccount holders

- Beneficial ownership registries increasingly accessible to tax authorities

- Penalties for willful non-disclosure can reach 50% of account balances annually plus criminal prosecution

Professional Representation: Investment vs. Expense

Cost Considerations:

Quality international tax representation for Streamlined Procedure submissions typically ranges from £15,000 to£50,000 depending on complexity. VDP matters frequently exceed £100,000 in professional fees.

Value Proposition:

Consider potential consequences of inadequate representation:

- Incorrectly prepared returns generating subsequent examination

- Inadequate non-willfulness explanations triggering rejection

- Missed opportunities for tax credit optimisation

- Criminal exposure from DIY voluntary disclosure attempts

For matters involving potential six-figure or seven-figure penalties—or criminal prosecution risk—qualifiedrepresentation represents essential risk mitigation rather than discretionary expense.

Sector-Specific Guidance: Tailored Strategies for Distinct Investor Profiles

International Executives and Dual-Status Taxpayers

Executives with international assignments frequently encounter dual-status taxation years, creating complexityin determining filing obligations and applicable exclusions.

Key Considerations:

- First-year and last-year choice elections under tax treaties

- Foreign housing exclusion calculations

- Totalisation agreement impacts on self-employment tax

- Stock option exercise timing and source-of-income rules

- Departure tax implications for long-term residents

Private Equity and Venture Capital Investors

Investment in foreign private equity funds and venture capital structures frequently generates:

- PFIC classification issues

- CFC ownership through fund structures

- Section 1256 contract reporting

- Qualified Small Business Stock exclusion considerations

Ultra-High-Net-Worth Individuals with Multi-Jurisdictional Exposure

Individuals with £50 million+ net worth across multiple countries face extraordinary compliance burdens:

- Foreign trust reporting (Forms 3520 and 3520-A)

- Foreign partnership interests (Form 8865)

- Controlled foreign corporation ownership (Form 5471)

- Transfer pricing documentation for intercompany transactions

- Exit tax planning under Section 877A for potential expatriation

Accidental Americans

Individuals with US citizenship through birth but lifelong foreign residence represent unique compliancechallenges:

- Potential eligibility for Streamlined Procedures

- Limited US economic connection reducing actual tax liability

- Foreign pension classification issues (qualified vs. non-qualified)

- Renunciation of citizenship as long-term solution

- Certificate of Loss of Nationality acquisition procedures

Comparative Analysis: Programme Selection Framework

Decision Matrix: Streamlined vs. VDP vs. Traditional Voluntary Disclosure

| Factor | Streamlined Procedures | Voluntary DisclosurePractice | Standard Filing |

| WillfulnessRequirement | Non-willful conduct only | Accepts willful conduct | Not applicable |

| Years Required | 3 tax returns, 6 FBARs | 6-8 years (IRS determines) | All unfiled yearsrecommended |

| Penalty Relief | Complete elimination | 20-40% offshore penalty | Full statutory penalties |

| CriminalProtection | Not primary purpose | Near-absolute protection | No protection |

| Processing Time | 6-12 months typically | 12-24 months minimum | Varies |

| Professional Fees | £15,000-£50,000 | £50,000-£200,000+ | £5,000-£25,000 |

| Audit Risk | Minimal if properly prepared | Guaranteed examination | Moderate to high |

| OptimalCandidate | Expatriate with unreportedforeign accounts throughignorance | US resident with substantialundisclosed offshore assets | Simple unfiled years withoutoffshore complications |

Jurisdictional Variations: State Tax Considerations

Whilst federal compliance represents the primary concern, state tax obligations demand parallel attention:

High-Risk States:

- California: 20-year collection statute; aggressive residency audits

- New York: Statutory resident rules based on days present

- Illinois: Complex nexus standards for business income

- Massachusetts: Stringent temporary assignment rules

Strategic Planning:

