The Internal Revenue Service (IRS) officially increased the 401k and roth 401k limits for 2026 to help retirement savers combat persistent inflationary pressures. According to IRS Notice 2025-67, the individual contribution limit has climbed to $24,500, providing a substantial window for employees to shield more income from taxes. Additionally, the full implementation of the SECURE 2.0 Act introduces nuanced “Super Catch-Up” tiers and mandatory Roth requirements for high earners. Navigating these updates is essential for maximizing your tax-efficient wealth and securing financial independence in 2026.

What Are 401k and Roth 401k Limits in 2026?

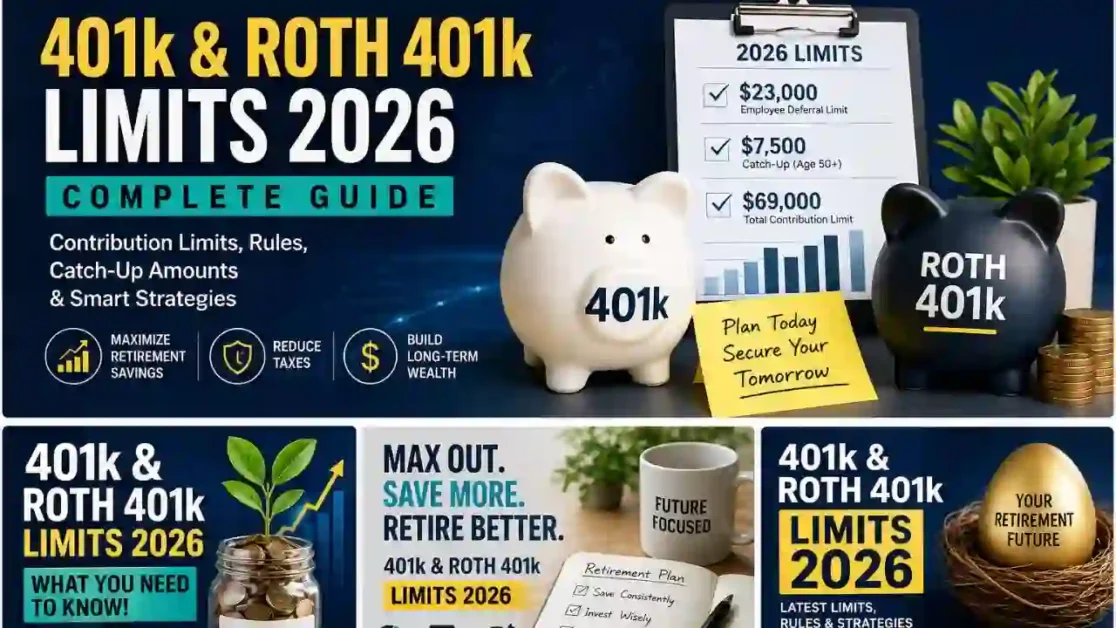

For the 2026 tax year, the IRS allows individuals to contribute up to $24,500 to their 401(k) or Roth 401(k) plans. If you are aged 50 or older, you can save a total of $32,500. Furthermore, a specialized “Super Catch-Up” enables participants aged 60 to 63 to contribute a massive $35,750 annually. The total combined limit, including employer matching, has reached $72,000.

2026 401(k) & Roth 401(k) Limits: Detailed Breakdown

To optimize your savings strategy, you must understand how these limits have evolved from the previous year. The following table highlights the official 2026 adjustments:

| Contribution Category | 2025 Limit | 2026 Limit | Change |

| Individual Deferral (Under 50) | $23,500 | $24,500 | +$1,000 |

| Catch-Up (Age 50-59 & 64+) | $7,500 | $8,000 | +$500 |

| Super Catch-Up (Ages 60-63) | $11,250 | $11,250 | No Change |

| Total Limit (Emp + Employer) | $70,000 | $72,000 | +$2,000 |

| IRA Contribution Limit | $7,000 | $7,500 | +$500 |

The SECURE 2.0 Revolution: New Rules for 2026

The SECURE 2.0 Act fundamentally changes how the 401k and roth 401k limits apply to different demographic groups. Specifically, it introduces age-based incentives while imposing new restrictions on high-income professionals.

