The Filing Mistake That Cost One S-Corp Owner $47,000

A manufacturing S-Corp in Ohio filed its 1120-S return three weeks late in 2024. No extension. No reasonable cause. The IRS assessed a $210-per-shareholder, per-month penalty — and the company had six shareholders.

That mistake cost them $47,880 before any legal fees.

Furthermore, the owner had no idea the clock started ticking on March 15th, not April 15th — a misconception that catches thousands of S-Corp owners every single year.

This Form 1120-S Filing Guide 2026 exists so you don’t become that story.

Whether you manage a two-member S-Corp or a multi-shareholder enterprise with complex distributions, this guide walks you through every requirement, deadline, compliance trigger, and e-filing strategy you need for a clean, penalty-free s corporation return in 2026.

Consequently, by the end of this article, you’ll have a roadmap — not a vague overview — but an actionable, step-by-step system built for precision.

Filing Requirements for Your S Corporation Return in 2026

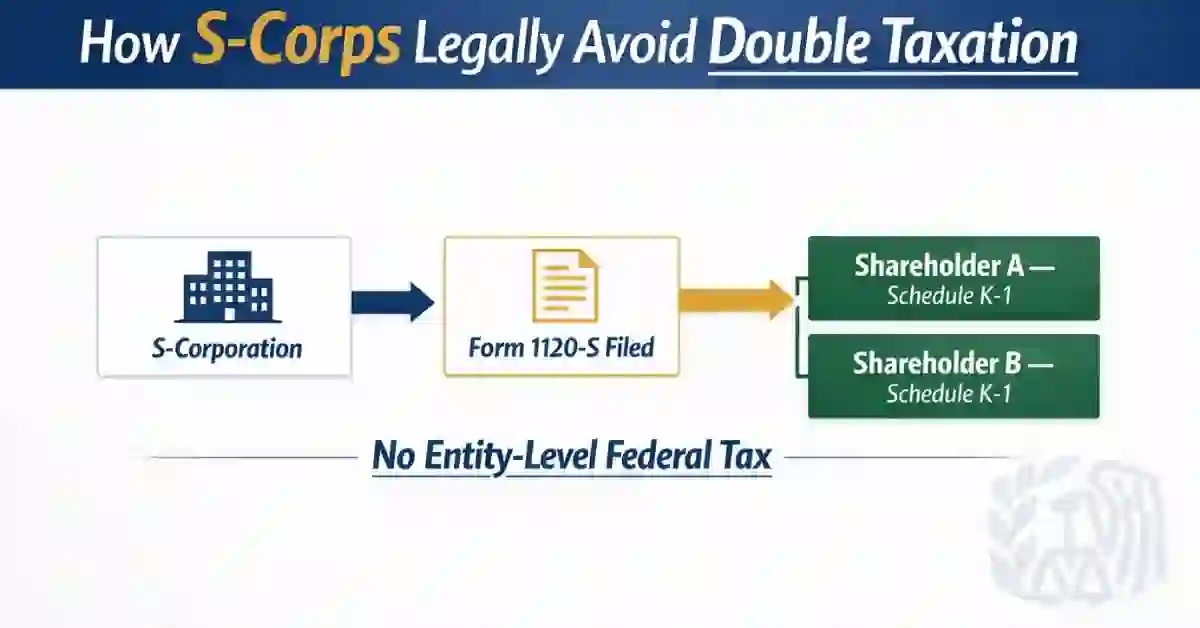

Form 1120-S Filing Guide is the U.S. Income Tax Return for an S Corporation. The IRS uses it to capture your company’s income, deductions, credits, and other financial activity for the tax year.

Here’s the critical distinction: the 1120-S corp itself pays no federal income tax.

Instead, income, losses, deductions, and credits pass through directly to each shareholder’s personal return. This is called pass-through taxation — and in 2026, it remains one of the most powerful structural advantages available to small and mid-sized business owners.

How Pass-Through Taxation Works in 2026

Each shareholder receives a Schedule K-1, which reports their proportional share of the S-Corp’s financial activity. Consequently, shareholders pay individual income tax on their allocated share — not on distributions.