- Evaluate state residency status for all relevant years

- Assess statutory resident vs. domiciliary classification

- Consider state amnesty programmes operating independently of federal initiatives

- Analyse whether state has income tax treaty with US (none currently exist)

Property Investment and Tax-Delinquent Real Estate Strategies

Understanding the Tax Lien Investment Landscape

Tax lien certificates represent an alternative investment class particularly attractive to high-net-worthindividuals seeking:

- Government-backed security

- Predictable returns (statutory interest rates)

- Minimal management requirements

- Potential property acquisition at substantial discounts

2026 Market Dynamics:

Recent regulatory developments substantially altered tax lien investing fundamentals:

- Alabama’s 2024 legislative changes introduced online auctions, extended foreclosure timelines, andenhanced compliance requirements

- Nebraska Supreme Court rulings created potential surplus equity compensation obligations for investors

- Institutional investor participation has escalated, with approximately 80% of certificates purchased byNational Tax Lien Association members

- Competitive bidding frequently drives interest rates below 5% in premium markets

Investment Mechanics:

When property owners fail to remit property taxes, local governments place liens securing the debt. Rather thanawaiting payment, jurisdictions auction these liens to private investors who pay the outstanding obligation. Theproperty owner must subsequently repay the investor with statutory interest, or the investor may eventuallyforeclose to acquire title.

Returns and Risks:

Interest rates vary by state law, ranging from 0% (highly competitive jurisdictions) to 24% annually. However,actual foreclosure rates approximate 4% nationally, with foreclosed properties predominantly comprising vacantland or abandoned structures rather than occupied residences.

Due Diligence Imperatives for Tax Lien Investments

Property Condition Assessment:

Before bidding:

- Physically inspect properties or engage local representatives

- Evaluate structural integrity and deferred maintenance

- Identify environmental contamination risks

- Assess marketability and comparable sales data

Title and Lien Verification:

- Research all junior liens surviving foreclosure

- Confirm no federal tax liens (IRS liens can supersede local tax liens under certain circumstances)

- Verify no bankruptcy filings staying foreclosure proceedings

- Assess mechanics’ liens or other senior encumbrances

Regulatory Compliance:

Each state imposes distinct requirements:

- Redemption periods: 6 months to 3 years

- Interest calculation methodologies: Simple vs. compound

- Notice requirements for foreclosure initiation

- Auction formats: Bid-down interest, premium bidding, or rotational assignment

Tax Treatment of Tax Lien Investments

Income Recognition:

Interest received during redemption period constitutes ordinary income, taxable in the year received regardlessof taxpayer’s accounting method.

Property Acquisition:

Upon foreclosure and title acquisition:

- Basis equals original lien purchase price plus subsequent tax payments

- Holding period commences on foreclosure date

- Capital gain/loss treatment applies on eventual sale

- Depreciation available if property converted to rental use

Self-Employment Tax Considerations:

Systematic tax lien acquisition and property management may constitute a trade or business, subjecting netearnings to self-employment tax at 15.3% on amounts up to the Social Security wage base.

1031 Exchange Opportunities:

Furthermore, properties acquired through tax lien foreclosure qualify as real property eligible for Section 1031 like-kind exchange treatment. Consequently, this permits a full tax deferral on appreciation, provided the asset is exchanged for similar investment property.

Comprehensive FAQ: Advanced Compliance Questions

What to do if you haven’t filed taxes in years: Step 1

What happens if I haven’t filed taxes in 10 years?

After a decade of non-compliance, the IRS will have likely prepared Substitute for Returns for multiple years,each with maximum penalties and accrued interest. Your exposure includes 25% failure-to-file penalties peryear, 25% failure-to-pay penalties per year, accuracy-related penalties potentially reaching 20%, and interestcompounding daily at approximately 8% annually.

The IRS typically prioritises compliance for the most recent six years, though retains indefinite authority toassess tax on unfiled years. Begin by requesting Wage and Income Transcripts for all ten years, then engagequalified international tax counsel to evaluate Streamlined Procedures eligibility or alternative compliancepathways.

