By the BermudaFin International Tax Advisory Team | Updated April 2026 | Primary Sources: Economic Substance Act 2018, OECD BEPS Action 5, Bermuda Registrar of Companies Guidance Notes v4.0

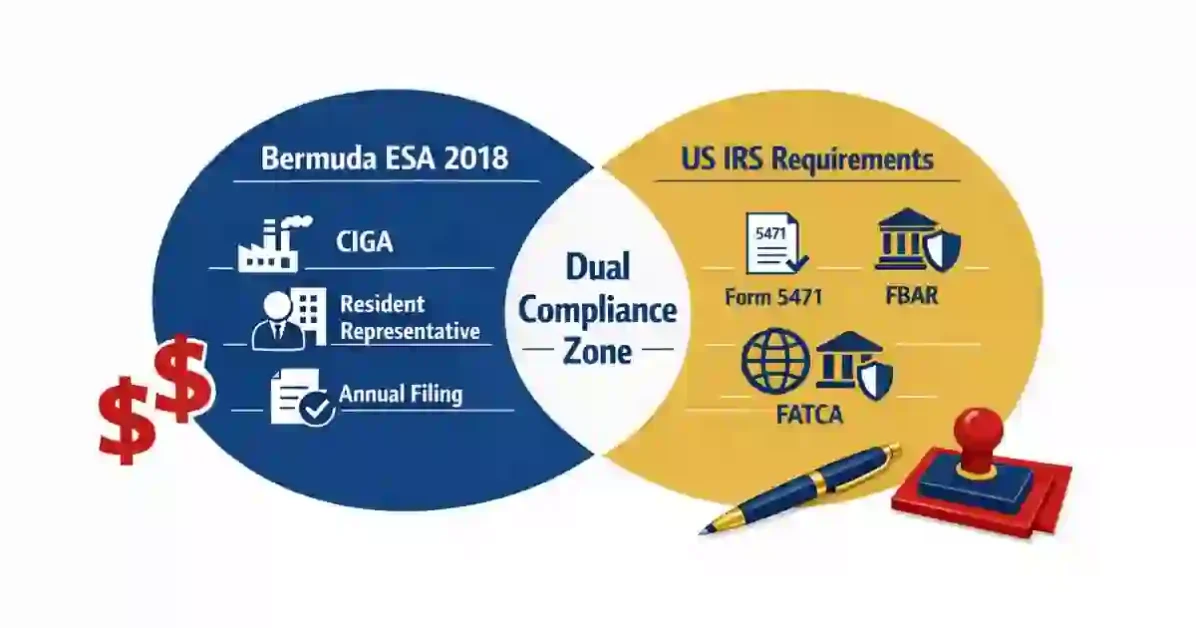

Bermuda economic substance requirements, governed by the Economic Substance Act 2018, mandate that all Bermuda-registered entities conducting relevant activities — including banking, insurance, IP, and fund management — demonstrate genuine local substance. This means Core Income Generating Activities (CIGA) must be performed in Bermuda, supported by a qualified resident representative, adequate local employees, physical premises, and an annual compliance filing. US tax residents face an additional layer: parallel FATCA, Form 5471, and FBAR obligations under IRS rules must align with Bermuda disclosures to avoid dual-jurisdiction penalties and automatic information exchange with the IRS.

Legal Foundation: Economic Substance Act 2018 & OECD Compliance Standards

The Bermuda economic substance requirements originate in the Economic Substance Act 2018 (ESA 2018), enacted by the Bermuda legislature on December 27, 2018, and brought into force on January 1, 2019. The companion Economic Substance Regulations 2018 provide the operational framework. Together, these instruments implement the OECD/G20 Base Erosion and Profit Shifting (BEPS) Action 5 standard on harmful tax practices — specifically, the requirement that jurisdictions with no or nominal corporate tax ensure registered entities exhibit genuine economic activity within the jurisdiction.