Furthermore, this structure avoids the double taxation that C-Corporations face, where the company pays corporate tax and shareholders pay again on dividends.

The federal 1120-S return, therefore, functions as an informational return at the entity level — but it carries serious compliance weight.

State-Level Note: Tax treatment varies by state. Some states impose minimum franchise taxes or separate S-Corp fees. For jurisdiction-specific data, consult the State Corporate Tax Lookup Tool available on BermudaFin to verify your state obligations before filing.

2026 Filing Deadlines & Key Requirements

Missing a deadline with the IRS 1120-S is not a paperwork inconvenience. It triggers automatic penalties that compound fast.

The March 15th Deadline

The Form 1120-S Filing Guide is due on March 15, 2026, for calendar-year S-Corporations. This is one month earlier than individual returns — a fact that blindsides new S-Corp owners repeatedly.

Fiscal-year S-Corps follow a different schedule: the return is due on the 15th day of the third month after the fiscal year closes.

Automatic Extension: Form 7004

If you need more time, file Form 7004 by March 15th. This grants a six-month extension to September 15, 2026.

Critically, Form 7004 extends the time to file — not the time to pay. Any estimated tax obligations still apply.

Key Forms at a Glance

| Form Name | Purpose | Due Date (Calendar Year) |

| Form 1120-S | Annual S-Corp income tax return | March 15, 2026 |

| Schedule K-1 | Reports each shareholder’s allocated share | Issued with Form 1120-S |

| Form 7004 | Automatic 6-month extension to file | March 15, 2026 |

| Schedule L | Balance sheet per books | Filed with 1120-S |

| Schedule M-2 | Analysis of accumulated adjustments account (AAA) | Filed with 1120-S |

| Schedule M-3 | Net income reconciliation (if assets ≥ $10M) | Filed with 1120-S |

Furthermore, if you have employees, payroll tax deposits and Form 941 filings run on a separate schedule entirely. Coordinate these deadlines with your filing calendar early.

Step-by-Step Instructions for the 1120-S Return

The s corporation return has multiple moving parts. Breaking it into three core phases — Income, Deductions, and Payments — keeps the process clean and audit-resistant.

Phase 1: Reporting Income

Start with Page 1, Lines 1–6 of the IRS 1120-S.

Report gross receipts or sales on Line 1a. Subtract any returns and allowances on Line 1b. The result — net receipts — flows to Line 1c.

In addition to revenue, report:

- Cost of Goods Sold (COGS) — pulled from Schedule A

- Gross profit — Line 3

- Other income — interest, rents, royalties (Lines 4–5)

- Total income — Line 6

Accuracy at this stage is non-negotiable. Discrepancies between your books, Schedule L (balance sheet), and Line 1 are a primary IRS audit trigger.

Phase 2: Claiming Deductions

Lines 7–19 cover your deductions. Common categories include:

- Compensation of officers (Line 7) — this line directly connects to your reasonable salary obligation

- Salaries and wages (Line 8)

- Repairs and maintenance (Line 9)

- Rents (Line 10)

- Taxes and licenses (Line 11)

- Depreciation (Line 14, linked to Form 4562)

- Advertising (Line 16)

- Other deductions (Line 19, with attached statement)

Consequently, every deduction on this return must be substantiated with documentation. Meals, vehicle use, and home office deductions are scrutinized heavily in sub s corporation taxes audits.

Phase 3: Tax & Payments

Most S-Corps owe no entity-level federal tax. However, two situations trigger corporate-level tax:

- Built-In Gains (BIG) Tax — applies if your company converted from a C-Corp and recognized gains within the recognition period

- Excess Net Passive Income Tax — applies if passive income exceeds 25% of gross receipts and the S-Corp has accumulated C-Corp earnings and profits

Report any applicable taxes on Lines 22a–22d and any estimated tax payments on Line 23.