Can the IRS pursue me for taxes from 20 years ago?

Yes, absolutely. The statute of limitations never commences when returns remain unfiled. The IRS retainsperpetual authority to assess tax on unfiled years regardless of age. Whilst the agency typically focusesenforcement resources on more recent years, discovery of decades-old non-compliance through third-partyinformation matching or whistleblower reports can trigger comprehensive examination of all unfiled tax returns years.

Additionally, the 10-year collection statute only begins upon assessment. Taxes assessed on 20-year-old incomeremain collectible for the full 10-year period following assessment, creating potential 30-year total exposure.

Is there an IRS amnesty programme in 2026?

The Streamlined Filing Compliance Procedures remain available as of January 2026 and represent the closestequivalent to traditional amnesty. These procedures eliminate all penalties for qualifying non-willful taxpayers.Additionally, the Voluntary Disclosure Practice (VDP) provides penalty reduction and criminal prosecutionprotection for willful non-compliance.

No general tax amnesty currently exists. The proposed VDP penalty framework modifications expected tofinalise after the March 2026 comment period may provide increased certainty, though likely not morefavourable terms than current provisions. Historical precedent demonstrates that programmes can terminatewithout advance notice, making immediate action prudent for eligible taxpayers.

How do I calculate penalties for 3 years of unfiled returns?

Penalties accumulate as follows for each unfiled tax returns:

Year 1:

- Failure-to-file: 25% of tax owed (maximum reached after 5 months)

- Failure-to-pay: 0.5% per month continuing indefinitely until paid

- Interest: Approximately 8% annually, compounded daily

- Minimum penalty (if return over 60 days late): $525 or 100% of tax, whichever is less

Years 2 and 3: Identical calculations applied independently

Example Calculation:

£100,000 tax owed for each of three years, unfiled for entire period:

- Year 1 failure-to-file: £25,000

- Year 2 failure-to-file: £25,000

- Year 3 failure-to-file: £25,000

- Combined failure-to-pay (assuming 36 months): £18,000

- Interest on tax and penalties: Approximately £60,000

- Total exposure: £353,000 on £300,000 tax

Streamlined Procedures eliminate these penalties entirely for qualifying taxpayers.

What to do if you haven’t filed taxes in years: Step 2

What is the “haven’t filed taxes in 10 years Reddit” community discussing?

Online communities on platforms including Reddit provide anecdotal experiences from individuals navigatingtax compliance after extended non-filing periods. Common themes include:

- Fear regarding IRS enforcement actions (wage garnishment, bank levies, passport revocation)

- Confusion regarding programme eligibility and selection

- Cost concerns regarding professional representation

- Relief upon discovering Streamlined Procedures and penalty elimination

- Warnings regarding inadequate DIY compliance attempts

Whilst these communities provide emotional support, the legal and financial advice quality varies dramatically.Professional guidance from qualified international tax attorneys with substantial Streamlined Proceduresexperience proves essential for high-net-worth individuals with complex offshore holdings.

How do I catch up on 5 years of unfiled taxes?

A systematic five-step process ensures optimal outcomes:

Step 1: Transcript Acquisition (Week 1) Request IRS Wage and Income Transcripts online or via Form 4506-T for all five years.

Step 2: Financial Reconstruction (Weeks 2-4) Gather bank statements, brokerage records, foreign accountdocumentation, cryptocurrency transaction logs, and business financial statements. Reconcile against IRStranscripts to identify gaps.

Step 3: Programme Evaluation (Week 5) Assess eligibility for Streamlined Procedures (requires non-willfulness and either foreign residency or 5% penalty acceptance for US residents). Evaluate VDP ifwillfulness concerns exist.

Step 4: Professional Engagement (Week 6) Retain experienced international tax counsel with demonstrableStreamlined Procedures expertise. Verify their background through bar association records and client references.