For US tax residents, the ESA 2018 creates a two-front compliance obligation. Bermuda’s annual compliance filing system, administered by the Registrar of Companies, intersects directly with IRS foreign reporting requirements. Because Bermuda signed the OECD Common Reporting Standard and maintains a FATCA agreement with the U.S., the Registrar automatically shares any ESA non-compliance notification with the IRS. This transforms Bermuda compliance into a domestic U.S. tax matter rather than a mere offshore formality.

Legislative Update — 2024

Bermuda last amended the Bermuda Economic Substance Act 2018 in 2021. The Registrar of Companies issued Guidance Notes Version 4.0 in 2023, which governs all 2026 filings. You should review any compliance analysis predating Version 4.0 against current guidance before the next filing deadline.

The Nine Relevant Activities — Full Statutory Breakdown

The Bermuda economic substance requirements apply only to entities conducting one or more of the nine statutorily defined relevant activities. Identifying which categories apply to a given entity is the mandatory first step in any substance analysis.

1. Banking business

Entities licensed under the Banks and Deposit Companies Act 1999. Deposit-taking, lending, foreign exchange operations, and financial intermediation all constitute relevant activities. Core Income Generating Activities for banking include raising funds, managing risk, providing loans, and maintaining regulatory capital — all of which must occur in Bermuda.

2. Insurance business

Bermuda is the world’s third-largest insurance and reinsurance hub. All entities registered under the Insurance Act 1978 (Class 1 through Class E) are subject to the full substance test.CIGA includes predicting and calculating risk, determining policy terms, and authorizing claims payments; the company cannot delegate any of these functions outside Bermuda.

3. Fund management business

Investment managers registered under the Investment Business Act 2003 who manage Bermuda-domiciled funds trigger the fund management relevant activity category. Qualified personnel physically present in Bermuda must conduct all portfolio investment decisions, risk management frameworks, and regulatory compliance functions.

4. Finance and leasing business

Special purpose vehicles used in structured finance transactions, asset-backed lending, or equipment leasing are in scope. US family office structures frequently use this category when they employ Bermuda exempted companies as intermediate financing vehicles between US operating entities and offshore capital sources.

5. Headquarters business

Any entity that provides corporate management services, strategic oversight, or administrative coordination to subsidiaries or group entities qualifies as a headquarters business. US residents who establish a Bermuda holding company as a group management hub — even informally — should expect the headquarters relevant activity category to apply.

6. Shipping business

Entities operating, chartering, or managing vessels registered under the Merchant Shipping Act 2002. Bermuda’s blue-chip shipping registry makes this a commercially significant category, particularly for US-based maritime investors with Bermuda flag vessels.

7. Distribution and service centre business

Entities that purchase goods from related foreign parties and resell them, or that provide services to group companies across borders. Distribution hubs serving Caribbean, Latin American, or Asia-Pacific markets through a Bermuda intermediary fall squarely within this relevant activity definition.

8. Intellectual property business

The most globally scrutinized relevant activity. Entities holding, licensing, or exploiting patents, trademarks, software copyrights, or trade secrets are subject to the full CIGA test — reinforced by the OECD’s modified nexus approach, which requires substance to be proportional to R&D expenditure that generated the IP.

High-Risk Alert — IP Holding Structures

US residents who park IP in a Bermuda IP-HoldCo and license back to US operating companies face a triple compliance hazard: Bermuda’s CIGA test, IRS Subpart F income inclusion under IRC §954, and Global Intangible Low-Taxed Income (GILTI) exposure under IRC §951A. A combined economic substance, transfer pricing, and GILTI modeling review is essential before establishing or maintaining such a structure in 2026.

9. Holding company business

Pure equity holding companies that hold shares in subsidiaries face a reduced substance test under ESA 2018, not a zero test. A holding company that also receives royalties, interest, or management fee income may be reclassified as conducting IP, finance, or headquarters business, triggering the full CIGA requirement retroactively.