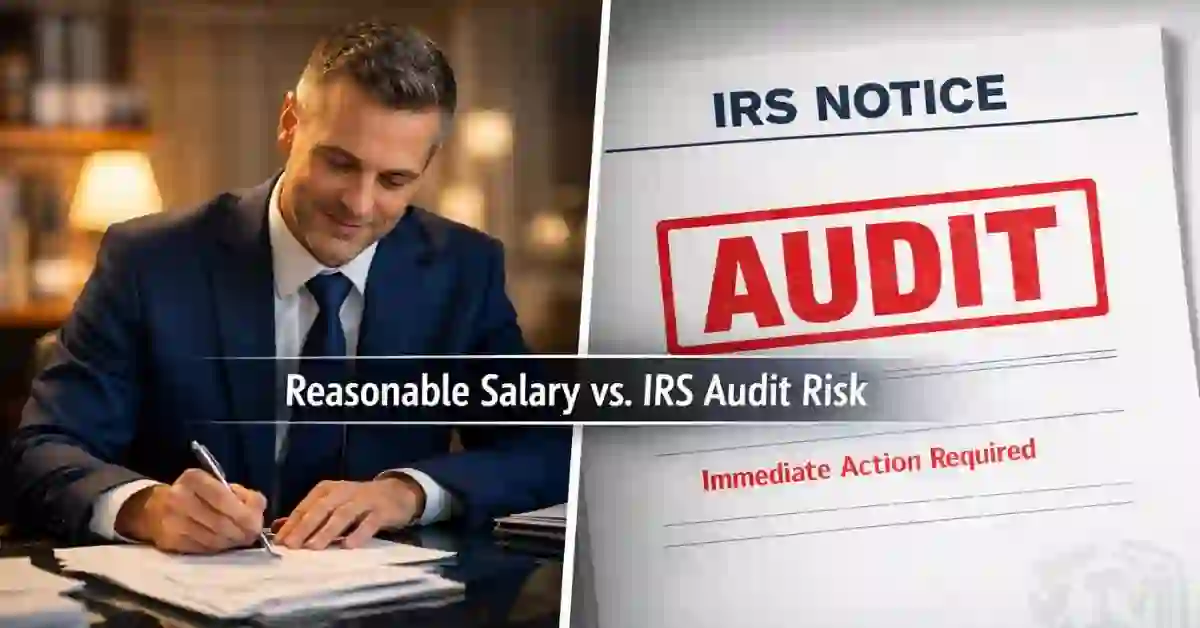

⚠️ Compliance Call-Out: The “Reasonable Salary” Rule

This is the most audited issue in all of sub s corporation taxes.

The rule: Shareholder-employees who perform services for the S-Corp must receive a reasonable salary before taking distributions. The IRS defines “reasonable” as compensation comparable to what an unrelated employer would pay for the same services.

Why it matters: S-Corp distributions are not subject to self-employment tax. Consequently, some owners attempt to minimize salary and maximize distributions — reducing their FICA exposure. The IRS targets this aggressively.

What triggers an audit:

- Officer compensation reported as zero while the business is profitable

- Distributions significantly larger than officer salaries

- No payroll tax filings despite active shareholder-employee involvement

What protects you:

- Document your salary benchmark using industry salary surveys (BLS Occupational Employment Statistics, Glassdoor data, or a compensation expert)

- Maintain consistent payroll records

- Keep minutes and resolutions that support the salary decision

The IRS has prevailed in multiple Tax Court cases on this issue. Furthermore, reclassified distributions trigger back payroll taxes, penalties, and interest — sometimes retroactively for three or more years.

Advanced Compliance — Avoiding IRS Red Flags in 2026

Filing the federal 1120-S correctly is one discipline. Filing it in a way that survives scrutiny is another.

Shareholder Basis: The Tracking Obligation You Cannot Ignore

Basis is each shareholder’s investment in the S-Corp for tax purposes. It determines:

- Whether losses are deductible

- Whether distributions are tax-free or taxable

- The tax treatment of a sale or liquidation

The IRS does not track basis for you. Each shareholder must maintain their own basis schedule, updated annually.