Step 5: Return Preparation and Submission (Weeks 7-12) For unfiled tax returns, prepare accurate filings that incorporate all worldwide income, optimising Foreign Tax Credits and the Foreign Earned Income Exclusion (FEIE) where applicable. Complete Form 14653 (non-willfulness certification) with a detailed factual narrative, file any delinquent FBARs electronically, and submit the complete package via certified mail.

Timeline assumes full cooperation and reasonable documentation availability. Complex situations involvingCFCs, PFICs, or foreign trusts may extend timelines substantially.

Can I invest in houses that haven’t paid taxes?

Yes, tax lien certificate investment and tax deed acquisition represent established alternative investmentstrategies. However, sophisticated due diligence proves essential:

Tax Lien Certificates: Purchase the government’s security interest in properties with delinquent taxes. Earnstatutory interest (varying by state) when owners redeem. Potentially foreclose to acquire title if redemptiondoesn’t occur.

Tax Deeds: Purchase property outright at auction following unsuccessful tax lien redemption. Acquireimmediate title subject to redemption rights in some jurisdictions.

Critical Risks:

- Properties frequently suffer substantial deferred maintenance or abandonment

- Environmental contamination liability transfers with title

- Junior liens may survive foreclosure in some jurisdictions

- Occupied properties require costly eviction proceedings

- Marketability challenges in depressed areas

Tax Treatment:

Interest from redeemed liens constitutes ordinary income. Properties acquired through foreclosure receivecapital asset treatment, with basis equal to lien purchase price plus subsequent tax payments. Depreciationbecomes available if converted to rental use.

Regulatory Landscape 2026:

Recent state legislative modifications (Alabama’s online auction requirements, Nebraska’s surplus equitycompensation mandates) create evolving compliance obligations requiring jurisdictional expertise.

What to do if you haven’t filed taxes in years: Step 3

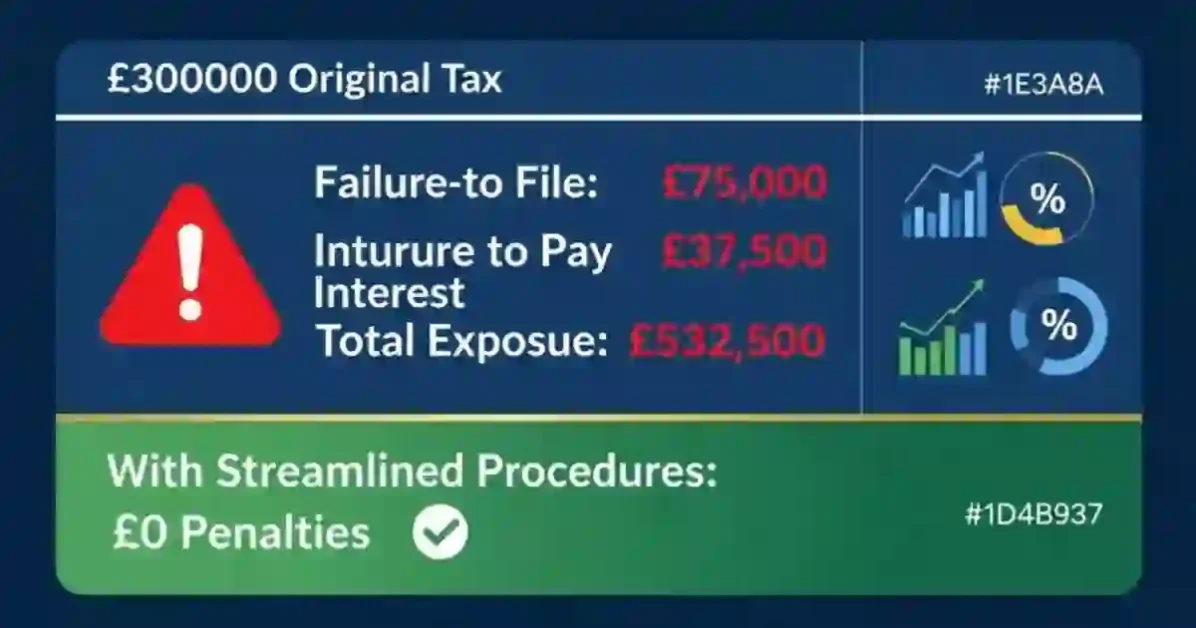

What penalties apply if I haven’t filed taxes for 3 years?