Core Income Generating Activities (CIGA): What You Cannot Outsource

To satisfy the ESA 2018 substance test, a company must perform, direct, and manage Core Income Generating Activities (CIGA) within Bermuda. The ESA 2018 and its associated Guidance Notes leave no room for doubt: companies cannot outsource CIGA to service providers, group companies, or affiliates located outside Bermuda.This prohibition is the central operational constraint that distinguishes genuine substance from regulatory arbitrage.

The “directed and managed” standard

Beyond performing CIGA in Bermuda, the Board must direct and manage the entity from within the jurisdiction. This means the Board of Directors must hold meetings physically in Bermuda, with a quorum of locally present directors, at a frequency that reflects the scale and complexity of the entity’s operations. Video conference participation by directors located in New York, Miami, or Los Angeles does not satisfy this requirement for quorum purposes.

The Board must record material business decisions in resolutions from meetings held in Bermuda.Contemporaneous, detailed minutes are the primary evidentiary document in any Registrar review. Minutes that record only formal resolutions without reflecting the substantive deliberation of directors physically present in Bermuda are a red flag during compliance examination.

What can we outsourced

The entity may outsource non-CIGA administrative functions, such as payroll processing, routine bookkeeping, IT support, and secretarial services — to third-party service providers. However, the entity must select providers resident in Bermuda and maintain adequate supervisory oversight of the outsourced functions.The oversight capacity itself must reside in Bermuda: a US-resident shareholder monitoring an outsourced Bermuda bookkeeper from their home office in Connecticut does not create Bermuda oversight for ESA purposes.

CIGA by Relevant Activity — Quick Reference

Banking: Raising funds, managing risk, hedging, providing loans. | Insurance: Predicting risk, setting policy terms, paying claims. | Fund Management: Taking investment decisions, managing portfolio risk. | IP Business: Directing R&D, managing and exploiting IP, licensing strategy. | Headquarters: Senior management decisions, incurring group opex. | Finance & Leasing: Agreeing financing terms, acquiring and monitoring assets.

How Pillar Two Influences Bermuda’s Corporate Income Tax Landscape

In a significant policy shift, Bermuda enacted the Corporate Income Tax Act 2023 (CITA 2023), imposing a 15% corporate income tax on large multinational enterprises (MNEs) with global revenues exceeding €750 million, effective for financial years beginning on or after January 1, 2025. This was a direct legislative response to the OECD’s Pillar Two / GloBE (Global Anti-Base Erosion) Rules, which establish a global minimum effective tax rate of 15% for in-scope MNEs.

For US tax residents with Bermuda entities, the interaction between Pillar Two, CITA 2023, and the existing Bermuda economic substance requirements creates a new compliance dimension:

- Entities within Pillar Two scope (€750M+ revenue groups) now face Bermuda corporate income tax at 15%, alongside ESA 2018 substance obligations. A Bermuda entity that previously relied on Bermuda’s zero-tax status as a planning benefit must re-evaluate its post-CITA 2023 economics entirely.

- Entities below the Pillar Two threshold (the vast majority of US-resident Bermuda structures) remain outside CITA 2023 scope but continue to face full ESA 2018 substance obligations. The Economic Substance Act 2018 applies regardless of Pillar Two status.

- GILTI interaction: US MNEs subject to Pillar Two may receive a domestic GILTI offset against Bermuda’s 15% top-up tax, but this coordination is technically complex and requires coordinated advice from both Bermuda and US international tax counsel.

Practitioner Note — Pillar Two & ESA 2018 Co-exist

The introduction of CITA 2023 does not reduce or replace ESA 2018 substance obligations. Both regimes apply independently. An in-scope MNE paying Bermuda corporate income tax still must satisfy the annual compliance filing requirements and demonstrate adequate CIGA — CITA 2023 compliance does not substitute for ESA 2018 compliance.