The “Super Catch-Up” (Ages 60–63)

If you turn 60, 61, 62, or 63 during the 2026 tax year, you qualify for an enhanced contribution tier. Instead of the standard catch-up, the IRS allows you to defer an additional $11,250. Consequently, this “Super Catch-Up” allows you to stash away $35,750 in a single year, facilitating a powerful “final sprint” toward retirement.

Mandatory Roth Catch-Ups for High Earners

The IRS now requires a structural change for savers with significant income. If your FICA wages from the 2025 calendar year exceeded $150,000, the law mandates that your catch-up contributions enter a Roth 401(k) account. Because these funds are after-tax, you can no longer use catch-up dollars to lower your immediate taxable income.

Impact on Tax Deductions for Individuals earning $150k+

Starting in 2026, the IRS strictly enforces this “Roth-only” rule for high earners. Specifically, because you must direct your catch-up funds into a Roth account, you will lose the upfront tax deduction for that portion of your savings. However, this shift provides a massive long-term advantage because those contributions and all subsequent investment gains will grow entirely tax-free. Furthermore, this ensures that high earners maintain a path to Roth-style growth, even if their income usually disqualifies them from traditional Roth IRAs.

Traditional 401(k) vs Roth 401(k): 2026 Strategic Decision

Both plans share the $24,500 individual limit, but choosing between them depends entirely on your current tax bracket versus your future expectations.

Why Choose a Traditional 401(k)?

You should prioritize a Traditional 401(k) if you currently sit in a high tax bracket (32% or higher). By contributing pre-tax dollars, you effectively lower your Adjusted Gross Income (AGI) today. This strategy proves most effective if you expect your income — and therefore your tax rate — to decrease during retirement.

Why Choose a Roth 401(k)?

Conversely, the Roth 401(k) is superior if you are early in your career or expect tax rates to rise. Although you pay taxes on the money now, you secure 100% tax-free withdrawals later. Additionally, SECURE 2.0 eliminated Required Minimum Distributions (RMDs) for Roth 401(k) accounts, allowing your wealth to compound indefinitely without forced withdrawals.

Global Perspective: Retirement Limits in UK, Canada, & Bermuda

For professionals managing international assets, the 401k and roth 401k limits serve as a benchmark for comparison against other major financial hubs.

United Kingdom (Workplace Pensions)

In the UK, the Annual Allowance for workplace pensions remains at £60,000 for the 2026/27 tax year. While this limit is higher than the US 401(k), high earners must navigate the “Tapered Annual Allowance,” which can reduce their contribution ceiling to as little as £10,000 based on total earnings.

Canada (RRSP & TFSA Updates)

Canadian residents see an RRSP limit increase to $33,810 for 2026. Moreover, the Tax-Free Savings Account (TFSA) room expands by an estimated $7,000. Unlike the US system, Canada allows you to carry forward unused contribution room from previous years, providing greater flexibility for those with fluctuating incomes.

Bermuda (Pension Reform 2026)

Bermuda continues its pension modernization project in 2026. Public sector contribution rates have adjusted to ensure long-term solvency, while private sector employees maintain the mandatory 10% total contribution. Because Bermuda has no personal income tax, the “Roth vs Traditional” debate is irrelevant; instead, the focus remains on maximizing voluntary contributions to capitalize on zero-tax investment growth.

Common Mistakes to Avoid

- Exceeding contribution limits

- Ignoring Roth benefits

- Missing employer match

- Withdrawing early (before age 59.5)

- Not adjusting contributions annually

Advanced Wealth Strategies for 2026

To truly maximize your benefits under the 401k and roth 401k limits, you must look beyond basic salary deferrals.