Understanding what to do if you haven’t filed taxes in years starts with recognising that unfiled tax returns trigger standard penalties after three years of non-compliance, including:

Failure-to-File Penalty:

- 5% of unpaid tax per month for each year

- Maximum 25% per year (£25,000 on £100,000 tax)

- Combined three-year maximum: £75,000 on £300,000 tax

Failure-to-Pay Penalty:

- 0.5% of unpaid tax per month continuing beyond five months

- Maximum 25% per year

- Reduced to 0.25% monthly if instalment agreement exists

Interest:

- Approximately 8% annually as of January 2026

- Compounded daily on tax and penalties

- Cannot be abated except for IRS errors

Accuracy-Related Penalties:

- 20% of underpayment attributable to negligence or substantial understatement

- 40% if gross valuation misstatement exists

FBAR Penalties (if applicable):

- £10,000 per account per year for non-willful violations

- Greater of £100,000 or 50% of account balance per year for willful violations

Total Potential Exposure:

For £300,000 combined tax liability:

- Failure-to-file: £75,000

- Failure-to-pay: £37,500

- Accuracy-related: £60,000

- Interest: £60,000+

- Total: £532,500+ on £300,000 tax

Streamlined Procedures eliminate all penalties except interest for qualifying taxpayers.

Will I go to jail for not filing taxes?

Understanding what to do if you haven’t filed taxes in years starts with a Criminal prosecution for tax evasion remains relatively uncommon, with the IRS pursuing approximately2,000-3,000 criminal investigations annually from 150+ million individual taxpayers. However, certain factorssubstantially elevate prosecution risk:

High-Risk Indicators:

- Willful evasion of known tax obligations

- Affirmative acts of concealment (false statements, destroyed records, nominee structures)

- Large dollar amounts (typically £70,000+ tax per year)

- Multiple years of deliberate non-compliance

- Public prominence or professional position in tax/finance/law

- Prior IRS contact ignored

Criminal Penalties:

Tax evasion (IRC Section 7201) carries maximum penalties of:

- Five years imprisonment per count

- £250,000 fines (£500,000 for corporations)

- Costs of prosecution

Protection Through Voluntary Disclosure:

Participation in the Voluntary Disclosure Practice (VDP) provides near-absolute protection from criminalprosecution. The IRS Internal Revenue Manual specifies that voluntary disclosures generally preclude criminalreferral absent extraordinary circumstances (terrorism, money laundering, organised crime).

Critical requirement: Disclosure must occur before IRS contact regarding the specific years or issues. Onceexamination commences or criminal investigation initiates, voluntary disclosure becomes unavailable.

What if I can’t afford to pay the taxes I owe?

Understanding what to do if you haven’t unfiled tax returns in years starts with Tax payment inability should never prevent filing. The IRS provides multiple resolution options for taxpayersachieving filing compliance but unable to immediately satisfy liabilities:

Instalment Agreements:

Monthly payment plans available for qualified taxpayers:

- Guaranteed: Liabilities under £10,000

- Streamlined: Liabilities under £100,000 (2026 threshold)

- Partial payment: Extended agreements with monthly amounts insufficient to satisfy full liability beforecollection statute expiration

Acceptance establishes legitimacy and halves the ongoing failure-to-pay penalty from 0.5% to 0.25% monthly.