Resident Representative & Physical Presence in Bermuda

Every entity subject to the Bermuda economic substance requirements must maintain a resident representative — a Bermuda-resident individual or corporate service provider authorized to represent the entity before the Registrar of Companies and the Bermuda Monetary Authority (BMA). The entity must maintain a resident representative at all times; it cannot suspend this mandatory function even during periods of reduced business activity.

Planning to hire local employees in Bermuda to satisfy your

Economic Substance Requirements? Before you hire, calculate

your exact payroll tax liability for 2026.

Use our free Bermuda Payroll Tax Calculator 2026 — instant results, no signup required.

Substance of the resident representative role

The Registrar’s 2023 Guidance Notes elevated expectations for resident representatives beyond pure legal formality. A resident representative must have sufficient working knowledge of the entity’s operations, relevant activity classification, and CIGA to respond meaningfully to regulatory inquiries. A registered agent who serves as nominee resident representative without substantive involvement in the entity’s governance is unlikely to satisfy this standard if the Registrar initiates a compliance review.

Physical presence requirements in detail

The ESA 2018 requires entities to maintain:

- Adequate premises in Bermuda: Exclusive or co-working office space proportionate to business scale. A virtual office address — mail-forwarding services only — does not satisfy this requirement.

- Adequate qualified employees: Personnel with the skills, experience, and authority to conduct or meaningfully supervise CIGA. The “adequacy” standard is facts-and-circumstances based: a complex reinsurance operation requires materially more local headcount than a pure holding company under the reduced test.

- Adequate Bermuda expenditure: Operating costs incurred in Bermuda — salaries, rent, professional fees, local supplier costs — that are proportionate to revenues generated through relevant activities. The Registrar benchmarks local expenditure against industry norms for comparably scaled entities.

Hamilton vs Bermuda-Wide Presence

The ESA 2018 requires physical presence in Bermuda — not specifically in Hamilton. However, given that the Registrar of Companies, BMA, the Supreme Court, and the majority of Bermuda’s financial services infrastructure are located in Hamilton, commercial premises in the City of Hamilton provide the most operationally convenient and regulatorily credible location for most entities.

In-Scope vs Out-of-Scope Entities: Comparison Table

| Entity Type | ESA 2018 Status | Substance Level | US-Specific Risk |

| Bermuda Holding Company (equity only) | Reduced Test | Resident representative + compliant directors + annual filing | Escalates to full test if royalties / interest received |

| Reinsurance / Insurance Company | Full CIGA Required | Local underwriters, BMA license, in-Bermuda risk decisions | PFIC status likely; Form 8621 required for US shareholders |

| IP HoldCo (patents / trademarks / copyright) | Full CIGA Required | R&D direction, nexus expenditure, licensing decisions in Bermuda | GILTI inclusion under IRC §951A; transfer pricing exposure |

| Finance & Leasing SPV | Full CIGA Required | Financing / asset decisions made in Bermuda by local staff | Subpart F passive income for US controlling shareholders |

| HQ Management Company | Full CIGA Required | Senior management physically in Bermuda; local opex incurred | IRS arm’s-length scrutiny on management fees charged to US affiliates |

| Fund Management Entity | Full CIGA Required | Portfolio managers employed and operating in Bermuda | SEC / CFTC registration may apply to US-person fund managers |

| Bermuda Exempted Company (investment vehicle) | Case-by-Case | Depends on whether activities = fund management relevant activity | PFIC / CFC analysis required; protective PFIC election advised |

| Large MNE Entity (€750M+ revenue group) | Full CIGA + CITA 2023 | ESA 2018 substance + 15% Bermuda CIT under Pillar Two | GILTI / Pillar Two credit coordination; Form 5471 Category 5b |

| Non-Resident Entity (foreign co. registered in Bermuda) | Out of Scope | No ESA 2018 substance test applicable | US reporting still required; no Bermuda tax benefit realized |

| Bermuda Exempted Partnership | Out of Scope | Not within ESA 2018 as currently enacted | Form 8865 for US partners; FBAR for foreign financial accounts |

Annual Compliance Filing: Step-by-Step Checklist

To begin the process, the entity submits the annual compliance filing via Bermuda’s BOSS (Beneficial Ownership Secure Search) and e-Legislation portals. Furthermore, the entity must complete this submission within 12 months of its financial year-end. Accordingly, the following checklist outlines the current ESA 2018 requirements and the Registrar’s Guidance Notes for your 2026 filings.