Stock basis increases with:

- Additional capital contributions

- Allocated income items (including tax-exempt income)

Stock basis decreases with:

- Distributions

- Allocated losses and deductions

- Non-deductible, non-capitalizable expenses

In addition to stock basis, shareholders may have debt basis if they’ve made direct loans to the corporation. This is a separate calculation and subject to its own ordering rules.

Failing to track basis leads to over-deducted losses, incorrectly tax-free distributions, and significant assessments upon examination.

Common Red Flags in Sub S Corporation Taxes

The following patterns draw IRS attention:

- Schedule M-2 imbalances — the AAA (Accumulated Adjustments Account) must reconcile precisely

- Losses in excess of basis — the IRS cross-references K-1 losses against known capital contributions

- Large officer compensation changes year over year — especially drops during profitable years

- Inconsistent shareholder ownership percentages — must match the stock ledger exactly

- Late or missing K-1s — shareholders receive K-1s late, file extensions, and the IRS flags timing mismatches

Furthermore, if you have unfiled prior-year returns, the risk multiplies exponentially. The IRS can reconstruct income, assess substitute returns under IRC §6020(b), and initiate collection. [Read BermudaFin’s guide on Unfiled Taxes to understand your exposure and resolution options before the IRS makes the first move.]

The Audit Selection Reality

The IRS uses the Discriminant Function System (DIF) to score returns statistically. Returns that deviate from industry norms — on income ratios, deductions, or officer compensation — receive higher scores and greater examination probability.

Consequently, consistency and documentation are your primary defenses. An audit-ready S-Corp maintains:

- Organized books reconciling to the return

- Signed board minutes for significant transactions

- Payroll records supporting officer compensation

- Basis schedules for every shareholder, updated annually

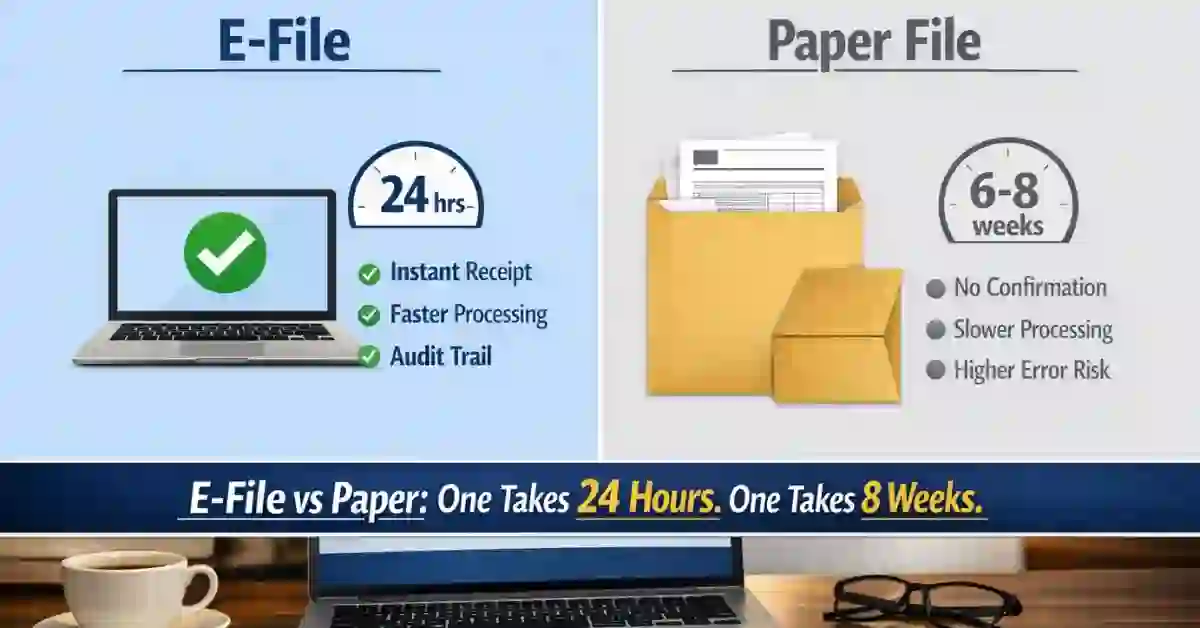

How to File — E-Filing vs Paper Filing in 2026

The IRS strongly prefers electronic filing. In 2026, e-filing is not just faster — it’s structurally safer.