Offer in Compromise (OIC):

Settlement of total debt for less than full amount based on:

- Reasonable Collection Potential calculations

- Asset net realisable value

- Future income potential over 12-24 months

- Necessary living expenses per IRS standards

Acceptance rates approximate 40%, with successful offers settling debts for 10-30% of original balances. Ultra-high-net-worth individuals with substantial income potential face intensive scrutiny and lower acceptanceprobability.

Currently Not Collectible (CNC) Status:

Temporary suspension of collection activities for taxpayers unable to meet basic living expenses whilst payingtax debt. CNC status doesn’t eliminate liability but halts active enforcement whilst financial distress continues.

Bankruptcy Consideration:

Limited circumstances permit tax debt discharge through bankruptcy:

- Tax debt older than three years

- Returns filed at least two years before bankruptcy

- Assessment at least 240 days before filing

- No fraud or willful evasion

Chapter 7 bankruptcy can discharge qualifying older tax debts, though recent liabilities remain non-dischargeable.

Are there penalties for not filing FBAR?

Foreign Bank Account Report (FBAR) penalties represent among the most severe in the tax code:

Non-Willful Violations:

- Up to £10,000 per account per year

- IRS possesses discretion to assess lower amounts or eliminate penalties entirely based on reasonablecause

Willful Violations:

- Greater of £100,000 or 50% of account balance per year

- Criminal penalties: Up to 10 years imprisonment plus £500,000 fines

Penalty Calculation Example:

Individual with £5 million aggregate foreign account balance, unreported for six years:

- Non-willful scenario: £60,000-£300,000 (£10,000 per year, variable based on account count)

- Willful scenario: £15,000,000 (£2.5 million × 6 years at 50% annual penalty)

Relief Through Streamlined Procedures:

SFOP (foreign residents): Complete FBAR penalty eliminationSDOP (US residents): 5% penalty on highest aggregate balance (£250,000 on £5 million)Delinquent FBAR Procedures: Zero penalty for taxpayers who timely filed returns

The extraordinary penalty exposure makes FBAR compliance essential for all taxpayers with foreign accountsignature authority or beneficial ownership.

How long does the Streamlined Procedure process take?

Processing timelines vary based on submission completeness and IRS workload:

Standard Timeline:

- Submission preparation: 8-12 weeks with professional guidance

- IRS processing: 6-12 months typically

- Additional information requests: Add 2-4 months if IRS requests clarification

- Final resolution: 8-18 months from initial engagement to completion

Factors Accelerating Processing:

- Complete, well-organised submissions with comprehensive documentation

- Detailed non-willfulness narratives with specific supporting facts

- All required forms and schedules included

- Certified mail submission with tracking confirmation

Factors Delaying Processing:

- Incomplete submissions missing required forms or schedules

- Insufficient documentation for reported positions

- Vague or conclusory non-willfulness explanations

- High complexity (CFCs, PFICs, foreign trusts)

- IRS resource constraints during peak filing season

Post-Submission Actions:

Continue timely filing current-year returns whilst submission processes. Monitor IRS online account fortranscript updates. Respond immediately to any IRS correspondence. Maintain detailed records of allsubmission materials.

Most submissions resolve through “silent acceptance”—IRS processes returns without contact. This representsoptimal outcome, typically confirmed through transcript updates showing assessment of any tax due.

Professional Disclaimer and Legal Notices

Jurisdictional Limitations:

This guide provides general educational information regarding US federal tax compliance and should not beconstrued as legal, tax, or financial advice applicable to specific circumstances.unfiled tax returns varies substantially byjurisdiction, with material differences between federal and state requirements, international tax treatyprovisions, and foreign country obligations.

Professional Advice Requirement:

Readers should engage qualified legal and tax professionals licenced in relevant jurisdictions beforeimplementing any strategies discussed herein. The complexity of international tax compliance, particularly forhigh-net-worth individuals with cross-border holdings, demands individualised analysis by experiencedpractitioners with demonstrable expertise in voluntary disclosure procedures and international tax planning.