How to Complete Your Bermuda Economic Substance Annual Compliance Filing

1. Classify relevant activities.

Identify all nine relevant activity categories. Document which apply to the entity in the current financial year, with reference to ESA 2018 definitions and Guidance Notes Version 4.0. Retain the analysis memo for six years.

2. Assess CIGA adequacy.

Review all Core Income Generating Activities performed during the year. Confirm each CIGA was performed, directed, and managed in Bermuda by employees or directors physically present in the jurisdiction. Prepare a CIGA adequacy memorandum with supporting evidence

3. Verify resident representative appointment.

Confirm the resident representative remains Bermuda-resident, properly authorized, and substantively informed about the entity’s operations. Update appointment documents if there has been any change in the past 12 months.

4. Compile local substance evidence.

Gather: current office lease or co-working agreement, payroll records for Bermuda-based employees, professional fee invoices from Bermuda service providers, and board meeting minutes confirming meetings held in Bermuda with quorum physically present.

5. Reconcile financial data.

Reconcile Bermuda-source revenues and expenditures against audited or management accounts. Ensure figures to be declared in the annual compliance filing exactly match financial statement data. Discrepancies are an automatic flag in Registrar review.

6. Prepare the ESA declaration.

Complete the statutory declaration via the BOSS portal, disclosing: entity type, all relevant activities conducted, CIGA details, employee headcount and qualifications, premises details, and total Bermuda expenditure incurred in the financial year.

7. Obtain board authorization.

Pass a formal board resolution authorizing the filing at a properly constituted board meeting held in Bermuda. Retain certified minutes. The resolution should reference the specific financial year covered by the declaration.

8. Submit and retain proof of filing.

Submit before the statutory deadline (12 months post financial year-end). Download and archive the submission confirmation. Retain all supporting documentation for a minimum of six years.

9. Update beneficial ownership register simultaneously.

Use the annual compliance filing cycle to verify that the beneficial ownership register reflects current ownership. Any changes since the last filing must be registered within 30 days of occurrence, if that deadline has already passed, regularize immediately and document the correction.

10. Coordinate with US tax counsel.

Cross-reference all Bermuda filing disclosures with Form 5471 / Form 8865, FBAR (FinCEN 114), Form 8938, and any PFIC or GILTI filings. Any revenue, asset, or ownership figure that is inconsistent between Bermuda filings and US foreign reporting is a primary IRS audit trigger. File US foreign reporting conservatively and on time.

Beneficial Ownership Register: Obligations & Deadlines

Unlike the annual compliance filing, the beneficial ownership register imposes a continuous, real-time obligation under the Companies Act 1981. In addition, the legislature amended this Act specifically to align with FATF Recommendation 24 and OECD transparency standards.

To fulfill this requirement, the entity’s registered agent maintains the register and uploads it to Bermuda’s BOSS platform. Consequently, this platform grants the BMA, law enforcement, and OECD partner jurisdictions structured access to the data.

Who qualifies as a registrable beneficial owner

Furthermore, the entity must register any individual who ultimately owns or controls, directly or indirectly more than 25% of the shares or voting rights, or who exercises effective control over its management. To ensure compliance, the Registrar requires firms to “look through” nominee arrangements, trust structures, and multi-layered holding chains to identify the Ultimate Beneficial Owner (UBO).