The Mega Backdoor Roth Strategy

If your employer’s plan allows for “After-Tax” (non-Roth) contributions, you can potentially save up to the total $72,000 limit. By immediately converting the excess after-tax funds into a Roth 401(k) or Roth IRA, you effectively bypass the standard $24,500 individual cap.

The “True-Up” Provision Audit

Many high earners “front-load” their contributions to maximize time in the market. However, if you reach the $24,500 limit by mid-year, your employer might stop their matching contributions. Therefore, you should verify if your plan includes a “True-Up” provision to ensure you receive the full company match regardless of your contribution timing.

Spousal IRA Coordination

Even if your spouse does not earn an income, you can contribute $7,500 to a Spousal IRA on their behalf. This effectively adds another layer of tax-advantaged protection to your household’s total retirement portfolio.

Common Pitfalls and Compliance Issues

Even seasoned investors can make mistakes that lead to heavy IRS penalties.

Multiple Job Contribution Limits

The $24,500 limit is per person, not per employer. If you switch jobs during 2026, you must track your total contributions across both plans. Exceeding this combined limit results in double taxation unless you correct the error before the tax deadline.

Excess Deferral Penalties

If you accidentally over-contribute, you must request an “excess deferral distribution” by April 15, 2027. Failure to do so means the IRS will tax the excess amount twice — once in the year of contribution and again upon withdrawal.

FAQ – 401k and Roth 401k Limits 2026

- Can I contribute to both a Traditional and Roth 401(k) in 2026?

Yes, you can split your contributions. However, the IRS mandates that your combined total must not exceed the $24,500 individual limit. You must track this across all employers if you switch jobs mid-year.

- What is the 2026 "Super Catch-Up" for ages 60–63?

Under the SECURE 2.0 Act, individuals aged 60 to 63 qualify for a higher catch-up limit of $11,250. This allows a total individual contribution of $35,750, helping late-career savers maximize their final retirement sprint.

- Do employer matches count toward the $24,500 limit?

No. The $24,500 limit applies only to your salary deferrals. Employer matches and profit-sharing count toward the total annual addition limit, which is $72,000 for 2026.

- What if I accidentally exceed the 2026 401(k) limits?

You must notify your plan administrator and withdraw the excess funds plus earnings by April 15, 2027. If you fail to do this, the IRS will tax the excess amount twice.

- Is the Roth 401(k) mandatory for high earners in 2026?

Yes, for catch-up contributions. If you earned over $150,000 in 2025, the IRS requires your 2026 catch-up contributions to be made to a Roth 401(k).

Conclusion: Your 2026 Financial Roadmap

The updated 401k and roth 401k limits for 2026 offer a robust framework for building long-term wealth. To stay ahead, you must automate your increases, understand your age-based catch-up rights, and strategically choose between Traditional and Roth buckets. By leveraging the new $24,500 limit and the SECURE 2.0 “Super Catch-Up,” you are not just saving for the future — you are engineering a tax-efficient legacy.

Disclaimer: This guide is for informational purposes only. Please consult a Certified Financial Planner (CFP) or tax professional before making significant investment decisions based on IRS Notice 2025-67.

Official Resources:

To verify these figures and dive deeper into the technical tax codes, refer to the following official sources:

- IRS Official Announcement: IRS Notice 2025-67 – Retirement Plan Limitations for 2026

- Comprehensive Guide: IRS Retirement Topics – 401(k) and Profit-Sharing Plan Contribution Limits

- Legislative Background: The SECURE 2.0 Act of 2022 – Full Text

- Global Context: UK Pensions Advisory Service and Canada Revenue Agency (CRA) RRSP Limits

Pingback: Roth IRA rules for US expats in Bermuda: the 2026 guide

Pingback: Roth IRA Bermuda rules: complete 2026 guide for US expats