Accuracy and Currency:

Whilst every effort has been made to ensure accuracy as of January 2026, unfiled tax returns law evolves continuously throughlegislation, regulation, administrative guidance, and judicial decisions. Proposed regulatory modifications,including the Voluntary Disclosure Practice penalty framework revisions subject to public comment through 22March 2026, may substantially alter compliance requirements and programme availability.

Important Disclosure Regarding Late Tax Returnsand Legal Advice

No Attorney-Client Relationship:

Nothing contained in this guide creates an attorney-client relationship between the reader and the author or anyaffiliated parties. Confidential information should never be transmitted to unfamiliar parties without verifyingtheir credentials and establishing formal engagement agreements.

Limitation of Liability:

To the maximum extent permitted by law, the author disclaims all liability for damages of any kind arising fromreliance upon information contained herein, including but not limited to direct, indirect, incidental,consequential, or punitive damages. Readers assume all risk associated with implementation of strategiesdiscussed.

Bermuda Context:

Whilst this guide is authored from a Bermuda perspective, it addresses US tax obligations applicable to UScitizens, green card holders, and residents regardless of foreign residence location. Bermuda’s status as a zero-income-tax jurisdiction creates particular complexity for US persons residing therein, as foreign tax creditsprovide limited benefit when minimal foreign taxes are paid. Such individuals should prioritise Foreign EarnedIncome Exclusion optimisation and engage professionals familiar with Bermuda-US tax treaty provisions.

Regulatory Compliance:

This guide does not constitute an offer to provide regulated tax preparation, legal, or investment advisoryservices in any jurisdiction. Readers requiring such services should engage appropriately licenced professionalsoperating within applicable regulatory frameworks.

Conclusion: Strategic Imperatives for Immediate Action

The convergence of enhanced global information exchange mechanisms, modernised IRS enforcement technology, and escalating penalties for non-compliance has fundamentally transformed the risk calculus for individuals with historical tax non-filing. The window of opportunity for penalty-free resolution through Streamlined Filing Compliance Procedures remains available as of January 2026 but exists at IRS discretion and could terminate without advance notice.

For high-net-worth individuals with undisclosed foreign financial accounts, the extraordinary FBAR penalties—potentially reaching 50% of account balances annually for willful violations—create existential wealth preservation threats. The mathematical certainty of penalty escalation through continued non-compliance stands in stark contrast to the complete penalty elimination available through timely voluntary disclosure under appropriate programmes.

The strategic pathway forward demands immediate action across five critical dimensions:

Expert Recommendations for Mitigating Tax Non-Compliance Risks

Comprehensive Financial Inventory: Systematically document all worldwide income sources, foreignfinancial accounts, beneficial ownership interests, and international information reporting obligations for themost recent six years minimum.

Objective Willfulness Assessment: Engage experienced international tax counsel to evaluate the facts andcircumstances surrounding historical non-compliance and determine optimal programme selection (Streamlined Procedures, VDP, or alternative pathways).

Proactive Professional Engagement: Retain qualified representation with demonstrable expertise in voluntarydisclosure procedures, evidenced through substantial successful submission experience and relevant credentialsverification.

Methodical Documentation Assembly: Reconstruct financial records through transcript requests, foreignfinancial institution outreach, blockchain analysis for cryptocurrency, and professional valuation for complexassets.

Immediate Programme Participation: Submit complete packages expeditiously to secure available penaltyrelief before potential programme modifications or elimination.

Final Steps to Resolve Your Unfiled Tax Returns Safely

The financial implications of delayed action compound daily through accruing interest and escalating penalties.For a taxpayer with £500,000 in unreported income generating £150,000 annual tax liability across five years,daily interest accumulation alone exceeds £160, whilst failure-to-file and failure-to-pay penalties aggregate to£187,500 before considering accuracy-related penalties or FBAR exposure.