25% Bermuda vs 10% IRS — The Threshold Discrepancy

A US person holding 15% of a Bermuda company will not appear on Bermuda’s beneficial ownership register (below the 25% threshold) but may still be a Category 4 or 5 filer on Form 5471 (IRS 10% threshold for US shareholders of controlled foreign corporations). Compliance counsel must map both thresholds independently , an individual may be invisible to the Bermuda register yet have full IRS reporting obligations.

Mandatory information for each beneficial owner

- Full legal name and any previous names used

- Current residential address (not a business or registered agent address)

- Date of birth and nationality

- Nature and extent of beneficial interest (exact percentage ownership and nature of control)

- Date on which the person became — or ceased to be — a registrable beneficial owner

The 30-day update rule

The entity must register any change in beneficial ownership, whether through share transfer, restructuring, change in trust beneficiaries, or any other mechanism, within 30 calendar days.This is not a best-efforts guideline; it is a statutory obligation. Failure to update the beneficial ownership register within 30 days carries penalties of BMD $5,000 per director for a first instance, escalating to BMD $25,000 and potential criminal referral for persistent or willful non-compliance.

Filing Deadlines & Penalty Timeline

| Obligation | Deadline | First-Instance Penalty | Escalated / Criminal Penalty |

| Annual compliance filing (ESA declaration) | Within 12 months of financial year-end | BMD $10,000 | BMD $100,000 + possible strike-off |

| Failure to meet substance test | Upon Registrar determination | BMD $25,000 | BMD $250,000 (Year 2+) |

| Beneficial ownership register update | Within 30 days of any change | BMD $5,000 per director | BMD $25,000 + criminal referral |

| Filing false or misleading information | Upon Registrar discovery | BMD $50,000 | Criminal prosecution; up to 5 years imprisonment |

| Failure to maintain resident representative | Continuous obligation | BMD $10,000 | Strike-off / dissolution |

| OECD automatic information exchange | Annual — calendar year basis | Non-compliant entities flagged to IRS; cross-referenced against Form 5471 / FBAR filings | |

| US Form 5471 (CFC reporting) | With federal return (April 15 / Oct 15 extended) | USD $10,000 per form per year | USD $50,000 + criminal exposure |

| FBAR — FinCEN 114 | April 15 (auto-extended to October 15) | USD $10,000 per account (non-willful) | USD $100,000 or 50% of balance (willful) |

Outbound Resources: High-Authority Reference

Outbound Resources: High-Authority References

To ensure technical accuracy, this guide cites the following primary and regulatory sources throughout. Practitioners should use these authoritative references when conducting due diligence on Bermuda economic substance requirements and related OECD transparency standards.

OECD — BEPS Action 5: Harmful Tax Practices

Official OECD guidance on the minimum standard for countering harmful tax practices, including the Bermuda Economic Substance Requirements underpinning ESA 2018.oecd.org — BEPS Action 5 →

Bermuda Registrar of Companies —Bermuda Economic Substance Requirements Guidance Notes

Version 4.0 (2023) — the primary regulatory guidance document for ESA 2018 compliance, CIGA definitions, and annual compliance filing requirements.

roc.gov.bm — Economic Substance →

IRS — International Taxpayers: Foreign Corporation Reporting (Form 5471)

IRS guidance on Form 5471 obligations for US persons with interests in controlled foreign corporations, including Bermuda-registered entities.

FinCEN — FBAR Reference Guide (FinCEN Form 114)

The authoritative reference for foreign bank and financial account reporting obligations, including accounts held by Bermuda entities owned by US persons.

Bermuda Monetary Authority — Regulatory & Licensing Framework

BMA oversight of Bermuda’s insurance, banking, and investment businesses — essential for entities conducting relevant activities requiring BMA registration.

bma.bm — Bermuda Monetary Authority →

OECD — Pillar Two / GloBE Rules (Global Minimum Tax)

The OECD’s technical guidance on the 15% global minimum tax, directly relevant to Bermuda’s Corporate Income Tax Act 2023 and its interaction with ESA 2018.oecd.org — Pillar Two GloBE Rules →

Conclusion:

The Bermuda economic substance requirements are not a static compliance checkbox — they are a dynamic regulatory framework that demands annual reassessment as business activities evolve, ownership structures change, and the OECD compliance standards continue to develop. The Economic Substance Act 2018, Bermuda’s new Corporate Income Tax Act 2023, and the IRS’s parallel foreign reporting obligations together constitute a multi-layered compliance architecture that demands coordinated, proactive management.