Why the IRS Prefers an E-File Amended 1120-S for Faster Audits

S-Corporations with 10 or more returns of any type (including W-2s and 1099s) are required to e-file the 1120-S under the consolidated e-file mandate effective from tax year 2023 onward.

Smaller entities may still e-file voluntarily — and should.

Advantages of e-filing:

- Immediate acknowledgment — the IRS confirms receipt within 24–48 hours

- Faster processing — refunds and carryforward credits post more quickly

- Reduced transcription errors — no manual data entry by IRS personnel

- Audit trail — electronic submission timestamps are documented

Why Choose to E-File Amended 1120-S for Your S Corporation Return?

When corrections are necessary, you can now efile amended 1120-S returns for tax years 2019 onward. This is a significant improvement over the prior paper-only process.

To file an amended return:

- Check the “Amended Return” box at the top of Form 1120-S

- Attach a statement explaining each change and the reason

- Submit corrected Schedule K-1s to all shareholders

- File amended K-1s with the IRS as part of the amended return

Furthermore, if the amendment affects a shareholder’s individual return, they must file Form 1040-X separately. Coordinate the timing carefully — amended K-1s should reach shareholders before they file or amend their personal returns.

Paper Filing: When It Applies

Paper filing remains an option for very small entities not subject to the e-file mandate. However, paper returns:

- Take 6–8 weeks or longer to process

- Carry a higher risk of processing errors

- Provide no real-time confirmation of receipt

- Delay any refund or credit acknowledgment

In addition to processing delays, paper-filed amended returns take significantly longer — often 20+ weeks — versus the faster resolution available through electronic submission.

The bottom line: E-file unless you have a specific reason not to.

Approved E-File Providers

File through IRS-authorized Modernized e-File (MeF) system-compatible software or a registered tax professional with e-file credentials. The IRS maintains a current list of authorized providers at IRS.gov/efile.

E-File vs Paper Filing: 2026 Comparison Table

| Feature | E-File Amended 1120-S | Paper-Filed Form 1120-S |

| Processing Speed | 2-4 Weeks (Fast) | 8-16 Weeks (Slow) |

| Confirmation | Immediate Digital Receipt | None (Until Processed) |

| Error Rate | Very Low (System Validated) | High (Manual Entry) |

| IRS Preference | Highly Recommended | Deprecated for HNWIs |

Conclusion: Position Your S-Corp for a Clean 2026 Filing — and Beyond

The Form 1120-S Filing Guide 2026 isn’t just about avoiding penalties. It’s about running a structurally sound business entity that works the way it was designed to.

S-Corporations remain one of the most tax-efficient structures for small to mid-sized businesses in the US. Pass-through taxation, flexible compensation strategies, and favorable treatment of fringe benefits all combine to create a compelling advantage — but only when the underlying compliance infrastructure is solid.

In 2026, the IRS continues to expand its data-matching capabilities, cross-referencing K-1 income, payroll records, and third-party information returns with greater precision than ever before. Consequently, sloppy recordkeeping, basis neglect, and officer compensation shortcuts carry more risk today than they did five years ago.

Furthermore, legislative momentum around small business tax policy —Form 1120-S Filing Guide including ongoing discussions about pass-through deduction thresholds and payroll tax reform — makes proactive planning more valuable than reactive filing.

Your action items before March 15, 2026:

- Confirm your officer salary is documented and defensible

- Update every shareholder’s basis schedule for the full tax year

- Reconcile your Schedule M-2 (AAA) against your books

- Determine e-file eligibility and select your authorized provider

- If you have prior unfiled returns, address them before the IRS does

The S-Corp structure rewards disciplined owners. File correctly, document thoroughly, and let the structure do what it was built to do.