Beyond pure financial considerations, the reputational and operational implications of tax non-compliancepresent material risks for corporate executives, board members, and regulated industry professionals. Discoveryof historical non-compliance through IRS enforcement action rather than voluntary disclosure eliminatesfavourable resolution options whilst potentially triggering securities law, corporate governance, andprofessional licencing consequences.

The path to resolution, whilst demanding comprehensive effort and material professional fees, providescertainty, eliminates criminal prosecution risk for VDP participants, and restores international mobilityunconstrained by passport revocation concerns. For qualifying taxpayers, Streamlined Procedures offercomplete penalty elimination—transforming potential seven-figure or eight-figure penalty exposure intomanageable tax and interest obligations often reduced substantially through Foreign Tax Credits and ForeignEarned Income Exclusion.

Restoring Compliance: Your 2026 Action Plan for Back Taxes

The fundamental strategic imperative remains unambiguous: if you haven’t filed unfiled tax returns in years, voluntarydisclosure under current programme terms represents the optimal pathway to compliance, wealth preservation,and peace of mind. What to do if you haven’t filed taxes in years begins with immediate action—delayedresponses serve no rational purpose and expose taxpayers to escalating financial consequences, potentialcriminal prosecution, and elimination of favourable resolution options.

High-net-worth individuals who have deferred action pending more favourable terms should recognise thatavailable programmes represent the most generous resolution framework likely to exist. Historical precedentthrough OVDP closure demonstrates that programmes terminate when utilisation reaches critical mass, leavingnon-participants exposed to maximum statutory penalties without amnesty eligibility.

The time for strategic action is now. Engage qualified professionals, evaluate programme eligibility objectively,and pursue voluntary disclosure expeditiously to secure available benefits whilst programmes remainaccessible.

FAQs:Resolving Back Taxes and Late Tax Returns

IRS can indefinitely assess taxes, interest, and penalties on unfiled tax returns. Enforcement often targets recent years, but older periods remain open to audit risk via international data sharing.

If tax returns remain unfiled, the statute of limitations never begins, allowing the IRS to assess taxes indefinitely. Once the assessment is made, the standard 10-year collection period then commences.

TThere is no general tax amnesty, but the IRS Streamlined Filing Procedures act as a de facto amnesty for non-willful non-compliance. They offer significant penalty relief when eligibility criteria are met.

Criminal prosecution for unfiled tax returns is rare, usually reserved for deliberate evasion or concealed income. Voluntarily coming forward significantly reduces the risk of a criminal investigation.

Most compliance programmes require filing only the last three to six years of unfiled tax returns. While older years legally exist, they are usually not required for a practical resolution.

Penalties for unfiled tax returns include failure-to-file, failure-to-pay, and daily-compounding interest. In international cases, additional heavy penalties apply for undisclosed foreign financial accounts.

Given the high legal and financial consequences of unfiled tax returns, professional tax counsel is strongly recommended. An expert can assess eligibility.

Disclaimer:

This guide is provided for educational and informational purposes only and does not constitute legal, tax, or professional advice. Readers should consult qualified legal and tax professionals licensed in the relevant jurisdictions before implementing any strategies discussed in this content.

Pingback: Unfiled Taxes Consequences: 10 Years Reddit Legal Advice ✓

Pingback: Bermuda Corporate Income Tax 2025/2026 Guide — BermudaFin

Pingback: Corporate Tax Rate by State 2026: Which State Pays Most?

Pingback: C Corp Tax Filing: 2026 Guide to Avoid 6 Costly Mistakes

Pingback: Federal Corporate Tax Rate 2026: Complete U.S. Guide

Pingback: Help with Overdue Taxes: Penalties, Solutions & Relief

Pingback: IRS Back Taxes Resolution: 7 Fatal Mistakes to Avoid (2026)

Pingback: 401k and Roth 401k Limits 2026: Official IRS Rules