Because the IRS monitors these structures closely, US tax residents who hold Bermuda entities must invest in genuine local substance. Specifically, they must employ qualified directors and staff physically present in Bermuda, conduct documented Core Income Generating Activities within the jurisdiction, and maintain real office premises with adequate local expenditure.

Additionally, the entity must submit an annual compliance filing that accurately and consistently reflects its substance position. To ensure transparency, the company must also maintain the beneficial ownership register with precision and update it within 30 days of any change.

The cost of proper compliance, while real, is substantially lower than the combined penalty exposure, IRS audit risk, and reputational consequences of non-compliance in a jurisdiction where automatic information exchange with the United States is routine and accelerating. Professional advice from counsel experienced in both Bermuda regulatory law and US international tax is not optional — it is the foundation of any defensible compliance posture.

FAQ: Bermuda Economic Substance Requirements for US Tax Residents

- Q1. What are the Bermuda Economic Substance Requirements?

Bermuda Economic Substance Requirements, established under the Economic Substance Act 2018, mandate that all Bermuda-registered entities conducting relevant activities — such as banking, insurance, IP holding, or fund management — must demonstrate genuine local substance. This includes performing Core Income Generating Activities (CIGA) in Bermuda, maintaining a qualified resident representative, adequate local employees, physical office premises, and submitting an annual compliance filing to the Bermuda Registrar of Companies.

- Q2. Who must comply with the Bermuda Economic Substance Act 2018?

Any entity registered in Bermuda that conducts one or more of the nine relevant activities — banking, insurance, fund management, finance and leasing, headquarters business, shipping, distribution, intellectual property, or holding company business — must comply. This includes Bermuda exempted companies, limited liability companies, and partnerships conducting relevant activities, regardless of whether the owner is a US tax resident, UK national, or any other foreign person.

- Q3. What happens if a Bermuda entity fails the Economic Substance test?

Failing the Bermuda Economic Substance test triggers serious consequences. For a first instance, the Bermuda Registrar of Companies imposes a penalty of BMD $25,000. For a second consecutive year of failure, the penalty escalates to BMD $250,000. Persistent non-compliance can result in the entity being struck off the Bermuda register — effectively dissolving the company. Additionally, under OECD automatic information exchange, the Registrar notifies partner jurisdictions including the United States IRS.

- Q4. Can Core Income Generating Activities (CIGA) be outsourced outside Bermuda?

No. The Economic Substance Act 2018 explicitly prohibits outsourcing CIGA to service providers, group companies, or affiliates located outside Bermuda. CIGA must be performed, directed, and managed within Bermuda by qualified employees or directors physically present in the jurisdiction. Non-CIGA administrative functions — such as bookkeeping, payroll, and IT support — may be outsourced, but only to Bermuda-resident service providers, and oversight of those functions must also remain in Bermuda.

- Q5. What is a Resident Representative in Bermuda and is it mandatory?

Yes, a resident representative is mandatory for every Bermuda entity subject to the Economic Substance Act 2018. A resident representative is a Bermuda-resident individual or corporate service provider authorized to represent the entity before the Registrar of Companies and the Bermuda Monetary Authority. Under the 2023 Guidance Notes, the resident representative must have substantive working knowledge of the entity’s operations — a purely nominal appointment does not satisfy regulatory expectations.

- Q6. How does the Bermuda Economic Substance requirement affect US tax residents specifically?