FAQ: Form 1120-S Filing Questions Answered

- Q1: What is the penalty for filing Form 1120-S late in 2026?

The IRS assesses a failure-to-file penalty of $235 per shareholder, per month (or part of a month) that the return is late, up to a maximum of 12 months. For a 5-shareholder S-Corp, a single month of lateness generates a $1,175 penalty — before interest. Furthermore, if the IRS determines the failure was fraudulent, a 15% monthly penalty applies, up to 75% of unpaid tax. Filing Form 7004 by March 15th eliminates this risk entirely for entities that need more time.

- Q2: Who is required to e-file the IRS 1120-S in 2026?

S-Corporations that file 10 or more information returns — including W-2s, 1099s, and other required filings — in the aggregate during the calendar year must e-file their federal 1120-S. This threshold dropped from 250 to 10 under final Treasury regulations that took effect for returns filed after January 1, 2024. Consequently, most active S-Corps now fall under the mandatory e-file requirement. Entities below the threshold may still e-file voluntarily — which the IRS actively encourages.

- Q3: Can I e-file an amended Form 1120-S, and how does the process work?

Yes. The IRS now accepts electronically filed amended 1120-S returns for tax years 2019 and forward through the Modernized e-File (MeF) system. To amend, check the “Amended Return” box on the face of the return, attach a written statement detailing each change and the reason for it, and issue corrected Schedule K-1s to all affected shareholders. In addition to the entity-level amendment, each shareholder whose individual return is affected must file Form 1040-X separately. Coordinate timing so shareholders receive corrected K-1s before amending their personal returns.

- Q4: How does shareholder basis affect the deductibility of S-Corp losses?

Losses allocated to a shareholder through their Schedule K-1 are only deductible to the extent the shareholder has sufficient stock basis and debt basis. If allocated losses exceed basis, the excess is suspended — carried forward indefinitely until the shareholder restores enough basis to absorb them. Furthermore, distributions that exceed basis are treated as capital gain, not tax-free return of investment. This is why annual basis tracking is not optional — it directly controls the tax value of the pass-through structure. Shareholders who fail to maintain accurate basis schedules routinely over-deduct losses, triggering IRS assessments with interest and penalties.

This article is intended for informational purposes and reflects federal tax rules applicable to the 2026 tax year. Consult a qualified CPA or tax attorney for advice specific to your situation. IRS rules are subject to legislative and regulatory change.

🏛️ Official Resources

| Resource | URL | Purpose |

|---|---|---|

| IRS Form 1120-S (Official Form) | https://www.irs.gov/forms-pubs/about-form-1120-s | Download the official 2025 Form 1120-S |

| IRS Instructions for Form 1120-S | https://www.irs.gov/instructions/i1120s | Official line-by-line instructions |

| IRS Publication 589 | https://www.irs.gov/publications/p589 | Tax information on S Corporations |

| IRS Form 7004 | https://www.irs.gov/forms-pubs/about-form-7004 | Automatic extension of time to file |

| IRS Schedule K-1 (Form 1120-S) | https://www.irs.gov/forms-pubs/about-schedule-k-1-form-1120-s | Shareholder’s share of income |

| IRS E-File for Business | https://www.irs.gov/businesses/e-file-for-business | Authorized e-file providers list |

| IRS Modernized e-File (MeF) | https://www.irs.gov/e-file-providers/modernized-e-file-mef-internet-filing | MeF system information |

| Treasury Regulation §1.1366-2 | https://www.ecfr.gov | Pass-through loss limitation rules |

| IRC Section 6699 | https://www.law.cornell.edu/uscode/text/26/6699 | Failure-to-file penalty for S-Corps |

| IRS Discriminant Function System | https://www.irs.gov/compliance | Audit selection methodology |

Pingback: BMA Regulations 2026: Complete Bermuda Guide

Pingback: Roth IRA rules for US expats in Bermuda: the 2026 guide

Pingback: Roth IRA Bermuda rules: complete 2026 guide for US expats