US tax residents face a dual compliance burden. They must simultaneously satisfy Bermuda’s Economic Substance Act 2018 requirements — CIGA, resident representative, annual compliance filing, and beneficial ownership register — and US federal foreign reporting obligations including Form 5471, FBAR (FinCEN 114), Form 8938 (FATCA), and potentially Form 8621 (PFIC). Since Bermuda automatically exchanges non-compliance information with the IRS under OECD CRS and the US-Bermuda FATCA IGA, a Bermuda compliance failure directly triggers IRS scrutiny.

- Q7. What is the deadline for the Bermuda Annual Compliance Filing?

The annual compliance filing must be submitted within 12 months of the entity’s financial year-end. For most Bermuda exempted companies whose financial year ends on December 31, the filing deadline is December 31 of the following year. Missing this deadline attracts a first-instance penalty of BMD $10,000, escalating to BMD $100,000 for continued non-compliance, with potential strike-off of the entity from the Bermuda register.

- Q8. What is the Beneficial Ownership Register in Bermuda?

The Beneficial Ownership Register is a statutory record maintained under the Companies Act 1981, listing all individuals who ultimately own or control more than 25% of shares or voting rights in a Bermuda entity. It is uploaded to Bermuda’s BOSS (Beneficial Ownership Secure Search) platform, accessible by the Bermuda Monetary Authority and law enforcement. Any change in beneficial ownership must be registered within 30 days. Failure to update carries penalties of BMD $5,000 per director for a first instance.

- Q9. Does Bermuda now have a Corporate Income Tax?

Yes. Bermuda enacted the Corporate Income Tax Act 2023 (CITA 2023), imposing a 15% corporate income tax on large multinational enterprises (MNEs) with global revenues exceeding €750 million, effective from January 1, 2025. This was enacted in direct response to the OECD Pillar Two / GloBE minimum tax rules. However, entities below the €750 million threshold — the vast majority of US-resident Bermuda structures — remain outside CITA 2023 scope and continue to pay zero Bermuda corporate income tax.

- Q10. Is a Bermuda IP Holding Company still viable for US tax residents in 2026?

It is legally viable but operationally and fiscally complex. A Bermuda IP HoldCo triggers the full Economic Substance test under the Economic Substance Act 2018, requiring genuine R&D direction, licensing strategy decisions, and nexus expenditure in Bermuda. For US tax residents, it also creates GILTI exposure under IRC §951A, potential Subpart F income inclusion, and transfer pricing scrutiny by the IRS. A combined economic substance review, GILTI modeling, and transfer pricing analysis is essential before establishing or maintaining such a structure.

Financial & Legal Disclaimer

Please note that BermudaFin.com publishes this guide for informational and educational purposes only. Consequently, this document does not provide legal advice, tax advice, or a solicitation of professional services.

Furthermore, the content presents the authors’ interpretation of the Economic Substance Act 2018, the Corporate Income Tax Act 2023, and related US federal tax provisions as of April 2026. Because laws and regulatory guidance change frequently, readers must not rely on this guide as a substitute for professional counsel. Instead, you should seek specific, current advice from qualified legal and tax professionals licensed in Bermuda and the United States.

Furthermore, reading or acting on the content of this guide does not form an attorney-client relationship. Consequently, BermudaFin.com, its authors, and affiliated entities expressly disclaim all liability for any loss, damage, or regulatory consequence. This disclaimer applies to any reliance on this material unless you first obtain independent professional advice tailored to your specific facts and circumstances.

Primary legal sources: Economic Substance Act 2018; Bermuda Economic Substance Requirements Regulations 2018; Corporate Income Tax Act 2023; Registrar of Companies Guidance Notes v4.0 (2023); OECD BEPS Action 5; OECD Pillar Two/GloBE Rules (2021); IRC §§951, 951A, 954, 1291–1298; FinCEN Form 114; IRS Forms 5471, 8621, 8865, 8938.

Pingback: Bermuda Monetary Authority New Regulations 2026 Outlook

Pingback: Roth IRA rules for US expats in Bermuda: the 2026 guide